You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5807)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1091)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (842)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (346)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Isb540 - HiwalahDocument16 pagesIsb540 - HiwalahMahyuddin Khalid100% (1)

- An Overview of Judicial Management in MalaysiaDocument17 pagesAn Overview of Judicial Management in MalaysiaTan Ji Xuen100% (1)

- Powers of CorporationsDocument4 pagesPowers of CorporationsSeffirion69No ratings yet

- Carta de Presentacion - R&GDocument5 pagesCarta de Presentacion - R&GRoberto Carlos Pisfil RoseroNo ratings yet

- El SaneamientoDocument14 pagesEl SaneamientoRenee SalazarNo ratings yet

- Obligations and Contracts Article 1156-Article 2270Document136 pagesObligations and Contracts Article 1156-Article 2270Nea TanNo ratings yet

- Agency Reviewer Doc Jim NotesDocument13 pagesAgency Reviewer Doc Jim NotesNA Nanorac JDNo ratings yet

- Contrato de Hospedaje en Derecho Mercantil GuatemalaDocument32 pagesContrato de Hospedaje en Derecho Mercantil GuatemalaJuan Carlos BeltranNo ratings yet

- Pravila Dobrovolnogo Medicinskogo StrahovaniyaDocument173 pagesPravila Dobrovolnogo Medicinskogo StrahovaniyaАнжелика ВасильеваNo ratings yet

- Ejercicios de Tasa de Interes y Ecuacion de Valor.Document13 pagesEjercicios de Tasa de Interes y Ecuacion de Valor.Jose Gregorio FuentesNo ratings yet

- Bailment and Pledge Notes PDFDocument6 pagesBailment and Pledge Notes PDFsridharNo ratings yet

- Common Law Cases On Liabilities of Undis PDFDocument28 pagesCommon Law Cases On Liabilities of Undis PDFKaustub PrakashNo ratings yet

- Ficha Registro, Termo de Rescisão e QuitaçãoDocument4 pagesFicha Registro, Termo de Rescisão e QuitaçãodiegoNo ratings yet

- Manajemen Investasi "Rangkuman Chapter 17 & 18": Dr. Vinola Herawaty, Ak., M.B.ADocument7 pagesManajemen Investasi "Rangkuman Chapter 17 & 18": Dr. Vinola Herawaty, Ak., M.B.AAlief AmbyaNo ratings yet

- Intl Exchange Bank V Sps BrionesDocument1 pageIntl Exchange Bank V Sps BrionesmoniquehadjirulNo ratings yet

- Gamma Scalping & Pyramiding Long StraddleDocument3 pagesGamma Scalping & Pyramiding Long StraddleMayuresh Deshpande0% (2)

- Setting Up A Cayman Islands CompanyDocument5 pagesSetting Up A Cayman Islands CompanyVeler VelericNo ratings yet

- Irrevocable Corporate Purchase Order (Icpo/Loi) For: Contract 12 MonthsDocument4 pagesIrrevocable Corporate Purchase Order (Icpo/Loi) For: Contract 12 MonthsjungNo ratings yet

- Deber 3Document9 pagesDeber 3Dani Torres HidalgoNo ratings yet

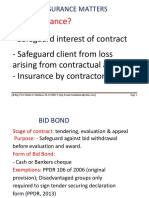

- Ecc 502 - Nsurance MattersDocument24 pagesEcc 502 - Nsurance MattersJohn Wafula wekesaNo ratings yet

- Modelos E.I.R.L. Chile.Document4 pagesModelos E.I.R.L. Chile.Eduardo Campos Henríquez100% (1)

- AP2 & AP2A Terms & ConditionsDocument1 pageAP2 & AP2A Terms & ConditionsJCNo ratings yet

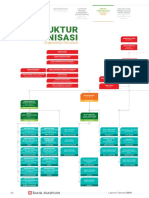

- Struktur Organisasi: Organization StructureDocument2 pagesStruktur Organisasi: Organization StructureRalila SejahteraNo ratings yet

- Islamic Finance and BankingDocument10 pagesIslamic Finance and BankingMaruf AhmedNo ratings yet

- Vices of ConsentDocument5 pagesVices of ConsentStephanie Cui SilvaNo ratings yet

- Article 1206Document2 pagesArticle 1206CG WitchyNo ratings yet

- Informe Descriptivo Sobre La Letra de CambioDocument5 pagesInforme Descriptivo Sobre La Letra de CambioDavid Samael Ortez LopezNo ratings yet

- Hedge Fund Structures PDFDocument9 pagesHedge Fund Structures PDFStanley MunodawafaNo ratings yet

- Sem 6 Audit CourseDocument9 pagesSem 6 Audit CourseSuyash KhadeNo ratings yet

- Contract Research Paper-Sem 3Document6 pagesContract Research Paper-Sem 3Priyanshi GandhiNo ratings yet