You might also like

- Journal Entries For Merchandising Business Problem 1Document12 pagesJournal Entries For Merchandising Business Problem 1Arn Manuyag88% (24)

- Test Questions and Solutions True-FalseDocument99 pagesTest Questions and Solutions True-Falsekabirakhan2007100% (1)

- Computerised Accounting Practice Set Using MYOB AccountRight - Advanced Level: Australian EditionFrom EverandComputerised Accounting Practice Set Using MYOB AccountRight - Advanced Level: Australian EditionNo ratings yet

- Oracle Fixed AssetsDocument78 pagesOracle Fixed AssetsTejeshwar KumarNo ratings yet

- 03-13-2023 - Letter To The Comptroller Office - Wells Fargo FraudDocument47 pages03-13-2023 - Letter To The Comptroller Office - Wells Fargo FraudJerry VashchookNo ratings yet

- Audit of InventoryDocument32 pagesAudit of Inventoryxxxxxxxxx92% (48)

- Chapter 3Document10 pagesChapter 3Kristina Kitty100% (1)

- AP03 Audit of Inventories QDocument6 pagesAP03 Audit of Inventories Qbobo kaNo ratings yet

- NYIF Accounting Module 9 Excercise With AnswersssDocument3 pagesNYIF Accounting Module 9 Excercise With AnswersssShahd OkashaNo ratings yet

- 718 MP111 Individual Assignment S2 2022 Part 1Document23 pages718 MP111 Individual Assignment S2 2022 Part 1Rosalie BachillerNo ratings yet

- AdjustingDocument7 pagesAdjustingRochelle BuensucesoNo ratings yet

- Accounting 1aDocument23 pagesAccounting 1aFaith Marasigan88% (16)

- Acctg Ass No. 10 Merchandising BusinessDocument5 pagesAcctg Ass No. 10 Merchandising BusinessDaisy Marie A. Rosel75% (4)

- Far Quiz Nov. 20, 2020Document7 pagesFar Quiz Nov. 20, 2020Yanna AlquisolaNo ratings yet

- Cambridge Made a Cake Walk: IGCSE Accounting theory- exam style questions and answersFrom EverandCambridge Made a Cake Walk: IGCSE Accounting theory- exam style questions and answersRating: 2 out of 5 stars2/5 (4)

- Intermediate 1A: Problem CompilationDocument24 pagesIntermediate 1A: Problem CompilationPatricia Nicole Barrios100% (4)

- QuizDocument15 pagesQuizMark Domingo Mendoza100% (1)

- Exercise. AdjustmentsDocument6 pagesExercise. AdjustmentsDavid Con Rivero79% (14)

- Chapter 5Document18 pagesChapter 5winkko ucsmNo ratings yet

- Chapter 3 InventoryDocument7 pagesChapter 3 InventoryPhoe MuNo ratings yet

- Machindising OperationDocument38 pagesMachindising Operationlove D infintyNo ratings yet

- HOSP1210 Chapter8extraDocument4 pagesHOSP1210 Chapter8extraMonica AtizadoNo ratings yet

- Accounting Tutorial 2Document6 pagesAccounting Tutorial 2Mega Pop LockerNo ratings yet

- CHAPTER 10 Intermediate AccountingDocument133 pagesCHAPTER 10 Intermediate AccountingWynpha PodiotanNo ratings yet

- Quiz 03 Name: - Score: - Rating: - Problem 01Document3 pagesQuiz 03 Name: - Score: - Rating: - Problem 01Jom BuddyNo ratings yet

- Horngrens Financial and Managerial Accounting The Financial Chapters 5Th Edition Miller Nobles Solutions Manual Full Chapter PDFDocument36 pagesHorngrens Financial and Managerial Accounting The Financial Chapters 5Th Edition Miller Nobles Solutions Manual Full Chapter PDFjestine.wesson615100% (14)

- Accounting Assignment 06A 207Document12 pagesAccounting Assignment 06A 207Aniyah's RanticsNo ratings yet

- 4355894Document5 pages4355894mohitgaba19No ratings yet

- Exercises of Session 3Document3 pagesExercises of Session 3tranhlthNo ratings yet

- SUBSIDIARY BOOKS Purchases Returns JournalDocument4 pagesSUBSIDIARY BOOKS Purchases Returns JournalRichard TshumahNo ratings yet

