You might also like

- Audit Manual Version 7Document276 pagesAudit Manual Version 7Tousief Naqvi50% (2)

- Participant Workbook-ISO 9001 - 2015-Issue 02 Rev 03 Nov 2022-3Document52 pagesParticipant Workbook-ISO 9001 - 2015-Issue 02 Rev 03 Nov 2022-3Jadesh ChandranNo ratings yet

- Getting Past NODocument1 pageGetting Past NONoel KlNo ratings yet

- SAMA BCM Framework - Continuity and ResilienceDocument36 pagesSAMA BCM Framework - Continuity and ResiliencechanchalNo ratings yet

- Raouf N Effect of ISO9001-2015 On Q1Document34 pagesRaouf N Effect of ISO9001-2015 On Q1jamil voraNo ratings yet

- PRMG Course - Project Planning BookDocument88 pagesPRMG Course - Project Planning Bookmaryam refaat100% (2)

- Development of Overall Audit StrategyDocument4 pagesDevelopment of Overall Audit StrategyPhrexilyn PajarilloNo ratings yet

- Software Process ImprovementDocument42 pagesSoftware Process ImprovementManmay MahurtaleNo ratings yet

- Project ManagementDocument18 pagesProject ManagementniniashashNo ratings yet

- PRINCE2 Foundation Essentials - NoDocument24 pagesPRINCE2 Foundation Essentials - NoLayar KayarNo ratings yet

- Agenda IRIS Advanced en OnlineDocument5 pagesAgenda IRIS Advanced en OnlineDelong KongNo ratings yet

- Chapter 2 Issues in Ex-Ante and Ex-Post Evaluations: Outline of This ChapterDocument86 pagesChapter 2 Issues in Ex-Ante and Ex-Post Evaluations: Outline of This ChapterReashiela LucenaNo ratings yet

- Audit Process Flowchart MC PDFDocument1 pageAudit Process Flowchart MC PDFDemi BangayanNo ratings yet

- Appraisals ReportDocument11 pagesAppraisals ReportKevinNo ratings yet

- Risk AssessmentDocument3 pagesRisk Assessmentsalman100% (1)

- ISO 14001:2015-Environmental Management Systems: Md. Sahadat HossainDocument56 pagesISO 14001:2015-Environmental Management Systems: Md. Sahadat HossainPinku KhanNo ratings yet

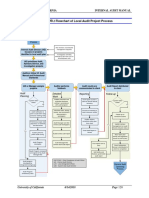

- 6000 Appendix 6000.: 2 Flowchart of Local Audit Project ProcessDocument1 page6000 Appendix 6000.: 2 Flowchart of Local Audit Project ProcessNiken RindasariNo ratings yet

- Initiating The ProjectDocument46 pagesInitiating The ProjectChris KokNo ratings yet

- Week 1 - Project Management PlanDocument6 pagesWeek 1 - Project Management PlanPriyanka DevunuriNo ratings yet

- Chapter 6 - Strategic ImplementationDocument14 pagesChapter 6 - Strategic ImplementationTú ÂnNo ratings yet

- Bqs Asq Lpa Overview 2 3 2017 Rev 11 PDFDocument48 pagesBqs Asq Lpa Overview 2 3 2017 Rev 11 PDFelyesNo ratings yet

- Cmmi Project ManagementDocument35 pagesCmmi Project ManagementHajirah ZarNo ratings yet

- Chapter24 - 1 Mod Completing Rev CiDocument50 pagesChapter24 - 1 Mod Completing Rev CiSufia Nur KamilaNo ratings yet

- Kaizen Blizt - Cost Transformation ProgramDocument23 pagesKaizen Blizt - Cost Transformation ProgramSaid Abu khaulaNo ratings yet

- PM GUIDE 03 End To End Project Delivery FrameworkDocument31 pagesPM GUIDE 03 End To End Project Delivery Frameworktimur.bartashNo ratings yet

- Report Writing For BCP Audit: A General GuideDocument29 pagesReport Writing For BCP Audit: A General GuideGreg Ezeilo100% (2)

- ABC Process Mapping and RBT Quality PlanningDocument97 pagesABC Process Mapping and RBT Quality Planningtony sNo ratings yet

- Zero Defect and Zero Effect: - Maturity ModelDocument8 pagesZero Defect and Zero Effect: - Maturity ModelYash BelaniNo ratings yet

- Project Cost Management: Bilguundemberel.M PMI Mongolia Chapter 25 JAN, 2020Document95 pagesProject Cost Management: Bilguundemberel.M PMI Mongolia Chapter 25 JAN, 2020ЗОЛЗАЯА ГантулгаNo ratings yet

- Implementing The COSO 2013's New 17 Principles in AuditDocument23 pagesImplementing The COSO 2013's New 17 Principles in Audittunlinoo.067433100% (1)

