You might also like

- Intermediate Accounting 2: a QuickStudy Digital Reference GuideFrom EverandIntermediate Accounting 2: a QuickStudy Digital Reference GuideNo ratings yet

- Shareholders' Equity ExplainedDocument61 pagesShareholders' Equity ExplainedLawrence NarvaezNo ratings yet

- Corporation: Shareholders EquityDocument38 pagesCorporation: Shareholders EquityKristen IjacoNo ratings yet

- Corporation Formation EssentialsDocument110 pagesCorporation Formation EssentialsXander MerzaNo ratings yet

- Accounting Chapter 9Document7 pagesAccounting Chapter 9Angelica Faye DuroNo ratings yet

- Retained EarningsDocument39 pagesRetained EarningsPrincess Aubrey BalbinNo ratings yet

- CORPORATIONDocument38 pagesCORPORATIONChristine Kaye DamoloNo ratings yet

- 06.module & Task-Share Capital PDFDocument8 pages06.module & Task-Share Capital PDFJohn Lery YumolNo ratings yet

- Shareholder S' EquityDocument55 pagesShareholder S' EquityRojParconNo ratings yet

- Ch10&11. Shareholders' EquityDocument29 pagesCh10&11. Shareholders' EquityHazell DNo ratings yet

- Chapter 16Document53 pagesChapter 16V ChandriaNo ratings yet

- Corporations Part 3Document20 pagesCorporations Part 3Miss LunaNo ratings yet

- ACC601Lecture 5Document33 pagesACC601Lecture 5Joe MajchrzakNo ratings yet

- Shareholders Equity Part 1Document57 pagesShareholders Equity Part 1AlliahDataNo ratings yet

- Dividend PolicyDocument52 pagesDividend PolicyANISH KUMARNo ratings yet

- Chapter 15 Corporation-Share CapitalDocument58 pagesChapter 15 Corporation-Share CapitalLe Ann Rhine MayantongNo ratings yet

- Shareholder's Equity-Share Capital - 0Document35 pagesShareholder's Equity-Share Capital - 0lilienesieraNo ratings yet

- Intermediate Accounting Volume 1: Accounting for Investments in Equity SecuritiesDocument69 pagesIntermediate Accounting Volume 1: Accounting for Investments in Equity SecuritiesRomuell BanaresNo ratings yet

- Intermediate Accounting Volume 1 Valix, Peralta and Valix (2020)Document69 pagesIntermediate Accounting Volume 1 Valix, Peralta and Valix (2020)Romuell Banares100% (3)

- Chapter 16 Class NotesDocument52 pagesChapter 16 Class NotesAnila ANo ratings yet

- Accounting for Share Capital in CorporationsDocument57 pagesAccounting for Share Capital in CorporationsMarriel Fate Cullano75% (8)

- Equity Investment 16Document9 pagesEquity Investment 16gab camonNo ratings yet

- What are Financial StatementsDocument51 pagesWhat are Financial Statementskrys_elleNo ratings yet

- Advanced Accounting-2 Company: HoldingDocument20 pagesAdvanced Accounting-2 Company: HoldingTB AhmedNo ratings yet

- Auditing Problem For Shareholder's EquityDocument14 pagesAuditing Problem For Shareholder's Equityblack hudieNo ratings yet

- Dividends PDFDocument41 pagesDividends PDFHarold EspirituNo ratings yet

- Orporations: Share Capital, Retained Earnings, and Financial ReportingDocument10 pagesOrporations: Share Capital, Retained Earnings, and Financial ReportingkakaoNo ratings yet

- Retained Earnings: Appropriation and Quasi-ReorganizationDocument25 pagesRetained Earnings: Appropriation and Quasi-ReorganizationtruthNo ratings yet

- Module 4 Packet: College of CommerceDocument24 pagesModule 4 Packet: College of CommerceDexie Jane MayoNo ratings yet

- IASSS16e Ch13.Ab - AzDocument28 pagesIASSS16e Ch13.Ab - AzLovely DungcaNo ratings yet

- Corporation ProblemsDocument5 pagesCorporation ProblemsKathleenNo ratings yet

- AC 1201 - RETAINED EARNINGS (Appropriation and Quasi-Reorganization)Document25 pagesAC 1201 - RETAINED EARNINGS (Appropriation and Quasi-Reorganization)Joseph Jason Kyle Baquero0% (1)

- Topic 2 - Accounting For Redemption of Shares and Debentures-1Document59 pagesTopic 2 - Accounting For Redemption of Shares and Debentures-1Neema JosephNo ratings yet

