You might also like

- 2 Operate A Spreadsheet Application AdvanceDocument32 pages2 Operate A Spreadsheet Application Advanceapi-247871582No ratings yet

- Managerial Economics Basics at GITAM UniversityDocument11 pagesManagerial Economics Basics at GITAM Universitysiva883No ratings yet

- Expert Systems: Unit-VDocument24 pagesExpert Systems: Unit-VasarvigaNo ratings yet

- Data and Information ManagementDocument6 pagesData and Information ManagementPraveen TrivediNo ratings yet

- Create Tables in Word with Less than 40 CharactersDocument3 pagesCreate Tables in Word with Less than 40 CharactersSharmila SathiaselanNo ratings yet

- Social, Ethical, and Legal Issues in Information Systems: Chapter FourDocument39 pagesSocial, Ethical, and Legal Issues in Information Systems: Chapter FourRyanNo ratings yet

- Cost Theory and Estimation (Group 4)Document48 pagesCost Theory and Estimation (Group 4)Angelica Mae ReyesNo ratings yet

- Statistical Quality ControlDocument35 pagesStatistical Quality ControlHassaan Naeem100% (1)

- Module 1 Overview of Management ScienceDocument10 pagesModule 1 Overview of Management ScienceRaphael GalitNo ratings yet

- M.COM PART II Advanced Cost Accounting Question BankDocument5 pagesM.COM PART II Advanced Cost Accounting Question BankPrathamesh ChawanNo ratings yet

- Production and Cost Analysis GuideDocument24 pagesProduction and Cost Analysis GuideSri HimajaNo ratings yet

- Quiz 1 Ia2Document4 pagesQuiz 1 Ia2Angelica NilloNo ratings yet

- Chapter 25 - Production and GrowthDocument22 pagesChapter 25 - Production and GrowthvanvobboyNo ratings yet

- Chapter 03 - The Accounting Cycle: Capturing Economic EventsDocument143 pagesChapter 03 - The Accounting Cycle: Capturing Economic EventsElio BazNo ratings yet

- Employee share option and SARs expense calculationDocument13 pagesEmployee share option and SARs expense calculationPHI NGUYEN HOANGNo ratings yet

- Lesson 1 Introduction To Xero: Cloud ComputingDocument17 pagesLesson 1 Introduction To Xero: Cloud ComputingLeah ManalangNo ratings yet

- The Origins of SoftwareDocument7 pagesThe Origins of SoftwareMay Ann Agcang SabelloNo ratings yet

- Data Warehouse Concepts PresentationDocument60 pagesData Warehouse Concepts PresentationThirumal Selvaraj100% (1)

- Joint Product L7 UpdatedDocument14 pagesJoint Product L7 Updatedviony catelinaNo ratings yet

- Transaction Processing SystemsDocument7 pagesTransaction Processing SystemsKarla MaeNo ratings yet

- Cost Estimation and Analysis TechniquesDocument9 pagesCost Estimation and Analysis TechniquesPATRICIA PEREZNo ratings yet

- Assurance and Non Assurance ServicesDocument4 pagesAssurance and Non Assurance ServicesAnne Waban100% (1)

- Analyze Factory Overhead VariancesDocument8 pagesAnalyze Factory Overhead VariancesLovely Mae LariosaNo ratings yet

- Demand and Supply AssignmentDocument3 pagesDemand and Supply AssignmentnailajazNo ratings yet

- BA 328 - Ch5 - Process Selection, Design, and AnalysisDocument16 pagesBA 328 - Ch5 - Process Selection, Design, and AnalysisBeboy TorregosaNo ratings yet

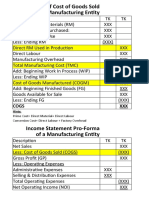

- Statement of Cost of Goods Sold of A Manufacturing Entity: Cogs XXXDocument1 pageStatement of Cost of Goods Sold of A Manufacturing Entity: Cogs XXXCasanovicNo ratings yet

- t3. Measuring The Cost of LivingDocument26 pagest3. Measuring The Cost of Livingmimi96No ratings yet

- Cost Theory and Estimation PDFDocument14 pagesCost Theory and Estimation PDFAngie BobierNo ratings yet

- Chapter 11 - Network ModelsDocument22 pagesChapter 11 - Network ModelsAbo Fawaz100% (1)

- LEASE ACCOUNTING ESSENTIALSDocument6 pagesLEASE ACCOUNTING ESSENTIALSIts meh SushiNo ratings yet

- Variable & Absorption Costing LectureDocument11 pagesVariable & Absorption Costing LectureElisha Dhowry PascualNo ratings yet

- 18 x12 ABC A Traditional Cost Accounting (MAS) BobadillaDocument12 pages18 x12 ABC A Traditional Cost Accounting (MAS) BobadillaAnnaNo ratings yet

- CHAPTER 4 - System Design N PDFDocument75 pagesCHAPTER 4 - System Design N PDFJia MingNo ratings yet

- ECON1B03 Exam 2012fall SolutionDocument8 pagesECON1B03 Exam 2012fall SolutionIshahNo ratings yet

