You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Coursebook Answers: Answers To Test Yourself QuestionsDocument3 pagesCoursebook Answers: Answers To Test Yourself QuestionsAejaz Mohamed81% (21)

- Pre Operating Cash FlowDocument43 pagesPre Operating Cash FlowCamille ManalastasNo ratings yet

- Krispy Kreme Case StudyDocument4 pagesKrispy Kreme Case StudyMike Crawford100% (1)

- Sap Fi Ecc 6 0 Bootcamp Day 1Document144 pagesSap Fi Ecc 6 0 Bootcamp Day 1Bala Ranganath100% (1)

- Orion Pharma Limited Integrated Annual Report 2019-20 PDFDocument340 pagesOrion Pharma Limited Integrated Annual Report 2019-20 PDFFouzia FarihaNo ratings yet

- Environmental Appraisal of ProjectsDocument27 pagesEnvironmental Appraisal of ProjectsKartik BhartiaNo ratings yet

- Environment AppraisalDocument26 pagesEnvironment AppraisalKartik BhartiaNo ratings yet

- 7 Non Life InsuranceDocument44 pages7 Non Life InsuranceKartik BhartiaNo ratings yet

- 6 Credit CardsDocument77 pages6 Credit CardsKartik BhartiaNo ratings yet

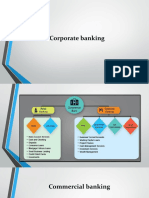

- 4 Corporate BankingDocument31 pages4 Corporate BankingKartik BhartiaNo ratings yet

- 12-Trends in Banking and Insurance MarketingDocument50 pages12-Trends in Banking and Insurance MarketingKartik BhartiaNo ratings yet

- 1-Marketing Financial Products - An IntroductionDocument43 pages1-Marketing Financial Products - An IntroductionKartik BhartiaNo ratings yet

- 10-Mutual FundsDocument69 pages10-Mutual FundsKartik BhartiaNo ratings yet

- 11-Fee-Based ServicesDocument16 pages11-Fee-Based ServicesKartik BhartiaNo ratings yet

- 8-Life InsuranceDocument51 pages8-Life InsuranceKartik BhartiaNo ratings yet

- Profit Planning: Chapter NineDocument89 pagesProfit Planning: Chapter NineAmy SIlverbergNo ratings yet

- Partnership and Piecemeal DistributionDocument46 pagesPartnership and Piecemeal DistributionPadmalochan NayakNo ratings yet

- Chapter 20: Audit of Other Accounts in The Statement of Profit or Loss and Comprehensive IncomeDocument9 pagesChapter 20: Audit of Other Accounts in The Statement of Profit or Loss and Comprehensive IncomeAnna TaylorNo ratings yet

- Journal, Ledger, Trail Balance and Finnancial Statement MCQsDocument5 pagesJournal, Ledger, Trail Balance and Finnancial Statement MCQsNoshair Ali100% (4)

- Corporate Liquidation PDFDocument6 pagesCorporate Liquidation PDFJae DenNo ratings yet

- Test Bank CH 3Document32 pagesTest Bank CH 3Sharmaine Rivera MiguelNo ratings yet

- 3 Stages ECLDocument4 pages3 Stages ECLPappy TresNo ratings yet

- Basics of Accounting and Finance For Small Water SystemsDocument34 pagesBasics of Accounting and Finance For Small Water SystemsRashe FasiNo ratings yet

- Practical Accounting 1: I ExamcoverageDocument12 pagesPractical Accounting 1: I ExamcoverageCharry Ramos0% (2)

- Intro To AccountDocument3 pagesIntro To AccountZahran Alkhairy AzharNo ratings yet

- Working Capital Management Live Project Report by Pranay Jindal in Jindal Steel and PowerDocument83 pagesWorking Capital Management Live Project Report by Pranay Jindal in Jindal Steel and PowerPranay Jindal71% (7)

- Intermediate: AccountingDocument51 pagesIntermediate: AccountingTiến NguyễnNo ratings yet

- EBL Annual Report 2013Document101 pagesEBL Annual Report 2013জয়ন্ত দেবনাথ জয়No ratings yet

- CH 21Document9 pagesCH 21Rica Raditiya0% (1)

- Business Combinations: Electronic Presentations in Microsoft® Powerpoint®Document47 pagesBusiness Combinations: Electronic Presentations in Microsoft® Powerpoint®mattxweb100% (1)

- Unit 3.2modes of Creating Charge FR LoanDocument8 pagesUnit 3.2modes of Creating Charge FR LoanVelankani100% (1)

- Solution Manual Advanced Accounting 11E by Beams 03 Solution Manual Advanced Accounting 11E by Beams 03Document22 pagesSolution Manual Advanced Accounting 11E by Beams 03 Solution Manual Advanced Accounting 11E by Beams 03vvNo ratings yet

- Capital Expenditure Formula Excel TemplateDocument3 pagesCapital Expenditure Formula Excel TemplateKSXNo ratings yet

- Financial Statements and ManagementReportsDocument325 pagesFinancial Statements and ManagementReportsBOCMANAGERNo ratings yet

- Commercial Tree Plantation Business PlanDocument21 pagesCommercial Tree Plantation Business PlanLuyinda SamuelNo ratings yet

- Group AccountingDocument144 pagesGroup AccountingziyuNo ratings yet

- Annual Report 2018Document467 pagesAnnual Report 2018Tasneef ChowdhuryNo ratings yet

- Basic Accounting EquationDocument42 pagesBasic Accounting Equationlily smithNo ratings yet

- Asset Asset Current Asset AssetDocument2 pagesAsset Asset Current Asset AssetNananNo ratings yet

- 11 Acc CH 1 Introduction To Accounting 23-24Document15 pages11 Acc CH 1 Introduction To Accounting 23-24Nathan DavidNo ratings yet