You might also like

- QuestionsDocument10 pagesQuestionsYat Kunt ChanNo ratings yet

- International FInanceDocument3 pagesInternational FInanceJemma JadeNo ratings yet

- Fiscal and Monetary Policy of GermanyDocument125 pagesFiscal and Monetary Policy of Germanyarpit vora100% (2)

- HSBC Case StudyDocument4 pagesHSBC Case Studyrajkamboj52100% (1)

- Cultural Awareness: Worksheet ADocument7 pagesCultural Awareness: Worksheet ARani PuspitaNo ratings yet

- Customer Service Representative Cover Letter Windsor - BlueDocument3 pagesCustomer Service Representative Cover Letter Windsor - BlueMocanu GabrielaNo ratings yet

- PPT-How Writers WriteDocument10 pagesPPT-How Writers WriteSplendidgodNo ratings yet

- Articles of Incorporation Example 02Document3 pagesArticles of Incorporation Example 02Sandra VargasNo ratings yet

- Sess 1 & 2 Basic AccountingDocument48 pagesSess 1 & 2 Basic Accountingdilshan jayawardanaNo ratings yet

- ACCT112 Wk4b Job Costing-Handout-LMSDocument16 pagesACCT112 Wk4b Job Costing-Handout-LMSKelvin Lim Wei LiangNo ratings yet

- Users of Financial Accounts - Tutor2u BusinessDocument5 pagesUsers of Financial Accounts - Tutor2u BusinessmwhaliNo ratings yet

- 7.2 Financial Ratio AnalysisDocument31 pages7.2 Financial Ratio AnalysisteeeNo ratings yet

- LESSON 16 - Cost, Revenue and ProfitDocument5 pagesLESSON 16 - Cost, Revenue and ProfitfarahNo ratings yet

- Wiley - Chapter 5: Balance Sheet and Statement of Cash FlowsDocument35 pagesWiley - Chapter 5: Balance Sheet and Statement of Cash FlowsIvan Bliminse75% (4)

- Accounting For Trading Business Chapter 5Document40 pagesAccounting For Trading Business Chapter 5MUHAMMAD AMMAD ARSHAD100% (1)

- Types of Business OrganizationDocument20 pagesTypes of Business OrganizationFernandaNo ratings yet

- Managerial Accounting 5th Ed. Kieso PPTs For ChaptersDocument63 pagesManagerial Accounting 5th Ed. Kieso PPTs For Chaptersj loNo ratings yet

- Topic 3 Example of Trial BalanceDocument6 pagesTopic 3 Example of Trial BalanceSalsabilaFahimNo ratings yet

- CH 01Document31 pagesCH 01Barisqi Januar RomaldoNo ratings yet

- The Thyroid Health ProtocolDocument10 pagesThe Thyroid Health ProtocolloanneNo ratings yet

- Chapter 2 - National IncomeDocument71 pagesChapter 2 - National IncomeRia Athirah100% (1)

- Causes of InflationDocument25 pagesCauses of InflationBushra NaumanNo ratings yet

- 4 - Introduction To MarketingDocument45 pages4 - Introduction To MarketingBerkshire Hathway coldNo ratings yet

- The Theory of The FirmDocument3 pagesThe Theory of The FirmspelicansNo ratings yet

- Cost Volume ProfitDocument73 pagesCost Volume ProfitAsiiyah100% (1)

- List of IFRS & IASDocument6 pagesList of IFRS & IASKhurram IqbalNo ratings yet

- What Are The Dimensions of PracticeDocument6 pagesWhat Are The Dimensions of PracticeNavarro Angelo100% (1)

- Financial StatementDocument84 pagesFinancial StatementssdjyfkhglgkfjugliNo ratings yet

- Target Costing Presentation FinalDocument57 pagesTarget Costing Presentation FinalMr Dampha100% (1)

- Absorption and Marginal CostingDocument4 pagesAbsorption and Marginal CostingJonathan Smoko100% (1)

- CH 13Document28 pagesCH 13ReneeNo ratings yet

- Backflush CosingDocument15 pagesBackflush Cosingapi-3730425100% (4)

- 3.sales Variance AnalysisDocument38 pages3.sales Variance Analysiskamasuke hegdeNo ratings yet

- Seasonal Gift IdeasDocument2 pagesSeasonal Gift IdeasMark HayesNo ratings yet

- CHAPTER 1 - Aims and Objectives and Factors of ProductionDocument4 pagesCHAPTER 1 - Aims and Objectives and Factors of ProductionVinetha Karunanithi100% (1)

