You might also like

- Statement of Financial Position Basic Problems Problem 1-1 (IFRS)Document18 pagesStatement of Financial Position Basic Problems Problem 1-1 (IFRS)student80% (5)

- Wm. Wrigley Jr. Co. recapitalization analysisDocument8 pagesWm. Wrigley Jr. Co. recapitalization analysisHussain AhmedNo ratings yet

- CH 23 Statementofcashflowssolutionsinteraccounting16thedition-171116132124Document71 pagesCH 23 Statementofcashflowssolutionsinteraccounting16thedition-171116132124Lina SakhiNo ratings yet

- Ghana Stock Exchange CourseDocument7 pagesGhana Stock Exchange CoursePrinceNo ratings yet

- Financial Planning and BudgetingDocument45 pagesFinancial Planning and BudgetingRafael BensigNo ratings yet

- Group Iii. Business FinanceDocument11 pagesGroup Iii. Business FinanceChristian PhilipNo ratings yet

- Nature and Characteristics of Budgets ExplainedDocument6 pagesNature and Characteristics of Budgets ExplainedJohn Dave JavaNo ratings yet

- COSTMAN REVIEWER FinalsDocument13 pagesCOSTMAN REVIEWER FinalsHoney MuliNo ratings yet

- Lecture 11 BIS ManagerialDocument25 pagesLecture 11 BIS Managerialnada ahmedNo ratings yet

- Horngrens Financial And Managerial Accounting The Managerial Chapters 4Th Edition Nobles Solutions Manual download pdf 2024Document133 pagesHorngrens Financial And Managerial Accounting The Managerial Chapters 4Th Edition Nobles Solutions Manual download pdf 2024thomas.casey387100% (18)

- Master BudgetDocument15 pagesMaster BudgetHaider AliNo ratings yet

- Budgeting 1Document53 pagesBudgeting 1MRIDUL GOELNo ratings yet

- CH7 BudgetingDocument51 pagesCH7 BudgetingYMNo ratings yet

- Managerial AccountingDocument21 pagesManagerial AccountingRifat HelalNo ratings yet

- Planning and Budgetng.: Course: Introduction To FinancialDocument38 pagesPlanning and Budgetng.: Course: Introduction To FinancialMichaelNo ratings yet

- Technical, Financial and Production Requirements for Business PlanningDocument18 pagesTechnical, Financial and Production Requirements for Business PlanningKimberly Quin CañasNo ratings yet

- Budget Matterial For The Students NewDocument10 pagesBudget Matterial For The Students NewheysemNo ratings yet

- CHAPTER 3 Financial PlanningDocument7 pagesCHAPTER 3 Financial Planningflorabel parana0% (1)

- Lecture Note Part IIDocument29 pagesLecture Note Part IIErit AhmedNo ratings yet

- Chapter 9 Profit PlanningDocument3 pagesChapter 9 Profit Planningahmed arfanNo ratings yet

- Financial Projections and BudgetsDocument53 pagesFinancial Projections and BudgetsRaquel Sibal RodriguezNo ratings yet

- Chapter 5 - Strategy and Master BudgetDocument8 pagesChapter 5 - Strategy and Master BudgetNelsie PinedaNo ratings yet

- Planning and Control For Managers September 2020Document10 pagesPlanning and Control For Managers September 2020muwowo1No ratings yet

- Budgeting Basics for Financial Planning and ControlDocument31 pagesBudgeting Basics for Financial Planning and Controlintan agustina100% (1)

- Local Media6428844306473856818Document38 pagesLocal Media6428844306473856818Maura Lizabeth Gawili BalunggayNo ratings yet

- BudgetDocument14 pagesBudgetKomal Shujaat100% (8)

- Chapter Iii. Master Budget: An Overall Plan: Page 1 of 19Document19 pagesChapter Iii. Master Budget: An Overall Plan: Page 1 of 19Nahum DaichaNo ratings yet

- 10) BudgetingDocument5 pages10) BudgetingAlbert Krohn SandahlNo ratings yet

- Budget FinalDocument32 pagesBudget FinalFaiza KhalilNo ratings yet

- Budgeting: Reference - MGMT Accounting - Reddy and SharmaDocument16 pagesBudgeting: Reference - MGMT Accounting - Reddy and SharmaHafiz RathodNo ratings yet

