You might also like

- Quantitative Finance - Module 4 CQFDocument18 pagesQuantitative Finance - Module 4 CQFBruce HaydonNo ratings yet

- Schaum's Outline of Bookkeeping and Accounting, Fourth EditionFrom EverandSchaum's Outline of Bookkeeping and Accounting, Fourth EditionRating: 5 out of 5 stars5/5 (1)

- Schaum's Outline of Principles of Accounting I, Fifth EditionFrom EverandSchaum's Outline of Principles of Accounting I, Fifth EditionRating: 5 out of 5 stars5/5 (3)

- CBMEC 2 Strategic Management 2021 Syllabus 1Document15 pagesCBMEC 2 Strategic Management 2021 Syllabus 1Ayame Kusuragi100% (1)

- Calculo, Renta, Tiempo en Funcion Del Monto y V.A.Document15 pagesCalculo, Renta, Tiempo en Funcion Del Monto y V.A.Victor López100% (2)

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineNo ratings yet

- A Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionFrom EverandA Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionNo ratings yet

- J.K. Lasser's Small Business Taxes 2007: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2007: Your Complete Guide to a Better Bottom LineNo ratings yet

- A Comparative Analysis of Tax Administration in Asia and the Pacific: 2020 EditionFrom EverandA Comparative Analysis of Tax Administration in Asia and the Pacific: 2020 EditionNo ratings yet

- Finding Balance 2016: Benchmarking the Performance of State-Owned Enterprise in Island CountriesFrom EverandFinding Balance 2016: Benchmarking the Performance of State-Owned Enterprise in Island CountriesNo ratings yet

- Balance Sheet StructuresFrom EverandBalance Sheet StructuresAnthony N BirtsNo ratings yet

- A Comparative Analysis of Tax Administration in Asia and the Pacific—Sixth EditionFrom EverandA Comparative Analysis of Tax Administration in Asia and the Pacific—Sixth EditionNo ratings yet

- Financial Management: Reference Book Study Guide ACCA CPA CA CIMA BBA MBA: A Comprehensive GuideFrom EverandFinancial Management: Reference Book Study Guide ACCA CPA CA CIMA BBA MBA: A Comprehensive GuideNo ratings yet

- Dividend Growth Investing: A Step-by-Step Guide to Building a Dividend Portfolio for Early RetirementFrom EverandDividend Growth Investing: A Step-by-Step Guide to Building a Dividend Portfolio for Early RetirementNo ratings yet

- Industrial Enterprises Act 2020 (2076): A brief Overview and Comparative AnalysisFrom EverandIndustrial Enterprises Act 2020 (2076): A brief Overview and Comparative AnalysisNo ratings yet

- Dividend Investing: A Beginner's Guide: Learn How to Earn Passive Income from Dividend StocksFrom EverandDividend Investing: A Beginner's Guide: Learn How to Earn Passive Income from Dividend StocksNo ratings yet

- Reforms, Opportunities, and Challenges for State-Owned EnterprisesFrom EverandReforms, Opportunities, and Challenges for State-Owned EnterprisesNo ratings yet

- Braced for Impact: Reforming Kazakhstan's National Financial Holding for Development Effectiveness and Market CreationFrom EverandBraced for Impact: Reforming Kazakhstan's National Financial Holding for Development Effectiveness and Market CreationNo ratings yet

- A Comparative Analysis of Tax Administration in Asia and the Pacific-Seventh EditionFrom EverandA Comparative Analysis of Tax Administration in Asia and the Pacific-Seventh EditionNo ratings yet

- How to Retire Early on Dividends: Dividend Growth Machine: Mastering the Art of Maximizing Returns Through Dividend InvestingFrom EverandHow to Retire Early on Dividends: Dividend Growth Machine: Mastering the Art of Maximizing Returns Through Dividend InvestingNo ratings yet

- The Handbook for Reading and Preparing Proxy Statements: A Guide to the SEC Disclosure Rules for Executive and Director Compensation, 6th EditionFrom EverandThe Handbook for Reading and Preparing Proxy Statements: A Guide to the SEC Disclosure Rules for Executive and Director Compensation, 6th EditionNo ratings yet

- Principles of Cash Flow Valuation: An Integrated Market-Based ApproachFrom EverandPrinciples of Cash Flow Valuation: An Integrated Market-Based ApproachRating: 3 out of 5 stars3/5 (3)

- Financial Accounting - Want to Become Financial Accountant in 30 Days?From EverandFinancial Accounting - Want to Become Financial Accountant in 30 Days?Rating: 3.5 out of 5 stars3.5/5 (2)

- Private Sector Operations in 2019: Report on Development EffectivenessFrom EverandPrivate Sector Operations in 2019: Report on Development EffectivenessNo ratings yet

- Fiscal Decentralization Reform in Cambodia: Progress over the Past Decade and OpportunitiesFrom EverandFiscal Decentralization Reform in Cambodia: Progress over the Past Decade and OpportunitiesNo ratings yet

- A Investment Platform for Future: Self Help a Self Operating BankingFrom EverandA Investment Platform for Future: Self Help a Self Operating BankingNo ratings yet

- The Role of The Stakeholder in The Quality Improvement of An OrganizationDocument11 pagesThe Role of The Stakeholder in The Quality Improvement of An OrganizationAyame KusuragiNo ratings yet

- Bryanna Christopher B C: Resume Objective ContactDocument1 pageBryanna Christopher B C: Resume Objective ContactAyame KusuragiNo ratings yet