- Correcting Errors - Booklet+lectureDocument22 pagesCorrecting Errors - Booklet+lectureJake blakeNo ratings yet

- Chapter 5 Question Review 11th EditionDocument10 pagesChapter 5 Question Review 11th EditionEmiraslan MhrrovNo ratings yet

- Chapter 5 Question ReviewDocument10 pagesChapter 5 Question ReviewRoting EnomarNo ratings yet

- AccountancyDocument16 pagesAccountancyevangiebalunsat9No ratings yet

- Dysas - Fin Acc - 3rdDocument5 pagesDysas - Fin Acc - 3rdJao FloresNo ratings yet

- Audit of Inventories and Cost of Goods SoldDocument9 pagesAudit of Inventories and Cost of Goods SoldDita Indah0% (1)

- FABM - L-10Document16 pagesFABM - L-10Seve HanesNo ratings yet

- Accounting 1 PretestDocument8 pagesAccounting 1 Pretestelumba michaelNo ratings yet

- Christine Bianca Chua - M3 S3.2 Learning TasksDocument14 pagesChristine Bianca Chua - M3 S3.2 Learning TasksChristine Bianca ChuaNo ratings yet

- AttachmentDocument22 pagesAttachmentchintya milathaniaNo ratings yet

- 10.14.2017 Quiz 1 (Audit of Inventory)Document5 pages10.14.2017 Quiz 1 (Audit of Inventory)PatOcampoNo ratings yet

- Chapter 8 InventoryDocument11 pagesChapter 8 Inventorymarwan2004acctNo ratings yet

- Cabigon Audit Inventories 5Document14 pagesCabigon Audit Inventories 5Rie CabigonNo ratings yet

- Accounting For InventoriesDocument11 pagesAccounting For InventoriesAllyssa A.No ratings yet

- Sheet (8) Intermediate Accounting: InventoriesDocument12 pagesSheet (8) Intermediate Accounting: Inventoriesmagdy kamelNo ratings yet

- CH 05Document4 pagesCH 05vivienNo ratings yet

- Chapter3 Students 1Document22 pagesChapter3 Students 1Leah Mae NolascoNo ratings yet

- Syllabus AnswerDocument24 pagesSyllabus AnswerasdfNo ratings yet

- Siti Nur Apriyani - 2009102 - PAK-7A - Tugas 3 AKHOSDocument5 pagesSiti Nur Apriyani - 2009102 - PAK-7A - Tugas 3 AKHOSS Nur ApriyaniNo ratings yet

- Assigment 9Document5 pagesAssigment 9WinaNo ratings yet

- Chap 4 Books of Prime EntryDocument29 pagesChap 4 Books of Prime EntrynabkillNo ratings yet

- QUIZ 6-QuesDocument7 pagesQUIZ 6-QuesPhán Tiêu TiềnNo ratings yet

- 2009-10-28 225356 SouthcoastDocument17 pages2009-10-28 225356 Southcoastjas02h1100% (1)

- Lecture 6 Accounting For Inventory (I)Document33 pagesLecture 6 Accounting For Inventory (I)chestervale1No ratings yet

- Cash BooksDocument13 pagesCash BooksWanjala RajabNo ratings yet

- Illustrative Problems On IAS 2 InventoriesDocument2 pagesIllustrative Problems On IAS 2 InventoriesAnne Marieline BuenaventuraNo ratings yet

- Audit 2 - Topic3Document20 pagesAudit 2 - Topic3YUSUFNo ratings yet

- WRD 27e SG Solutions CH 06Document22 pagesWRD 27e SG Solutions CH 06Ellii YouTube channelNo ratings yet

- 6.3.2.7 Evaluate 6.2 - Long ProblemDocument4 pages6.3.2.7 Evaluate 6.2 - Long ProblemJohn Clinton PeñafloridaNo ratings yet

- Accounting For Merachandising BusinessDocument11 pagesAccounting For Merachandising BusinessErick MonteNo ratings yet

- Audit of Inventory - HomeworkDocument3 pagesAudit of Inventory - HomeworkMarnelli CatalanNo ratings yet

- Problems 1 - Accounting Cycle PDFDocument17 pagesProblems 1 - Accounting Cycle PDFEliyah JhonsonNo ratings yet

