You might also like

- COT 2 - TLE - Storing and Packaging DessertsDocument3 pagesCOT 2 - TLE - Storing and Packaging DessertsAngelic Almayda100% (2)

- Accounting 101: From Calculating Revenues and Profits to Determining Assets and Liabilities, an Essential Guide to Accounting BasicsFrom EverandAccounting 101: From Calculating Revenues and Profits to Determining Assets and Liabilities, an Essential Guide to Accounting BasicsRating: 4 out of 5 stars4/5 (7)

- Rapport de Stage AtacadaoDocument39 pagesRapport de Stage Atacadaooumaima elharrar100% (3)

- Computerised Accounting Practice Set Using Xero Online Accounting: Australian EditionFrom EverandComputerised Accounting Practice Set Using Xero Online Accounting: Australian EditionNo ratings yet

- Atuadores Mecanico ReiDocument66 pagesAtuadores Mecanico ReiSamuel Dos Santos Mateus100% (1)

- Intermediate Accounting 2: a QuickStudy Digital Reference GuideFrom EverandIntermediate Accounting 2: a QuickStudy Digital Reference GuideNo ratings yet

- Taller GrupalDocument9 pagesTaller GrupalAbigail ZambranoNo ratings yet

- Bookkeeping Essentials For Dummies - AustraliaFrom EverandBookkeeping Essentials For Dummies - AustraliaRating: 4 out of 5 stars4/5 (2)

- Interface Specification - Dimension - Interface Manual DXDCM 09008b8380544007-1321582685628Document36 pagesInterface Specification - Dimension - Interface Manual DXDCM 09008b8380544007-1321582685628Rupesh Nidhi100% (1)

- Value Chain Management Capability A Complete Guide - 2020 EditionFrom EverandValue Chain Management Capability A Complete Guide - 2020 EditionNo ratings yet

- Controlling Payroll Cost - Critical Disciplines for Club ProfitabilityFrom EverandControlling Payroll Cost - Critical Disciplines for Club ProfitabilityNo ratings yet

- It’s Not What You Sell—It’s How You Sell It: Outshine Your Competition & Create Loyal CustomersFrom EverandIt’s Not What You Sell—It’s How You Sell It: Outshine Your Competition & Create Loyal CustomersNo ratings yet

- The Barrington Guide to Property Management Accounting: The Definitive Guide for Property Owners, Managers, Accountants, and Bookkeepers to ThriveFrom EverandThe Barrington Guide to Property Management Accounting: The Definitive Guide for Property Owners, Managers, Accountants, and Bookkeepers to ThriveNo ratings yet

- Teeter-Totter Accounting: Your Visual Guide to Understanding Debits and Credits!From EverandTeeter-Totter Accounting: Your Visual Guide to Understanding Debits and Credits!Rating: 2 out of 5 stars2/5 (1)

- Summary of Peter Frampton & Mark Robilliard's The Joy of AccountingFrom EverandSummary of Peter Frampton & Mark Robilliard's The Joy of AccountingNo ratings yet

- Accounting Principles and Practice: The Commonwealth and International Library: Commerce, Economics and Administration DivisionFrom EverandAccounting Principles and Practice: The Commonwealth and International Library: Commerce, Economics and Administration DivisionRating: 2.5 out of 5 stars2.5/5 (2)

- Cambridge Made a Cake Walk: IGCSE Accounting theory- exam style questions and answersFrom EverandCambridge Made a Cake Walk: IGCSE Accounting theory- exam style questions and answersRating: 2 out of 5 stars2/5 (4)

- Bookkeeping And Accountancy Made Simple: For Owner Managed Businesses, Students And Young EntrepreneursFrom EverandBookkeeping And Accountancy Made Simple: For Owner Managed Businesses, Students And Young EntrepreneursNo ratings yet

- Your Amazing Itty Bitty® Book of QuickBooks® Best PracticesFrom EverandYour Amazing Itty Bitty® Book of QuickBooks® Best PracticesNo ratings yet

