You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5819)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1092)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (845)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (348)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Agl BillDocument2 pagesAgl BillPratik KayasthaNo ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Affidavit of Conformity (TPM)Document1 pageAffidavit of Conformity (TPM)ellirehcNo ratings yet

- 2 Corporation-RevisedDocument8 pages2 Corporation-RevisedSamantha Nicole Hoy100% (2)

- Name. Salman Sultan Roll No. 21-BBA-22 IFM Assignment. 02Document166 pagesName. Salman Sultan Roll No. 21-BBA-22 IFM Assignment. 02salman soomroNo ratings yet

- Salman Sultan Roll No. 21-BBA-22 IFM Assignment 01Document4 pagesSalman Sultan Roll No. 21-BBA-22 IFM Assignment 01salman soomroNo ratings yet

- Lecture # 3Document18 pagesLecture # 3salman soomroNo ratings yet

- Lecture # 1Document8 pagesLecture # 1salman soomroNo ratings yet

- Lecture # 2Document13 pagesLecture # 2salman soomroNo ratings yet

- Rate of ReturnDocument1 pageRate of Returnsalman soomroNo ratings yet

- Logic May Be Defined As The Organized Body of KnowledgeDocument1 pageLogic May Be Defined As The Organized Body of Knowledgesalman soomroNo ratings yet

- International Financial Management OutlineDocument1 pageInternational Financial Management Outlinesalman soomroNo ratings yet

- Marketing Management Chapter 2Document13 pagesMarketing Management Chapter 2salman soomroNo ratings yet

- LOGICDocument6 pagesLOGICsalman soomroNo ratings yet

- Marketing Management NotesDocument24 pagesMarketing Management Notessalman soomroNo ratings yet

- Marketing Management Chapter 3Document3 pagesMarketing Management Chapter 3salman soomroNo ratings yet

- Edgar DetoyaDocument16 pagesEdgar DetoyaAngelica EltagonNo ratings yet

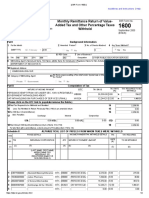

- EFPS Home - EFiling and Payment SystemDocument2 pagesEFPS Home - EFiling and Payment SystemJinkieNo ratings yet

- Insurance Project FinalDocument17 pagesInsurance Project Finalamitkmara0% (1)

- Board Independence and Internal Control Weakness: Evidence From SOX 404 DisclosuresDocument19 pagesBoard Independence and Internal Control Weakness: Evidence From SOX 404 DisclosuresTrixieNo ratings yet

- Tax Case 1 To 30Document21 pagesTax Case 1 To 30Ma RaNo ratings yet

- 000001111841513Document3 pages000001111841513adam sandsNo ratings yet

- Kev 2Document11 pagesKev 2adam burdNo ratings yet

- Simple Discount InterestDocument16 pagesSimple Discount InterestVivian100% (2)

- Acc 101 PDFDocument6 pagesAcc 101 PDFalizaNo ratings yet

- Companies ActDocument27 pagesCompanies ActmiraaloabiNo ratings yet

- Que. 1 Given Below Are The Cash Transaction of M/sDocument5 pagesQue. 1 Given Below Are The Cash Transaction of M/sdeepika_naikNo ratings yet

- Caribbean Examinations CouncilDocument4 pagesCaribbean Examinations CouncilAneilRandyRamdialNo ratings yet

- Financial Accounts: Check Your Understanding G: Activity 3.5.ADocument2 pagesFinancial Accounts: Check Your Understanding G: Activity 3.5.ASOURAV MONDALNo ratings yet

- Summer Internship Project - Sharang Dev - CMBA2Y3Document55 pagesSummer Internship Project - Sharang Dev - CMBA2Y3Kausik BhagatNo ratings yet

- Rise of VeniceDocument65 pagesRise of Venicebill51235No ratings yet

- Banking Master Thesis TopicsDocument7 pagesBanking Master Thesis Topicswcldtexff100% (1)

- Notice of Default Judgement Tendered To Cornerstone Credit ServicesDocument10 pagesNotice of Default Judgement Tendered To Cornerstone Credit ServicesMARK MENO©™No ratings yet

- Andromeda BrochureDocument17 pagesAndromeda Brochurenisha justofficeNo ratings yet

- Effect of Contractionary Monetary Policy On PDFDocument3 pagesEffect of Contractionary Monetary Policy On PDFKhurram AbbasNo ratings yet

- UAE Digest Feb 10Document68 pagesUAE Digest Feb 10Fa HianNo ratings yet

- RailTel Annual Report For Web-CompressedDocument228 pagesRailTel Annual Report For Web-CompressedAmit SahooNo ratings yet

- FM - Kelompok 4 - 79D - Assignment CH9, CH10Document8 pagesFM - Kelompok 4 - 79D - Assignment CH9, CH10Shavia KusumaNo ratings yet

- Claim FormDocument2 pagesClaim Formsupriya67% (6)

- Offer 31197Document1 pageOffer 31197Jheynner MaldonadoNo ratings yet

- Performance Manager PDFDocument146 pagesPerformance Manager PDFparivijjiNo ratings yet

- Calculator-Estimate-9.2kw Without SREC Upfront PurchaseDocument3 pagesCalculator-Estimate-9.2kw Without SREC Upfront PurchaseAhmed CarrionNo ratings yet

- Chapter 8-1. ProblemsDocument10 pagesChapter 8-1. ProblemsCloudKielGuiangNo ratings yet