- Chapter 06 Intercompany Profit Transactions Plant AssetsDocument28 pagesChapter 06 Intercompany Profit Transactions Plant AssetsJonathan VidarNo ratings yet

- Decision Analysis TechniquesDocument8 pagesDecision Analysis TechniquesLumumba KuyelaNo ratings yet

- Gbagada General HospitalDocument1 pageGbagada General HospitalChijioke PaschalNo ratings yet

- Practice Set Audit of PPEDocument1 pagePractice Set Audit of PPEAlexis BagongonNo ratings yet

- Topic: The Importance of Logic in Business: Period: Prelim Time Frame: 6 HoursDocument41 pagesTopic: The Importance of Logic in Business: Period: Prelim Time Frame: 6 HoursPatricia Jane CabangNo ratings yet

- Managerial Accounting: Tools For Business Decision-MakingDocument56 pagesManagerial Accounting: Tools For Business Decision-MakingdavidNo ratings yet

- Chapter 2 - Gross Estate PDFDocument6 pagesChapter 2 - Gross Estate PDFVanessa Castor GasparNo ratings yet

- Far Quiz 2 Final W AnswersDocument6 pagesFar Quiz 2 Final W AnswersGia HipolitoNo ratings yet

- Introduction To Management Accounting: Asst Prof. Jonlen DesaDocument22 pagesIntroduction To Management Accounting: Asst Prof. Jonlen DesaAryanSainiNo ratings yet

- Rubric For Reporting in PrinciplesDocument1 pageRubric For Reporting in PrinciplesMarian KayeNo ratings yet

- Business CombinationDocument21 pagesBusiness CombinationSamNo ratings yet

- CH04 - Revenue CycleDocument45 pagesCH04 - Revenue CycleIan Vincent Lazaga MaribaoNo ratings yet

- Joint Product by ProductDocument31 pagesJoint Product by ProductMahfuzulNo ratings yet

- Difference between absorption and variable costingDocument3 pagesDifference between absorption and variable costingJerrizza RamirezNo ratings yet

- Absorption CostingDocument2 pagesAbsorption CostingbanglauserNo ratings yet

- Queueing TheoryDocument45 pagesQueueing TheoryManas KumarNo ratings yet

- Managerial Accounting Solutions Ch3Document12 pagesManagerial Accounting Solutions Ch3Marwan Al-Asbahi75% (4)

- Statement of Cashflows For The Year Ended XYZ Cash Flows From Operating ActivitiesDocument27 pagesStatement of Cashflows For The Year Ended XYZ Cash Flows From Operating ActivitieszeeshanNo ratings yet

- CISM SyllabusDocument4 pagesCISM SyllabusBirhanNo ratings yet

- CHAPTER 10: Capital Budgeting Techniques: Annual Net IncomeDocument2 pagesCHAPTER 10: Capital Budgeting Techniques: Annual Net IncomeSeresa EstrellasNo ratings yet

- Decision Making Under Uncertainty Decision TreeDocument32 pagesDecision Making Under Uncertainty Decision TreeEko Nopianto100% (1)

- Cfas Paa 1 ReviewerDocument44 pagesCfas Paa 1 ReviewerGleah Mae GonzagaNo ratings yet

- Process Costing and Hybrid Product-Costing SystemsDocument17 pagesProcess Costing and Hybrid Product-Costing SystemsWailNo ratings yet

- Module 2 Sub Mod 2 Standard Costing and Material Variance FinalDocument31 pagesModule 2 Sub Mod 2 Standard Costing and Material Variance Finalmaheshbendigeri5945No ratings yet

- Concept of ProductionDocument29 pagesConcept of ProductionJon SagabayNo ratings yet

- Colander ch09 Production&CostsIDocument71 pagesColander ch09 Production&CostsIJenil BetitoNo ratings yet

- Profit Maximization in Various Market Structure: de Jesus, Lerrie Quejada, Abegail Vilog, LheamDocument32 pagesProfit Maximization in Various Market Structure: de Jesus, Lerrie Quejada, Abegail Vilog, LheamJohn Stephen EusebioNo ratings yet

- ECOMANDocument37 pagesECOMANJohn Stephen EusebioNo ratings yet

- The PH From Other Countries, and Overseas Businesses and Consumers Buy PH Products Known AsDocument6 pagesThe PH From Other Countries, and Overseas Businesses and Consumers Buy PH Products Known AsJohn Stephen EusebioNo ratings yet

- ECOMAN Profit MaximizationDocument6 pagesECOMAN Profit MaximizationJohn Stephen EusebioNo ratings yet

- What is Economic ActivityDocument7 pagesWhat is Economic ActivityJohn Stephen EusebioNo ratings yet

- Ecoman AssignmentDocument11 pagesEcoman AssignmentJohn Stephen EusebioNo ratings yet

- Gross Domestic Product (GDP)Document10 pagesGross Domestic Product (GDP)John Stephen EusebioNo ratings yet

- Assignment in R.P.H: Submitted By: John Stephen S. Eusebio Submitted To: Ms. Melinda San JuanDocument3 pagesAssignment in R.P.H: Submitted By: John Stephen S. Eusebio Submitted To: Ms. Melinda San JuanJohn Stephen EusebioNo ratings yet