- Bookkeeping: Learning The Simple And Effective Methods of Effective Methods Of Bookkeeping (Easy Way To Master The Art Of Bookkeeping)From EverandBookkeeping: Learning The Simple And Effective Methods of Effective Methods Of Bookkeeping (Easy Way To Master The Art Of Bookkeeping)No ratings yet

- Accounting For Small Businesses QuickStart Guide: Understanding Accounting For Your Sole Proprietorship, Startup, & LLCFrom EverandAccounting For Small Businesses QuickStart Guide: Understanding Accounting For Your Sole Proprietorship, Startup, & LLCRating: 5 out of 5 stars5/5 (1)

- Bookkeeping 101 For Business Professionals | Increase Your Accounting Skills And Create More Financial Stability And WealthFrom EverandBookkeeping 101 For Business Professionals | Increase Your Accounting Skills And Create More Financial Stability And WealthNo ratings yet

- Financial Accounting - Want to Become Financial Accountant in 30 Days?From EverandFinancial Accounting - Want to Become Financial Accountant in 30 Days?Rating: 3.5 out of 5 stars3.5/5 (2)

- Economic & Budget Forecast Workbook: Economic workbook with worksheetFrom EverandEconomic & Budget Forecast Workbook: Economic workbook with worksheetNo ratings yet

- Business Financial Information Secrets: How a Business Produces and Utilizes Critical Financial InformationFrom EverandBusiness Financial Information Secrets: How a Business Produces and Utilizes Critical Financial InformationNo ratings yet

- CPA Financial Accounting and Reporting: Second EditionFrom EverandCPA Financial Accounting and Reporting: Second EditionNo ratings yet

- Your Amazing Itty Bitty® Book of QuickBooks® TerminologyFrom EverandYour Amazing Itty Bitty® Book of QuickBooks® TerminologyNo ratings yet

- Build a $1,000 Emergency Fund in 10 Steps: Financial Freedom, #82From EverandBuild a $1,000 Emergency Fund in 10 Steps: Financial Freedom, #82No ratings yet

- Bookkeeping for Nonprofits: A Step-by-Step Guide to Nonprofit AccountingFrom EverandBookkeeping for Nonprofits: A Step-by-Step Guide to Nonprofit AccountingRating: 4 out of 5 stars4/5 (2)

- Business Skills: Money Management, Accounting, and Communication for Small BusinessesFrom EverandBusiness Skills: Money Management, Accounting, and Communication for Small BusinessesNo ratings yet

- Credit Restore Secrets They Never Wanted You to KnowFrom EverandCredit Restore Secrets They Never Wanted You to KnowRating: 4 out of 5 stars4/5 (3)

- Business Skills: The Ultimate Guide to Understanding Communication, Finances, and LeadershipFrom EverandBusiness Skills: The Ultimate Guide to Understanding Communication, Finances, and LeadershipNo ratings yet

- Building Wealth on a Dime: Finding your Financial FreedomFrom EverandBuilding Wealth on a Dime: Finding your Financial FreedomNo ratings yet

- Business Skills: Practical Knowledge for Business Leaders and EntrepreneursFrom EverandBusiness Skills: Practical Knowledge for Business Leaders and EntrepreneursNo ratings yet

- Why Net Present Value Leads To Better Investment Decisions Than Other CriteriaDocument29 pagesWhy Net Present Value Leads To Better Investment Decisions Than Other CriteriaFaxri MammadovNo ratings yet

- 6-7. Risk and ReturnDocument29 pages6-7. Risk and ReturnFaxri MammadovNo ratings yet

- Balance Sheet - Class 3 and 4 Chapter 2Document94 pagesBalance Sheet - Class 3 and 4 Chapter 2Faxri MammadovNo ratings yet

- Financial Accounting ClassTwo Brief RecapDocument8 pagesFinancial Accounting ClassTwo Brief RecapFaxri MammadovNo ratings yet

- Financial Accounting: Fakhri Mammadov Azerbaijan State Economic UniversityDocument39 pagesFinancial Accounting: Fakhri Mammadov Azerbaijan State Economic UniversityFaxri MammadovNo ratings yet