- Winter Sales Proposal by SlidesgoDocument12 pagesWinter Sales Proposal by SlidesgoAyame KusuragiNo ratings yet

- AC 4101 SyllabusDocument16 pagesAC 4101 SyllabusAyame KusuragiNo ratings yet

- SSRN Id26238Document21 pagesSSRN Id26238Ayame KusuragiNo ratings yet

- CBMEC2 Course SequenceDocument1 pageCBMEC2 Course SequenceAyame KusuragiNo ratings yet

- AC 4103 OBEdized SyllabusDocument21 pagesAC 4103 OBEdized SyllabusAyame KusuragiNo ratings yet

- Country Continent GDP (Millions of US$)Document4 pagesCountry Continent GDP (Millions of US$)Ayame KusuragiNo ratings yet

- 2019 Petron Annual Report FINALDocument106 pages2019 Petron Annual Report FINALAyame KusuragiNo ratings yet

- Country Continent GDP (Millions of US$)Document3 pagesCountry Continent GDP (Millions of US$)Ayame KusuragiNo ratings yet

- Total Result 45,311,476Document9 pagesTotal Result 45,311,476Ayame KusuragiNo ratings yet

- Revision Del Archivo Permanente de AdrisaDocument3 pagesRevision Del Archivo Permanente de AdrisaMiguel Ivan PosadaNo ratings yet

- Actividad 2. Simulación de Estados FinancierosDocument7 pagesActividad 2. Simulación de Estados FinancierosruthNo ratings yet

- University of Kelaniya: Viva Voice Presentation On Business InternshipDocument14 pagesUniversity of Kelaniya: Viva Voice Presentation On Business InternshipAsiri KasunjithNo ratings yet

- Informe de Practicas CETPRO PUNODocument111 pagesInforme de Practicas CETPRO PUNOKarloz Velasquez HerzeleidNo ratings yet

- COMPLAINT 2nd AMENDED - Filed Jul 14 04Document25 pagesCOMPLAINT 2nd AMENDED - Filed Jul 14 04Jon DruckerNo ratings yet

- Lec 3Document7 pagesLec 3ahmedgalalabdalbaath2003No ratings yet

- Golden Pickaxe - Setup GuideDocument127 pagesGolden Pickaxe - Setup Guideelarabnews478No ratings yet

- EncuestadorDocument16 pagesEncuestadorJorge Alejandro PonceNo ratings yet

- ACTA de Entrega de CargoDocument4 pagesACTA de Entrega de CargoKATY CHIRINOSNo ratings yet

- (教學) PayMe轉賬至八達通App - Zakumo 資訊情報Document5 pages(教學) PayMe轉賬至八達通App - Zakumo 資訊情報Lee HomeuseNo ratings yet

- Additional Practical Problems-5Document3 pagesAdditional Practical Problems-5Ayush Kumar XIth classNo ratings yet

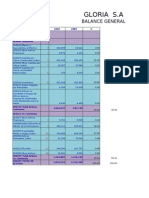

- Gloria S.ADocument6 pagesGloria S.AcomequitNo ratings yet

- Bab 14Document83 pagesBab 14Dias Farenzo PuthNo ratings yet

- FS PT Acset Indonusa TBK 31 Maret 2018Document87 pagesFS PT Acset Indonusa TBK 31 Maret 2018yani andriyaniNo ratings yet

- Olin Finance Club Interview Questions & AnswersDocument20 pagesOlin Finance Club Interview Questions & AnswersSriram ThwarNo ratings yet

- Seminario de Investigacion Dayana Ef AvanceeDocument65 pagesSeminario de Investigacion Dayana Ef AvanceePablo Antonio Rivera MartínezNo ratings yet

- Categorizacion Del ImpuestoDocument33 pagesCategorizacion Del Impuestoronald mafriNo ratings yet

- Ejercicio Contab. Vi SemestreDocument9 pagesEjercicio Contab. Vi Semestredana sofia baez diazNo ratings yet

- NYDA AR 2012 Low ResDocument132 pagesNYDA AR 2012 Low ResNqabisa MtwesiNo ratings yet

- Trabajo Final Bolsa de ValoresDocument15 pagesTrabajo Final Bolsa de ValoresFabián HolnessNo ratings yet

- Ratios LPVDocument22 pagesRatios LPVPuente NNo ratings yet

- SSS Loan Transmittal 2018Document1 pageSSS Loan Transmittal 2018A BNo ratings yet

- Act. 5 Conciliacion Bancaria - Galvan - Sosa - Armando FidelDocument15 pagesAct. 5 Conciliacion Bancaria - Galvan - Sosa - Armando FidelArmando Galvan SosaNo ratings yet

- Resumen PlasticsacksDocument6 pagesResumen PlasticsacksAngelica VegaNo ratings yet

- Elementos de La Sociedad AnónimaDocument3 pagesElementos de La Sociedad AnónimaFanki PankiNo ratings yet

- Case Study - Kelompok 3Document10 pagesCase Study - Kelompok 3elida wenNo ratings yet

- Adopcion Por Primera Vez de Las Normas Internacionales de Informacion - Niif 1Document17 pagesAdopcion Por Primera Vez de Las Normas Internacionales de Informacion - Niif 1Allison CartolinNo ratings yet

- Copia de Nomina 2da de Enero 2017 Epsk - C-1Document15 pagesCopia de Nomina 2da de Enero 2017 Epsk - C-1Felipe RangelNo ratings yet