- Assignment in R.P.H: Submitted byDocument4 pagesAssignment in R.P.H: Submitted byJohn Stephen EusebioNo ratings yet

- Is It Inevitable That The Monopoly Prices Are Higher Than The Competitive PriceDocument17 pagesIs It Inevitable That The Monopoly Prices Are Higher Than The Competitive PriceMuhammad AbdullahNo ratings yet

- MSU College of Business Administration Short-Term Non-Routine DecisionsDocument6 pagesMSU College of Business Administration Short-Term Non-Routine Decisionskochanay oya-oyNo ratings yet

- Profit MaximazationDocument36 pagesProfit MaximazationFrank BabuNo ratings yet

- Chap V Market StructureDocument36 pagesChap V Market StructureDaniel YirdawNo ratings yet

- Industry Economics Market ModelsDocument10 pagesIndustry Economics Market ModelsrosheelNo ratings yet

- Topic 8 - Firms in Competitive Markets PDFDocument32 pagesTopic 8 - Firms in Competitive Markets PDF郑伟权No ratings yet

- Shut Down PriceDocument14 pagesShut Down PriceNoor NabiNo ratings yet

- Apree Midterms MNGT Acctng PDF FreeDocument36 pagesApree Midterms MNGT Acctng PDF Freejeon jkNo ratings yet

- Perfect Competition Model: Part 3/3Document68 pagesPerfect Competition Model: Part 3/3subNo ratings yet

- A Review in Managerial Economics: Prepared By: Jeams E. VidalDocument8 pagesA Review in Managerial Economics: Prepared By: Jeams E. Vidaljeams vidalNo ratings yet

- Market Structures & Price DeterminationDocument52 pagesMarket Structures & Price Determinationghosh71No ratings yet

- Perfect Competition: Answers To The Review QuizzesDocument18 pagesPerfect Competition: Answers To The Review Quizzesrajan20202000No ratings yet

- Assignment 8Document8 pagesAssignment 8eric stevanusNo ratings yet

- Snazzlefrags Microeconomics Clep Study NotesDocument4 pagesSnazzlefrags Microeconomics Clep Study NotesEllenNo ratings yet

- Econ 107Document14 pagesEcon 107hazem 00No ratings yet

- ACFrOgAMnktC8b01ely7fyjtYz-48iVFqaYfEYb8Mpky5ihkpwaGsnvIyuRhRT6xlBhJv-Mh0UALByl0AIN40GJir7u4in kYpXpEQr2aBFDImeR j2q7U5RP0lumUt7kU1S1gNAmjqEEIyuDHPMDocument36 pagesACFrOgAMnktC8b01ely7fyjtYz-48iVFqaYfEYb8Mpky5ihkpwaGsnvIyuRhRT6xlBhJv-Mh0UALByl0AIN40GJir7u4in kYpXpEQr2aBFDImeR j2q7U5RP0lumUt7kU1S1gNAmjqEEIyuDHPMRosevel C. IliganNo ratings yet

- Chapter 7 Market Structure: Perfect Competition: Economics For Managers, 3e (Farnham)Document25 pagesChapter 7 Market Structure: Perfect Competition: Economics For Managers, 3e (Farnham)ForappForapp100% (1)

- MasDocument20 pagesMasMarie AranasNo ratings yet

- Explicit Costs Implicit Costs Fixed Costs Variable Costs Total Costs Average Fixed Costs Average Variable Costs Average Total Costs Marginal CostsDocument11 pagesExplicit Costs Implicit Costs Fixed Costs Variable Costs Total Costs Average Fixed Costs Average Variable Costs Average Total Costs Marginal CostsZulaikha RazaliNo ratings yet

- Micro Economics:market Structures.Document33 pagesMicro Economics:market Structures.Manal AftabNo ratings yet

- Differential Cost Analysis Relevant CostingDocument10 pagesDifferential Cost Analysis Relevant CostingBSIT 1A Yancy CaliganNo ratings yet

- Price Determination Under Perfect CompetitionDocument16 pagesPrice Determination Under Perfect CompetitionShantnu SoodNo ratings yet

- Basic Economics 1Document27 pagesBasic Economics 1kashifzieNo ratings yet

- Tucker ch08 PDFDocument29 pagesTucker ch08 PDFSudhagar KingNo ratings yet

- Relevant Costing With Highlighted Answer KeyDocument32 pagesRelevant Costing With Highlighted Answer KeyRed Christian Palustre0% (1)

- Non Routine Decisions AnswerDocument9 pagesNon Routine Decisions AnswerCindy CrausNo ratings yet

- Economics: 讲师: CherieDocument306 pagesEconomics: 讲师: CherieEvelyn YangNo ratings yet

- Managerial Economics Solution 1Document10 pagesManagerial Economics Solution 1GARUIS MELINo ratings yet

- ch5 PDFDocument164 pagesch5 PDFBeri Z Hunter75% (4)

- CH 12Document39 pagesCH 12Bobby513No ratings yet