- Day 3Document61 pagesDay 3naltousNo ratings yet

- Project Phases and MilestonesDocument4 pagesProject Phases and MilestonesUmer FarooqNo ratings yet

- SPM Chapter7Document56 pagesSPM Chapter7KidusNo ratings yet

- Turnaround Management: Connected Excellence in All We DoDocument8 pagesTurnaround Management: Connected Excellence in All We Doimafish100% (1)

- Virender Singh AccentureDocument17 pagesVirender Singh Accenturejaganmohan29No ratings yet

- ISO 9001 2015 Management Review Webinar Presentation DeckDocument19 pagesISO 9001 2015 Management Review Webinar Presentation DeckHernane BiniNo ratings yet

- Project Management MethodologyDocument13 pagesProject Management MethodologyMoeslem HaqNo ratings yet

- Audit Process: - Phase 1: Audit Plan - Phase 2: Audit Implementation - Phase 3: Audit CompletionDocument5 pagesAudit Process: - Phase 1: Audit Plan - Phase 2: Audit Implementation - Phase 3: Audit CompletionMai LinhNo ratings yet

- Audit Manual Version 5Document247 pagesAudit Manual Version 5MahediNo ratings yet

- Country Assistance Evaluation at OEDDocument20 pagesCountry Assistance Evaluation at OEDRose Diane CabiscuelasNo ratings yet

- Part A: Objectives What Is Expected of Me in My Role?Document7 pagesPart A: Objectives What Is Expected of Me in My Role?Aang WidiaNo ratings yet

- IATF OER Checklist Along With Attendance Sheet 2021 07 EditionDocument11 pagesIATF OER Checklist Along With Attendance Sheet 2021 07 EditionAshok PanchalNo ratings yet

- Chap 4 - Audit in Automated EnvironmentDocument19 pagesChap 4 - Audit in Automated EnvironmentTejas jogadeNo ratings yet

- GL CreationDocument38 pagesGL CreationMK YNo ratings yet

- Sistema de Gobierno en Base A Factores de GobiernoDocument285 pagesSistema de Gobierno en Base A Factores de Gobiernoyoao007No ratings yet

- PM GUIDE 03 End To End Project Delivery FrameworkDocument32 pagesPM GUIDE 03 End To End Project Delivery FrameworkBAHIJNo ratings yet

- Candidate InformationDocument6 pagesCandidate InformationMarius BuysNo ratings yet

- OpCo Audit ProgramDocument11 pagesOpCo Audit ProgramMarco Giovani ZancanellaNo ratings yet

- Group # 09, PresentationDocument24 pagesGroup # 09, PresentationMuhammad NaumanNo ratings yet

- Formal Clat Control PlanDocument1 pageFormal Clat Control PlanenjoythedocsNo ratings yet

- ABCD Risk Management TeachingDocument16 pagesABCD Risk Management TeachingSherweet A. AlsaadanyNo ratings yet

- TR006 NQA UK Client Transition Gap Analysis Tool ISO 9001 Rev3 2 11 2015 Interactive - CZ PDFDocument8 pagesTR006 NQA UK Client Transition Gap Analysis Tool ISO 9001 Rev3 2 11 2015 Interactive - CZ PDFriskihNo ratings yet

- PM CH 2Document44 pagesPM CH 2jamshedjaved4673No ratings yet

- Imprest Funds & ReplenishmentsDocument38 pagesImprest Funds & ReplenishmentsraghavNo ratings yet

- Chapter+2+ +Audit+Planning+and+Internal+Controls+Considerations+ +part+1Document16 pagesChapter+2+ +Audit+Planning+and+Internal+Controls+Considerations+ +part+1Dan MorettoNo ratings yet

- Gerbang Nilai Presentation - Ir - HizamuldinDocument39 pagesGerbang Nilai Presentation - Ir - HizamuldinAiffah Mohammed100% (1)

- BPM - 3 - HalaDocument12 pagesBPM - 3 - HalaAsadulla KhanNo ratings yet

- UADP IA TrainingDocument22 pagesUADP IA Trainingsreeraj88No ratings yet

- Financial Statement Analysis - CODocument4 pagesFinancial Statement Analysis - COHaardik GandhiNo ratings yet

- Sample 5Document2 pagesSample 5Josephine LimNo ratings yet

- Sample 4Document1 pageSample 4Josephine LimNo ratings yet

- Sample 1Document2 pagesSample 1Josephine LimNo ratings yet

- Sample 2Document2 pagesSample 2Josephine LimNo ratings yet

- Sample 3Document2 pagesSample 3Josephine LimNo ratings yet

- PPEDisposals PM 04 DispTemplateDocument1 pagePPEDisposals PM 04 DispTemplateJosephine LimNo ratings yet

- PPEDisposals PM 08 SLExtractDocument1 pagePPEDisposals PM 08 SLExtractJosephine LimNo ratings yet