- Financial RatiosDocument15 pagesFinancial RatiosHojol100% (1)

- 05 AC212 Lecture 5-Marginal Costing and Absorption Costing PDFDocument22 pages05 AC212 Lecture 5-Marginal Costing and Absorption Costing PDFsengpisalNo ratings yet

- The Regulatory Framework of AccountingDocument52 pagesThe Regulatory Framework of Accountingssentu100% (1)

- Elegant Campaign: Here Is Where Your Presentation BeginsDocument49 pagesElegant Campaign: Here Is Where Your Presentation BeginsAnskaria100% (1)

- Theories of UnemploymentDocument28 pagesTheories of UnemploymentIndu GuptaNo ratings yet

- Marginal Revenue and Marginal Cost ApproachDocument6 pagesMarginal Revenue and Marginal Cost ApproachswastikaNo ratings yet

- Leverage MaterialsDocument9 pagesLeverage MaterialsArnnava SharmaNo ratings yet

- CA IPCC Costing & FM Quick Revision NotesDocument21 pagesCA IPCC Costing & FM Quick Revision NotesChandreshNo ratings yet

- CH 8Document16 pagesCH 8emanmamdouh596No ratings yet

- Chapter 7Document53 pagesChapter 7Baby KhorNo ratings yet

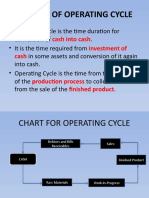

- Concept of Operating Cycle: Cash Into Cash Investment of CashDocument6 pagesConcept of Operating Cycle: Cash Into Cash Investment of CashVenket RamanaNo ratings yet

- Ch07 Incremental AnalysisDocument47 pagesCh07 Incremental Analysisعبدالله ماجد المطارنهNo ratings yet

- Chapter Two-Accounting For InventoryDocument25 pagesChapter Two-Accounting For Inventoryzewdie100% (1)

- Module IV - Working Capital ManagementDocument50 pagesModule IV - Working Capital ManagementAshwin DholeNo ratings yet

- Managerial Accounting: Tools For Business Decision-MakingDocument56 pagesManagerial Accounting: Tools For Business Decision-MakingdavidNo ratings yet

- Cost Allocation Joint by ProductsDocument31 pagesCost Allocation Joint by ProductsFanie Saphira100% (1)

- Valuation Measurement and Value CreationDocument44 pagesValuation Measurement and Value CreationalijordanNo ratings yet

- EconomicsDocument78 pagesEconomicsEliz CiprianoNo ratings yet

- Cost II-ch 1 - CVPDocument45 pagesCost II-ch 1 - CVPYitera SisayNo ratings yet

- Blocher8e EOC SM Ch04 FinalDocument46 pagesBlocher8e EOC SM Ch04 FinalDiah ArmelizaNo ratings yet

- Cost ManagementDocument18 pagesCost ManagementGeo Rublico ManilaNo ratings yet

- Q and As-Advanced Management Accounting - June 2010 Dec 2010 and June 2011Document95 pagesQ and As-Advanced Management Accounting - June 2010 Dec 2010 and June 2011Samuel Dwumfour100% (1)

- CHP 12 - Strategy, Balanced Scorecard, and Strategic Profitability (With Answers)Document54 pagesCHP 12 - Strategy, Balanced Scorecard, and Strategic Profitability (With Answers)kenchong7150% (1)

- Topic 7 - Absorption & Marginal CostingDocument8 pagesTopic 7 - Absorption & Marginal CostingMuhammad Alif100% (5)

- AQA Business Weekly Revision Guide 2023Document7 pagesAQA Business Weekly Revision Guide 2023DivineNo ratings yet

- Practice Questions and Concepts of The Balanced ScorecardDocument8 pagesPractice Questions and Concepts of The Balanced ScorecardJuan Dela Cruz IIINo ratings yet

- Flexible BudgetDocument30 pagesFlexible BudgetTebaterrorNo ratings yet

- ch01 - Managerial AccountingDocument46 pagesch01 - Managerial AccountingPadlah Riyadi. SE., Ak., CA., MM.No ratings yet

- Managerial AccountingDocument42 pagesManagerial AccountingshamsaNo ratings yet

- L5257 - 1 Introduction 2017Document46 pagesL5257 - 1 Introduction 2017Reza Nursyah PutraNo ratings yet