- Audit of Shareholders' Equity RecordsDocument7 pagesAudit of Shareholders' Equity RecordsJustine UngabNo ratings yet

- Chap6 150401024123 Conversion Gate01 PDFDocument54 pagesChap6 150401024123 Conversion Gate01 PDFrosalie gelbolingoNo ratings yet

- Im Share Capital Transactions Subsequent To Original IssuanceDocument7 pagesIm Share Capital Transactions Subsequent To Original IssuanceElaine OlivarioNo ratings yet

- 2017 Class 16 EquityDocument35 pages2017 Class 16 EquityChandra Sekhar ChittineniNo ratings yet

- Chapter 15 - Accounting For CorporationsDocument22 pagesChapter 15 - Accounting For CorporationsAlizah BucotNo ratings yet

- SHE - Treasury Shares, Right Issue, Share Split With Warrants - 0Document50 pagesSHE - Treasury Shares, Right Issue, Share Split With Warrants - 0lilienesieraNo ratings yet

- Corporation NotesDocument5 pagesCorporation NotesPrestine Faith SalinasNo ratings yet

- Limited CompaniesDocument51 pagesLimited CompaniesSteven RaintungNo ratings yet

- Financial Accounting - Information For Decisions - Session 8 - Chapter 10 PPT Eh5CoID6zuDocument38 pagesFinancial Accounting - Information For Decisions - Session 8 - Chapter 10 PPT Eh5CoID6zumukul3087_305865623No ratings yet

- Acctg1205 - Chapter 8Document48 pagesAcctg1205 - Chapter 8Elj Grace BaronNo ratings yet

- Introduction To Financial Statements: Income Statement: Topic 4bDocument31 pagesIntroduction To Financial Statements: Income Statement: Topic 4bsarahNo ratings yet

- Shareholders Equity With Discussion ExercisesDocument163 pagesShareholders Equity With Discussion ExercisesGiane Bernard PunayanNo ratings yet

- Chapter 13Document13 pagesChapter 13Mondy MondyNo ratings yet

- Corporation Part 1Document9 pagesCorporation Part 11701791No ratings yet

- Accounting For Corporation - Retained EarningsDocument50 pagesAccounting For Corporation - Retained EarningsAlessandraNo ratings yet

- Financial Analysis and Reporting Part 1Document21 pagesFinancial Analysis and Reporting Part 1Zhai HumidoNo ratings yet

- FEU Institute Accounting for Corporations ConceptsDocument10 pagesFEU Institute Accounting for Corporations ConceptsFatima GuevarraNo ratings yet

- On-Line Lesson 1 Part 2Document28 pagesOn-Line Lesson 1 Part 2Kimberly Claire AtienzaNo ratings yet

- Bvps and EpsDocument30 pagesBvps and EpsRenzo Melliza100% (1)

- Copy Treasury StocksDocument213 pagesCopy Treasury StocksJuren Demotor Dublin100% (2)

- Understanding The BSDocument33 pagesUnderstanding The BSAbhishekh KashyapNo ratings yet

- Share Holders Equity: BOOKS and Records of A CorporationDocument5 pagesShare Holders Equity: BOOKS and Records of A CorporationQueen ValleNo ratings yet

- Intermediate Accounting 3Document20 pagesIntermediate Accounting 3Gali jizNo ratings yet

- Unit 2 - Financial StatementDocument16 pagesUnit 2 - Financial StatementLihassNo ratings yet

- 61415Document65 pages61415Jnn CycNo ratings yet

- Statement of Equity ChangesDocument7 pagesStatement of Equity ChangesHikmət RüstəmovNo ratings yet

- CHAPTER 14 Non. 14Document6 pagesCHAPTER 14 Non. 14Ahmed AymanNo ratings yet

- Ch.16 Dilutive Securities and Earnings Per Share: Chapter Learning ObjectivesDocument7 pagesCh.16 Dilutive Securities and Earnings Per Share: Chapter Learning ObjectivesFaishal Alghi FariNo ratings yet

- Venture Capital Finder ' S Fee AgreementDocument2 pagesVenture Capital Finder ' S Fee AgreementSteven Swanson100% (1)

- Anita Mills CaseDocument6 pagesAnita Mills CaseKushal ThakkarNo ratings yet

- CorporationDocument1 pageCorporationHanaNo ratings yet

- The Contemporary World M6T4Document13 pagesThe Contemporary World M6T4joint accountNo ratings yet