- PPEDisposals PM 07 BankStmtsDocument3 pagesPPEDisposals PM 07 BankStmtsJosephine LimNo ratings yet

- PPEDisposals PM 09 RFSCHDocument1 pagePPEDisposals PM 09 RFSCHJosephine LimNo ratings yet

- 10 - AF - L1 - Flow of The Audit - LM - 02 - Five PhasesDocument1 page10 - AF - L1 - Flow of The Audit - LM - 02 - Five PhasesJosephine LimNo ratings yet

- Study Guide AFF v2022Document22 pagesStudy Guide AFF v2022Josephine LimNo ratings yet

- Fiqws 10108 - Summary of Young Immigrants RevisedDocument3 pagesFiqws 10108 - Summary of Young Immigrants Revisedapi-490001116No ratings yet

- IEEE STD IEEE-1346-1998 - IEEE Recommenden Practice For Ev. EPS. Compability PDFDocument45 pagesIEEE STD IEEE-1346-1998 - IEEE Recommenden Practice For Ev. EPS. Compability PDFCarlos Gabriel Quintero RodríguezNo ratings yet

- Engineering Desgin Process Pringle ProjectDocument7 pagesEngineering Desgin Process Pringle Projectapi-310020492No ratings yet

- WebSphere Application Server For Developers V7Document256 pagesWebSphere Application Server For Developers V7Jose Luis Balmaseda FrancoNo ratings yet

- Asimov FrustrationDocument1 pageAsimov FrustrationSilviu PaduraruNo ratings yet

- Bow Valley Clean Air Society NewsletterDocument2 pagesBow Valley Clean Air Society NewsletterSTOP THE QUARRYNo ratings yet

- Working With RTFX PackDocument4 pagesWorking With RTFX PackpapuNo ratings yet

- Lesson Plan Weight Management and Physical ActivityDocument5 pagesLesson Plan Weight Management and Physical Activityapi-269378468No ratings yet

- May Sagot Na To Eto Yung Magpapakita GuysDocument60 pagesMay Sagot Na To Eto Yung Magpapakita GuysDenzel Ivan PalatinoNo ratings yet

- Architect Competency Profile: Description of WorkDocument7 pagesArchitect Competency Profile: Description of WorkRahmi Andrianna PutriNo ratings yet

- As ISO 10993.9-2002 Biological Evaluation of Medical Devices Framework For Identification and QuantificationDocument8 pagesAs ISO 10993.9-2002 Biological Evaluation of Medical Devices Framework For Identification and QuantificationSAI Global - APACNo ratings yet

- Bergson and The Metaphysics of TimeDocument9 pagesBergson and The Metaphysics of TimeRob Boileau100% (1)

- Sinumerik 840d SL EnsaDocument508 pagesSinumerik 840d SL EnsaTurcanuGheorgheNo ratings yet

- Case Study: AirlinesDocument6 pagesCase Study: AirlinesAngelica RoblesNo ratings yet

- Sociology - Study Plan For CSSDocument13 pagesSociology - Study Plan For CSSMuhammad Faisal Ul Islam100% (6)

- CADI Business PlanDocument25 pagesCADI Business PlanVllybllrNo ratings yet

- Parenting in The PhilippinesDocument17 pagesParenting in The PhilippinesN MalbasNo ratings yet

- State of The School AddressDocument1 pageState of The School AddressAllan RabinoNo ratings yet

- Q3 - WRITE SIMPLE STORY - Grade 3Document5 pagesQ3 - WRITE SIMPLE STORY - Grade 3Elimi Rebucas100% (4)

- Maths Program Proforma Yr 6 t2Document57 pagesMaths Program Proforma Yr 6 t2api-237136245No ratings yet

- Risk Aversion in MLBDocument23 pagesRisk Aversion in MLBDevin EnsingNo ratings yet

- Responsibility AccountingDocument2 pagesResponsibility Accountingswati.bhattNo ratings yet

- BIO2133 NotesDocument20 pagesBIO2133 NotesSammie TdtNo ratings yet

- Transportation Problem - Finding Initial Basic Feasible SolutionDocument9 pagesTransportation Problem - Finding Initial Basic Feasible SolutionWaqar YounasNo ratings yet

- Tower Crane Slew Brakes SalmanDocument2 pagesTower Crane Slew Brakes SalmanAbbas RoziminNo ratings yet

- Google Advance SearchDocument5 pagesGoogle Advance SearchKosma KosmicNo ratings yet

- How To Form A Chunk PowerpointDocument13 pagesHow To Form A Chunk Powerpointhzgl25No ratings yet

- CSCCDocument3 pagesCSCCSudarshan GopalNo ratings yet

- Krishna Kanta Handiqui State Open University: (Only For The January 2021 Batch and in Lieu of MCQ Tests)Document4 pagesKrishna Kanta Handiqui State Open University: (Only For The January 2021 Batch and in Lieu of MCQ Tests)avatar sudarsanNo ratings yet