You might also like

- Scotland Analysis Macroeconomic and Fiscal Performance PDFDocument124 pagesScotland Analysis Macroeconomic and Fiscal Performance PDFgabrielarevelNo ratings yet

- Ireland Financial CrisisDocument15 pagesIreland Financial Crisissantaukura2No ratings yet

- UK Offshore Oil and Gas Industry: Briefing PaperDocument44 pagesUK Offshore Oil and Gas Industry: Briefing PaperLegend AnbuNo ratings yet

- Accounts 11-12Document6 pagesAccounts 11-12api-250300967No ratings yet

- Real World Examples To Incorporate in AnswersDocument3 pagesReal World Examples To Incorporate in AnswersachinthaNo ratings yet

- Abf Annual Report 2012Document120 pagesAbf Annual Report 2012ummesidNo ratings yet

- International Oil & Gas Supply Chain Grow To Record LevelsDocument2 pagesInternational Oil & Gas Supply Chain Grow To Record Levelspathanfor786No ratings yet

- Income in The UkDocument8 pagesIncome in The UkJason KTNo ratings yet

- Economy of The UK: Falling But Still StrongDocument17 pagesEconomy of The UK: Falling But Still StrongVeerduttTiwariNo ratings yet

- UK FNB Market ProfileDocument18 pagesUK FNB Market ProfileTaofiq AbiolaNo ratings yet

- Whitbread AssignmewntDocument50 pagesWhitbread AssignmewntlouisNo ratings yet

- The Scottish EconomyDocument11 pagesThe Scottish EconomyOxfamNo ratings yet

- The Scottish EconomyDocument11 pagesThe Scottish EconomyOxfamNo ratings yet

- The Scottish EconomyDocument11 pagesThe Scottish EconomyOxfamNo ratings yet

- The Scottish EconomyDocument11 pagesThe Scottish EconomyOxfamNo ratings yet

- The Scottish EconomyDocument11 pagesThe Scottish EconomyOxfamNo ratings yet

- The Scottish EconomyDocument11 pagesThe Scottish EconomyOxfamNo ratings yet

- The Scottish EconomyDocument11 pagesThe Scottish EconomyOxfamNo ratings yet

- The Scottish EconomyDocument11 pagesThe Scottish EconomyOxfamNo ratings yet

- The Scottish EconomyDocument11 pagesThe Scottish EconomyOxfamNo ratings yet

- The Scottish EconomyDocument11 pagesThe Scottish EconomyOxfamNo ratings yet

- Money, Interest Rates and Prices in Ireland, 1933-2012Document32 pagesMoney, Interest Rates and Prices in Ireland, 1933-2012ALEEM TEHSEENNo ratings yet

- Front 20 OctDocument1 pageFront 20 OctRebecca BlackNo ratings yet

- Front June 6Document1 pageFront June 6Rebecca BlackNo ratings yet

- The Balance of Payments - A Level EconomicsDocument10 pagesThe Balance of Payments - A Level EconomicsjannerickNo ratings yet

- Fiscal Policy in UkDocument27 pagesFiscal Policy in UkFazil Abbas BanatwalaNo ratings yet

- Scotland Analysis Infographic Oil and Gas Receipts PDFDocument1 pageScotland Analysis Infographic Oil and Gas Receipts PDFgabrielarevelNo ratings yet

- Britain Presentation.Document19 pagesBritain Presentation.Вікторія ДрачукNo ratings yet

- (British Studies Series) Alan Booth (Auth.) - The British Economy in The Twentieth Century-Macmillan Education UK (2001)Document255 pages(British Studies Series) Alan Booth (Auth.) - The British Economy in The Twentieth Century-Macmillan Education UK (2001)Camilo QuezadaNo ratings yet

- Drinks Industry ReportDocument27 pagesDrinks Industry ReportraymanNo ratings yet

- Ilovepdf MergedDocument590 pagesIlovepdf MergedAli Al-mahwetiNo ratings yet

- History of Scotch Whisky Richard ResearchDocument19 pagesHistory of Scotch Whisky Richard ResearchRichard Osahon EseleNo ratings yet