- 2 Major Types of AccountsDocument18 pages2 Major Types of AccountsLUKE ADAM CAYETANONo ratings yet

- POA1-Assignment - Chapter 5 - QDocument5 pagesPOA1-Assignment - Chapter 5 - QAuora Bianca100% (1)

- Chapter 5Document14 pagesChapter 5RB100% (3)

- MPS 55R118 01583021L 05 2011Document2 pagesMPS 55R118 01583021L 05 2011vinayak_patil72No ratings yet

- Quiz BowlDocument2 pagesQuiz Bowlaccounting probNo ratings yet

- Not For Profit IonDocument23 pagesNot For Profit Ioncarahul89No ratings yet

- Account Activity: Shantinagar BranchDocument2 pagesAccount Activity: Shantinagar BranchRaFaT HaQNo ratings yet

- August 13, 2014Document12 pagesAugust 13, 2014The Delphos HeraldNo ratings yet

- C.T.a. EB Case No. 1786 - Deductible Input VATDocument19 pagesC.T.a. EB Case No. 1786 - Deductible Input VATKaira ArmadaNo ratings yet

- CashTOa JPDocument11 pagesCashTOa JPDarwin LopezNo ratings yet

- Chapter 8 - Input Tax Credit - NotesDocument57 pagesChapter 8 - Input Tax Credit - Notesmohd abidNo ratings yet

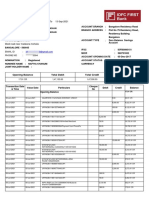

- IDFC FIRST Bank Statement 13 000 2021 120000 - 3948Document4 pagesIDFC FIRST Bank Statement 13 000 2021 120000 - 3948chandra kiranNo ratings yet

- 6 The Trial BalanceDocument4 pages6 The Trial Balanceayshaneasrin08No ratings yet

- Sap Fi 4.6 Exercises Financial Accounting - Chapter 14 Document/Account MaintenanceDocument12 pagesSap Fi 4.6 Exercises Financial Accounting - Chapter 14 Document/Account MaintenanceKishore NaiduNo ratings yet

- Fi ReportsDocument66 pagesFi ReportsShreekumarNo ratings yet

- Contoh Tugasan AccountDocument20 pagesContoh Tugasan AccountMuhammad IddinNo ratings yet

- Adjustments To Final AccountsDocument20 pagesAdjustments To Final AccountsSalamaNo ratings yet

- Journal Entry: NARVAEZ, CapitalDocument7 pagesJournal Entry: NARVAEZ, CapitalRachelle Mae SalvadorNo ratings yet

- Fundamentals of Accountancy, Business and Management 2: Fatima N. RecopelacionDocument33 pagesFundamentals of Accountancy, Business and Management 2: Fatima N. RecopelacionCharity Lumactod AlangcasNo ratings yet

- AFAR Problems WorksheetDocument13 pagesAFAR Problems WorksheetjajajaredredNo ratings yet

- Chapter - 1 & 2 (Presentations On Introduction To Accounting & The Accounting Equation)Document52 pagesChapter - 1 & 2 (Presentations On Introduction To Accounting & The Accounting Equation)Sattaki RoyNo ratings yet

- Acc117 Test 2 July 2022 - Tapah BRS SSDocument3 pagesAcc117 Test 2 July 2022 - Tapah BRS SSNajmuddin AzuddinNo ratings yet

- Question Paper Unit Test - I Accountancy XIDocument1 pageQuestion Paper Unit Test - I Accountancy XIJoshi DrcpNo ratings yet

- Using JournalEntries and JournalVouchers Objects in SAP Business One 6.5.HtmDocument7 pagesUsing JournalEntries and JournalVouchers Objects in SAP Business One 6.5.HtmRenzo Gutierrez MedinaNo ratings yet

- 15-Mca-Nr-Accounting and Financial ManagementDocument4 pages15-Mca-Nr-Accounting and Financial ManagementSRINIVASA RAO GANTA0% (2)

- 3 - Book of Prime Entry - Latihan General JournalDocument7 pages3 - Book of Prime Entry - Latihan General Journalnurzbiet8587No ratings yet

- 01-CalapanCity2019 Transmittal LetterDocument6 pages01-CalapanCity2019 Transmittal LetterkQy267BdTKNo ratings yet