- H9 Master Budget and ForecastingDocument17 pagesH9 Master Budget and ForecastingGodwin Jil CabotajeNo ratings yet

- Budgeting and Budgetary Control 2019Document10 pagesBudgeting and Budgetary Control 2019Kerrice RobinsonNo ratings yet

- Topic 8 Operation BudgetingDocument12 pagesTopic 8 Operation BudgetingALYZA ANGELA ORNEDONo ratings yet

- Budgeting and Forecasting GuideDocument19 pagesBudgeting and Forecasting Guidemisra anggrainiNo ratings yet

- Chapter 9 Profit PlanningDocument3 pagesChapter 9 Profit Planningahmed arfanNo ratings yet

- BudgetDocument24 pagesBudgetAbhishek ChowdhuryNo ratings yet

- Master BudgetDocument5 pagesMaster BudgetSaranyaa KanagarajNo ratings yet

- Module in BudgetingDocument5 pagesModule in BudgetingJade TanNo ratings yet

- Cost and Management Accounting IIDocument9 pagesCost and Management Accounting IIarefayne wodajoNo ratings yet

- Budgeting for Profits, Sales, Costs and ExpensesDocument2 pagesBudgeting for Profits, Sales, Costs and ExpensesSanwal ShoaibNo ratings yet

- Fiscal Management WF Dr. Emerita R. Alias Edgar Roy M. Curammeng Financial Forecasting, Corporate Planning and BudgetingDocument10 pagesFiscal Management WF Dr. Emerita R. Alias Edgar Roy M. Curammeng Financial Forecasting, Corporate Planning and BudgetingJeannelyn CondeNo ratings yet

- Profit Planning Master BudgetDocument67 pagesProfit Planning Master BudgetJade Ballado-TanNo ratings yet

- Cost II-Ch - 3 Master BudgetDocument14 pagesCost II-Ch - 3 Master BudgetYitera SisayNo ratings yet

- Review 20Document4 pagesReview 20StubadubNo ratings yet

- Marginal Costing and Budgetary ControlDocument5 pagesMarginal Costing and Budgetary ControlThigilpandi07 YTNo ratings yet

- Financial Planning and Control ProcessDocument3 pagesFinancial Planning and Control ProcessPRINCESS HONEYLET SIGESMUNDONo ratings yet

- CH 2 Cost IIDocument10 pagesCH 2 Cost IIfirewNo ratings yet

- Master Budgeting OutlineDocument14 pagesMaster Budgeting OutlineGina Mantos GocotanoNo ratings yet

- Financial Forecasting, Corporate Planning and BudgetingDocument6 pagesFinancial Forecasting, Corporate Planning and BudgetingAdoree RamosNo ratings yet

- Business Finance 2ndquarterDocument176 pagesBusiness Finance 2ndquarterJanelle Dela CruzNo ratings yet

- Ch.13 Managing Small Business FinanceDocument5 pagesCh.13 Managing Small Business FinanceBaesick MoviesNo ratings yet

- UNIT 10 BudgetingDocument28 pagesUNIT 10 BudgetingWinnie Francine LimNo ratings yet

- Chapter 5Document7 pagesChapter 5intelragadio100% (1)

- Financial Planning ToolDocument125 pagesFinancial Planning ToolKareen Tapia PublicoNo ratings yet

- Budget Types, Planning & ControlDocument15 pagesBudget Types, Planning & ControlAnderson GuzmanNo ratings yet

- MAS 5 - Module 1Document11 pagesMAS 5 - Module 1Razmen Ramirez PintoNo ratings yet

- Operational BudgetDocument14 pagesOperational BudgetTsega BirhanuNo ratings yet

- Budget (!Document6 pagesBudget (!Timilehin GbengaNo ratings yet

- Chapter 4 PptsDocument111 pagesChapter 4 PptsKimberly Quin Cañas100% (1)

- BudgetDocument13 pagesBudgetstaycgirls itsgoingdownNo ratings yet

- Chapter 4 Budgeting For Planning and ControlDocument8 pagesChapter 4 Budgeting For Planning and ControlShem CasimiroNo ratings yet

- Sales Budget PlanningDocument18 pagesSales Budget PlanninganashussainNo ratings yet