- Foreign Direct InvestmentDocument17 pagesForeign Direct InvestmentIrene GranadosNo ratings yet

- The Economic Landscape of United KindomDocument5 pagesThe Economic Landscape of United KindomJoanna Marie DucutNo ratings yet

- What Went WrongDocument12 pagesWhat Went WrongAléxia DinizNo ratings yet

- How Ireland Became Celtic TigerDocument13 pagesHow Ireland Became Celtic TigerIgor3211No ratings yet

- Retail Grocery SectorDocument19 pagesRetail Grocery SectorAidan ThompsonNo ratings yet

- Green Party 2011 General Election Manifesto Unabridged VersionDocument45 pagesGreen Party 2011 General Election Manifesto Unabridged Versiongreenparty_ieNo ratings yet

- Economy of Uk: - Service SectorDocument18 pagesEconomy of Uk: - Service SectorKeith BrittoNo ratings yet

- Tourism in ScotlandDocument33 pagesTourism in Scotlandapi-253479558No ratings yet

- BREXITDocument26 pagesBREXITPhan Thị Liên XuânNo ratings yet

- UK Total Trade Ad-Hoc Data Release Main FDI ReleaseDocument15 pagesUK Total Trade Ad-Hoc Data Release Main FDI Releaseh3493061No ratings yet

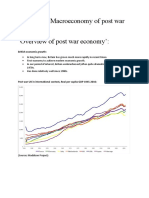

- Week 4 - Lecture 4 - Macroeconomy of Post War BritainDocument8 pagesWeek 4 - Lecture 4 - Macroeconomy of Post War BritainKunal SharmaNo ratings yet

- MK006 - Module 2 - PPT 1Document43 pagesMK006 - Module 2 - PPT 1NICOLE YHNA LAGUISMANo ratings yet

- The Balance of Payments Provides Us With Important Information About Whether or Not A Country Is "Paying Its Way" in The International EconomyDocument6 pagesThe Balance of Payments Provides Us With Important Information About Whether or Not A Country Is "Paying Its Way" in The International EconomyankitaiimNo ratings yet

- Front 1 DecDocument1 pageFront 1 Decanon_565668357No ratings yet

- MacroTutorial 1 AnswersDocument7 pagesMacroTutorial 1 AnswersAndreea Criclevit100% (1)

- Bibin Thomas: Mcompart1Document53 pagesBibin Thomas: Mcompart1Sky509No ratings yet

- UK Cost of Living CrisisDocument17 pagesUK Cost of Living CrisisNishthaNo ratings yet

- The British Economy: Past Present FutureDocument30 pagesThe British Economy: Past Present FutureSanjaya WijesekareNo ratings yet

- The Beer Story Spreads 2013 v6Document2 pagesThe Beer Story Spreads 2013 v6mikfezNo ratings yet

- Macroeconomic Insights For FinlandDocument18 pagesMacroeconomic Insights For FinlandNikshep AntonyNo ratings yet

- The Yorkshire Report 2012 How Did Yorkshire Do?: Aggregated Accounts For The Region's Top 150 CompaniesDocument44 pagesThe Yorkshire Report 2012 How Did Yorkshire Do?: Aggregated Accounts For The Region's Top 150 CompaniesKaren C. TriunfoNo ratings yet

- Presentation 3Document16 pagesPresentation 3eydmann69No ratings yet

- During 1970s and 1980s Scotland's Economy Faced Problems of Many European Countries, Which Were Caused by The Failure of Heavy IndustriesDocument4 pagesDuring 1970s and 1980s Scotland's Economy Faced Problems of Many European Countries, Which Were Caused by The Failure of Heavy Industriesdimasik REDNo ratings yet

- Scotland in The UKDocument24 pagesScotland in The UKTom DonaldsonNo ratings yet

- The United Kingdom: Done By: Zafeer Aaryan RezaDocument10 pagesThe United Kingdom: Done By: Zafeer Aaryan RezaZafeer Aaryan RezaNo ratings yet

- Investing in The FutureDocument13 pagesInvesting in The FuturekkarajanevaNo ratings yet