- Chapter 1: Introduction To ITIL: Preparatory ExerciseDocument3 pagesChapter 1: Introduction To ITIL: Preparatory ExerciseMohamed AlyNo ratings yet

- Capital Market and Intermediaries NotesDocument62 pagesCapital Market and Intermediaries NoteslavanyaNo ratings yet

- ANALYSIS AND DESIGN OF Cable Stayed BridgeDocument31 pagesANALYSIS AND DESIGN OF Cable Stayed Bridgeshrikantharle100% (1)

- ESD Asociation Standard For Protection of Electrostatic Disharge ANSI-ESD S6.1-1999Document14 pagesESD Asociation Standard For Protection of Electrostatic Disharge ANSI-ESD S6.1-1999EmilianoNo ratings yet

- CV-Fabián Antonio Rojas Soto 15.05.2021Document4 pagesCV-Fabián Antonio Rojas Soto 15.05.2021Nora Larenas ArriagadaNo ratings yet

- MODULE Special Topics For Public AdministrationDocument27 pagesMODULE Special Topics For Public AdministrationNicolas B. Manolito BootsNo ratings yet

- At Product Sheet MK 90dDocument2 pagesAt Product Sheet MK 90dmetalurg87No ratings yet

- Formato de Registro de Estudiantes Del Programa de Participación Estudiantil 2016-2017Document15 pagesFormato de Registro de Estudiantes Del Programa de Participación Estudiantil 2016-2017Fernando SilvaNo ratings yet

- Caso NeuroderechosDocument26 pagesCaso NeuroderechosVICENTE VELASCO PUEBLANo ratings yet

- Nike México 2Document10 pagesNike México 2Bryan ValtierraNo ratings yet

- Facility Procedures and MaintenanceDocument34 pagesFacility Procedures and Maintenancebaba100% (1)

- Experience Certificate Format Letter PDFDocument2 pagesExperience Certificate Format Letter PDFDenise0% (2)

- CRW-2 Passanger Ship Crisis... Rev. 08Document69 pagesCRW-2 Passanger Ship Crisis... Rev. 08belen bastistaNo ratings yet

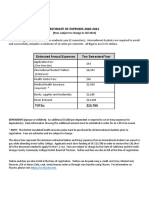

- Estimate of Expenses 2020-2021: (Fees Subject To Change in Fall 2021)Document2 pagesEstimate of Expenses 2020-2021: (Fees Subject To Change in Fall 2021)Walid TaouhidNo ratings yet

- 4655dt1-Mec-002 - C - Cálculos de IluminaciónDocument16 pages4655dt1-Mec-002 - C - Cálculos de IluminaciónChristian RondonNo ratings yet

- Torquimetro MARK-10 CTA100Document12 pagesTorquimetro MARK-10 CTA100Stiven Giraldo NuñezNo ratings yet

- Bliss: Blind Source Separation and ApplicationsDocument4 pagesBliss: Blind Source Separation and ApplicationspostscriptNo ratings yet

- Lista PirâmidesDocument3 pagesLista PirâmidesMargareth SanchezNo ratings yet

- Res 20080086320105315000821516Document2 pagesRes 20080086320105315000821516Hernán Cahuana OrdoñoNo ratings yet

- Mr. and Ms. Ue Caloocan 2011 ScriptDocument29 pagesMr. and Ms. Ue Caloocan 2011 ScriptRochelle Alava CercadoNo ratings yet

- Testing Ingine KaliDocument30 pagesTesting Ingine KaliIngiaNo ratings yet

- El Canal de PanamaDocument8 pagesEl Canal de PanamaFabwalkAltamiranoNo ratings yet

- Proyecto Eco Turístico Reserva Natural Sierra de GuadalupeDocument4 pagesProyecto Eco Turístico Reserva Natural Sierra de GuadalupeEri HernandezNo ratings yet

- Plan Maestro de ProduccionDocument11 pagesPlan Maestro de ProduccionAngel Antonio Diaz NaranjoNo ratings yet

- Law of Contract I PDFDocument71 pagesLaw of Contract I PDFSharath AlimiNo ratings yet