- Profit PlanningDocument34 pagesProfit Planningmonkey beanNo ratings yet

- Master Budgeting and Forecasting for Hospitality Industry-Teaser: Financial Expertise series for hospitality, #1From EverandMaster Budgeting and Forecasting for Hospitality Industry-Teaser: Financial Expertise series for hospitality, #1No ratings yet

- DIA 22-05 NDOC Fiscal Processes.2Document36 pagesDIA 22-05 NDOC Fiscal Processes.2Sean GolonkaNo ratings yet

- Investment Guide Market Outlook Year End 2022 enDocument52 pagesInvestment Guide Market Outlook Year End 2022 enAurora Ferreira GonzalezNo ratings yet

- ETF Screener - JustETF A2Document4 pagesETF Screener - JustETF A2fish0123No ratings yet

- 5 Institutions of The World Bank GroupDocument3 pages5 Institutions of The World Bank GroupFakhriyya GaflanovaNo ratings yet

- Marketing Strategies of JK Bank Debit CardsDocument51 pagesMarketing Strategies of JK Bank Debit CardsLeo SaimNo ratings yet

- Chapter 11 HWDocument2 pagesChapter 11 HWVinícius AlvesNo ratings yet

- My CA Articleship Experience of Working at Deloitte (Big 4)Document5 pagesMy CA Articleship Experience of Working at Deloitte (Big 4)Rudrin Das100% (1)

- Ans: AnsDocument7 pagesAns: AnsRomelie M. NopreNo ratings yet

- Statute of Limitations For Collecting A DebtDocument2 pagesStatute of Limitations For Collecting A DebtmikotanakaNo ratings yet

- Lic PDFDocument1 pageLic PDFAMIT KUMARNo ratings yet

- Condonation or RemissionDocument6 pagesCondonation or RemissionRhon Mhiel RomanoNo ratings yet

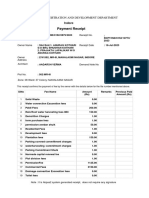

- Payment Receipt: Urban Administration and Development DepartmentDocument2 pagesPayment Receipt: Urban Administration and Development Departmentaadarsh vermaNo ratings yet

- Exchange Rate Pass Through in India: Abhishek KumarDocument15 pagesExchange Rate Pass Through in India: Abhishek KumarinventionjournalsNo ratings yet

- Different Between Conventional Economics & Islamic EconomicsDocument1 pageDifferent Between Conventional Economics & Islamic EconomicsFieza Kyrana100% (2)

- Sandhya New CVDocument3 pagesSandhya New CVNoushad N HamsaNo ratings yet

- Bill statement chargesDocument6 pagesBill statement chargesjjayNo ratings yet

- Andrew AngDocument3 pagesAndrew AngShane Kimberly LubatNo ratings yet

- 1.guess Questions - Theory - Questions and AnswersDocument44 pages1.guess Questions - Theory - Questions and AnswersKrishnaKorada100% (14)

- BUS 6140 module 1 AssignmentDocument4 pagesBUS 6140 module 1 AssignmentvertmeddNo ratings yet

- Invoice: Thank You For Staying With Us at Fairfield by Marriott, KolkataDocument1 pageInvoice: Thank You For Staying With Us at Fairfield by Marriott, Kolkatakousik ChatterjeeNo ratings yet

- Cooper 2015 - Shadow Money and The Shadow WorkforceDocument30 pagesCooper 2015 - Shadow Money and The Shadow Workforceanton.de.rotaNo ratings yet

- Problem SetDocument105 pagesProblem SetYodaking Matt100% (1)

- Manipulation of Financial Statements V0.1Document17 pagesManipulation of Financial Statements V0.1Aniket RaneNo ratings yet

- Reliance Retail Limited Tax Invoice: Original For RecipientDocument1 pageReliance Retail Limited Tax Invoice: Original For RecipientalokNo ratings yet

- Valuation Analysis of Initial Public Offer (IPO) : The Case of IndiaDocument16 pagesValuation Analysis of Initial Public Offer (IPO) : The Case of IndiaAdarsh P RCBSNo ratings yet

- Cfas Midterms q1Document3 pagesCfas Midterms q1Rommel Royce CadapanNo ratings yet