- Behavioural Economics (Spring 2020) : Andrea Giovannetti Office Hour: Fri (10:30-11:30) Zoom: 8712136666Document43 pagesBehavioural Economics (Spring 2020) : Andrea Giovannetti Office Hour: Fri (10:30-11:30) Zoom: 8712136666SHAMRAIZKHANNo ratings yet

- 2nd Sessional CHN - BBADocument2 pages2nd Sessional CHN - BBASHAMRAIZKHANNo ratings yet

- Income Statement: The Star Logo, and South-Western Are Trademarks Used Herein Under LicenseDocument24 pagesIncome Statement: The Star Logo, and South-Western Are Trademarks Used Herein Under LicenseSHAMRAIZKHANNo ratings yet

- Project Cost Management-1Document17 pagesProject Cost Management-1SHAMRAIZKHANNo ratings yet

- Behavioural Economics (Spring 2020) : HD and Commitment HD in The Field TutorialDocument46 pagesBehavioural Economics (Spring 2020) : HD and Commitment HD in The Field TutorialSHAMRAIZKHANNo ratings yet

- Behavioural Economics (Spring 2020) : Survey Limit of EUT & Prospect Theory I Tutorial On EV and EUTDocument68 pagesBehavioural Economics (Spring 2020) : Survey Limit of EUT & Prospect Theory I Tutorial On EV and EUTSHAMRAIZKHANNo ratings yet

- Gibson Ch05 SM 13eDocument19 pagesGibson Ch05 SM 13eSHAMRAIZKHANNo ratings yet

- Behavioural Economics (Spring 2020) : Prospect Theory and Applications Reference-Point Determination TutorialDocument58 pagesBehavioural Economics (Spring 2020) : Prospect Theory and Applications Reference-Point Determination TutorialSHAMRAIZKHANNo ratings yet

- Behavioural Economics (Spring 2020) Lecture I - IntroductionDocument34 pagesBehavioural Economics (Spring 2020) Lecture I - IntroductionSHAMRAIZKHANNo ratings yet

- Name: Shamraiz Khan Reg No: FA17-BBA-042 Assignment: 1 Date: 04-03-2020Document4 pagesName: Shamraiz Khan Reg No: FA17-BBA-042 Assignment: 1 Date: 04-03-2020SHAMRAIZKHANNo ratings yet

- Gibson10e ch02Document23 pagesGibson10e ch02SHAMRAIZKHANNo ratings yet

- Q1 AnsDocument2 pagesQ1 AnsSHAMRAIZKHANNo ratings yet

- BUS101 Final Exam Summer - FTHE - 2020 (Ver B) - QuestionsDocument16 pagesBUS101 Final Exam Summer - FTHE - 2020 (Ver B) - QuestionsSHAMRAIZKHAN0% (1)

- Chapter 02: Company SummaryDocument4 pagesChapter 02: Company SummarySHAMRAIZKHANNo ratings yet

- BUS101 Final Exam Summer - FTHE - 2020 (Ver B) - QuestionsDocument16 pagesBUS101 Final Exam Summer - FTHE - 2020 (Ver B) - QuestionsSHAMRAIZKHAN0% (1)

- CH 02Document61 pagesCH 02SHAMRAIZKHAN100% (2)

- A Strategic Analysis of A Company in The Wedding IndustryDocument86 pagesA Strategic Analysis of A Company in The Wedding IndustrySHAMRAIZKHANNo ratings yet

- CH 03: Products and Services: ProductDocument1 pageCH 03: Products and Services: ProductSHAMRAIZKHANNo ratings yet

- Write Approved Name of Business Plan Here (Business Plan) : Project Report OnDocument6 pagesWrite Approved Name of Business Plan Here (Business Plan) : Project Report OnSHAMRAIZKHANNo ratings yet

- Chapter No.: 6 Financial Plans: 6.1 Financial Projections: Items Amount in PKRDocument2 pagesChapter No.: 6 Financial Plans: 6.1 Financial Projections: Items Amount in PKRSHAMRAIZKHANNo ratings yet

- Chinese (HUM434) Unit 1 Lesson 07 Unit 1 Lesson 07Document10 pagesChinese (HUM434) Unit 1 Lesson 07 Unit 1 Lesson 07SHAMRAIZKHANNo ratings yet

- Lecturer 17: Buy Side AnalystsDocument8 pagesLecturer 17: Buy Side AnalystsSHAMRAIZKHANNo ratings yet

- Chinese (HUM434) Unit 1 Lesson 08 Unit 1 Lesson 08Document6 pagesChinese (HUM434) Unit 1 Lesson 08 Unit 1 Lesson 08SHAMRAIZKHANNo ratings yet