- Nummi: New United Motor Manufacturing, Inc. (NUMMI) Was AnDocument11 pagesNummi: New United Motor Manufacturing, Inc. (NUMMI) Was AnRoberto Ortega MicalizziNo ratings yet

- Numbers 19, 20 and 21 (Corporate Liquidation)Document2 pagesNumbers 19, 20 and 21 (Corporate Liquidation)Tk KimNo ratings yet

- 2 1 4 PDFDocument4 pages2 1 4 PDFankusha SharmaNo ratings yet

- Print VAT Registration - GOV - UkDocument11 pagesPrint VAT Registration - GOV - Uksiva kumarNo ratings yet

- Cabbage Market Value Chain Profile 2020Document40 pagesCabbage Market Value Chain Profile 2020Deep & Minimal Tech House Music UnionHouseMusicNo ratings yet

- Position PaperDocument6 pagesPosition PaperDonalyn RamosNo ratings yet

- Gill Marcus: Issues For Consideration in Mergers and Takeovers From A Regulatory PerspectiveDocument12 pagesGill Marcus: Issues For Consideration in Mergers and Takeovers From A Regulatory PerspectiveTushar AhujaNo ratings yet

- Sentence TransformationDocument23 pagesSentence TransformationAn ThuNo ratings yet

- Socio 101 Midterm Exam ReviewDocument9 pagesSocio 101 Midterm Exam ReviewNeil bryan MoninioNo ratings yet

- Hexaware Futures Feb 2019 ReportDocument4 pagesHexaware Futures Feb 2019 Reportmraghavendra.20056383No ratings yet

- Financial Markets: Submitted byDocument12 pagesFinancial Markets: Submitted byrjay manaloNo ratings yet

- Lecture03 SlidesDocument50 pagesLecture03 Slidesaditya jainNo ratings yet

- 4.2 Contracts of Similar Size and Nature: Criteria Compliance Requirements DocumentsDocument3 pages4.2 Contracts of Similar Size and Nature: Criteria Compliance Requirements DocumentsRameshNo ratings yet

- Strategic Management Midterm Exam Question B Answer-2Document3 pagesStrategic Management Midterm Exam Question B Answer-2Aayush AgarwalNo ratings yet

- Mobile Financial Services (MFS) Business and Regulations: Evolution in South Asian MarketsDocument26 pagesMobile Financial Services (MFS) Business and Regulations: Evolution in South Asian MarketsNishat ShimaNo ratings yet

- Humpuss Intermoda Transportasi TBK - Bilingual - 31 - Dec - 2018 - Released PDFDocument132 pagesHumpuss Intermoda Transportasi TBK - Bilingual - 31 - Dec - 2018 - Released PDFAyu Krisma YupitaNo ratings yet

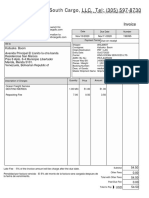

- South Cargo, LLC. Tel: (305) 597-8730: InvoiceDocument1 pageSouth Cargo, LLC. Tel: (305) 597-8730: InvoiceChevyveronaNo ratings yet

- InTech Feb2021Document46 pagesInTech Feb2021Fernando KatayamaNo ratings yet

- Presentation 1Document14 pagesPresentation 1Tanvi SidhayeNo ratings yet

- Human Resources Performance Measurement Approaches Compared To Measures Used in Master's Theses in ASUDocument7 pagesHuman Resources Performance Measurement Approaches Compared To Measures Used in Master's Theses in ASUHugo Enrique Oblitas SalinasNo ratings yet

- Strategi Digital Branding Pada Startup Social Crowdfunding: Syahrul Hidayanto & Ishadi Soetopo KartosapoetroDocument15 pagesStrategi Digital Branding Pada Startup Social Crowdfunding: Syahrul Hidayanto & Ishadi Soetopo Kartosapoetrofour TeenNo ratings yet

- Problem 7-1: True or False False: Fact PatternDocument23 pagesProblem 7-1: True or False False: Fact PatternMichael Brian TorresNo ratings yet

- Corrugated Paper BoxDocument13 pagesCorrugated Paper BoxGulfCartonNo ratings yet

- Urban Development Policies in Punjab Volume IIDocument303 pagesUrban Development Policies in Punjab Volume IIsakshi sainiNo ratings yet

- Botswana: 2020 Annual Research: Key HighlightsDocument1 pageBotswana: 2020 Annual Research: Key HighlightsLisani DubeNo ratings yet