- Internal and External AuditorsDocument19 pagesInternal and External AuditorsSHAMRAIZKHANNo ratings yet

- CHN Unit 01 Lesson 04Document7 pagesCHN Unit 01 Lesson 04SHAMRAIZKHANNo ratings yet

- Training and Developing EmployeesDocument25 pagesTraining and Developing EmployeesSHAMRAIZKHANNo ratings yet

- Investment BanksDocument8 pagesInvestment BanksSHAMRAIZKHANNo ratings yet

- Corporate GovernanceDocument6 pagesCorporate GovernanceSHAMRAIZKHANNo ratings yet

- Earnings Management Earnings ManagementDocument10 pagesEarnings Management Earnings ManagementSHAMRAIZKHANNo ratings yet

- Week 11, Lecture 1 &2Document20 pagesWeek 11, Lecture 1 &2SHAMRAIZKHANNo ratings yet

- Students Problem Solving Strategies in Problem SoDocument6 pagesStudents Problem Solving Strategies in Problem SoGlen GayagayNo ratings yet

- Wool ProcessingDocument16 pagesWool ProcessingUmar Mohammad MirNo ratings yet

- CV Biographical ReviewDocument3 pagesCV Biographical ReviewOscar Mauricio Carrillo ViverosNo ratings yet

- q2 Week 2-3 Module - (Follow Methods and Procedures & Produce Project or Product)Document7 pagesq2 Week 2-3 Module - (Follow Methods and Procedures & Produce Project or Product)Lovely Sunga-AlboroteNo ratings yet

- Module-Prof Ed - 9Document127 pagesModule-Prof Ed - 9Gabriel Pelicano0% (1)

- Leaders:: Creating An Environment For Exceptional FollowersDocument61 pagesLeaders:: Creating An Environment For Exceptional FollowersYusranNo ratings yet

- General Class Program 2019-2020Document111 pagesGeneral Class Program 2019-2020Ian MooneNo ratings yet

- Is It The Right Time To Have A Population Control Law in India? By: Rajat Sharma and Pooja BaliDocument21 pagesIs It The Right Time To Have A Population Control Law in India? By: Rajat Sharma and Pooja BaliLatest Laws TeamNo ratings yet

- Mirpur University of Science and Technology: Department of Software EngineeringDocument23 pagesMirpur University of Science and Technology: Department of Software EngineeringaliNo ratings yet

- Discussion QuestionsDocument6 pagesDiscussion QuestionsHamza AslamNo ratings yet

- Certification SalinTUBIG CY 2020Document3 pagesCertification SalinTUBIG CY 2020michael ricafortNo ratings yet

- Individual Daily Log and Accomplishment ReportDocument2 pagesIndividual Daily Log and Accomplishment ReportJe-ann H. GonzalesNo ratings yet

- MODULE 2 HRP and HRDDocument9 pagesMODULE 2 HRP and HRDTitus ClementNo ratings yet

- What Is Pre-Writing?: English IvDocument5 pagesWhat Is Pre-Writing?: English IvA Erick Stalin GuerraNo ratings yet

- 2008 Code of EthicsDocument70 pages2008 Code of EthicsdocmabelNo ratings yet

- Education HOD Lalkrishna KhanraDocument4 pagesEducation HOD Lalkrishna Khanrasandip pandeyNo ratings yet

- Achievement Test TOS G10Document1 pageAchievement Test TOS G10Ariel Delos ReyesNo ratings yet

- Projectiden Tificationand Selectio01Document11 pagesProjectiden Tificationand Selectio01Md SolaimanNo ratings yet

- .I International BusinessDocument4 pages.I International Businessdikpalak100% (1)

- Krautkrämer Ultrasonic Transducers: For Flaw Detection and SizingDocument8 pagesKrautkrämer Ultrasonic Transducers: For Flaw Detection and SizingWilliam Cubillos PulidoNo ratings yet

- Chapter 5 - Group DynamicsDocument7 pagesChapter 5 - Group DynamicsLord GrimNo ratings yet

- CVDocument2 pagesCVOana Camelia SamoilaNo ratings yet

- CCM Neutral Write-UpDocument5 pagesCCM Neutral Write-UpniharNo ratings yet

- Foundation of MathematicsDocument3 pagesFoundation of MathematicsJemelyn VergaraNo ratings yet

- MSC MEng Programme 2012 2013Document5 pagesMSC MEng Programme 2012 2013shobziNo ratings yet