You might also like

- Paper Work PDFDocument1 pagePaper Work PDFAnonymous KWHusENo ratings yet

- BNYX Lease AgreementDocument2 pagesBNYX Lease AgreementBenjamin Debosnigs Saint Fort100% (1)

- Estate Tax and Some Exempt TransfersDocument3 pagesEstate Tax and Some Exempt TransfersfcnrrsNo ratings yet

- Bar Review Companion: Civil Law: Anvil Law Books Series, #1From EverandBar Review Companion: Civil Law: Anvil Law Books Series, #1No ratings yet

- International Relations and Its TheoriesDocument27 pagesInternational Relations and Its TheoriesAilyn AñanoNo ratings yet

- Political Law Suggested Answers 2019Document23 pagesPolitical Law Suggested Answers 2019sonya80% (5)

- Novation of Shipbuilding ContractDocument2 pagesNovation of Shipbuilding ContractDavid SeahNo ratings yet

- MCQs (Leave Rules) 1Document12 pagesMCQs (Leave Rules) 1Crick Compact100% (4)

- UCEDA Admissions Application 2021Document5 pagesUCEDA Admissions Application 2021Adriana OsorioNo ratings yet

- Unedited Evidence CASE Digest 1Document88 pagesUnedited Evidence CASE Digest 1rheyneNo ratings yet

- Estate Taxation NotesDocument39 pagesEstate Taxation NotesJovel LayasanNo ratings yet

- Tax2 - L02 - Notes (Business Tax)Document12 pagesTax2 - L02 - Notes (Business Tax)Savage KongNo ratings yet

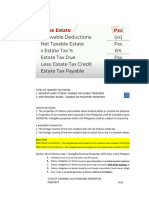

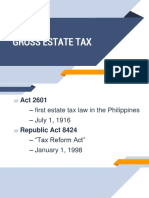

- Chapter 2 Gross EstateDocument4 pagesChapter 2 Gross EstateMary Anne KazuyaNo ratings yet

- Estate Tax Summary Tax CodeDocument1 pageEstate Tax Summary Tax CodeAlthea PalmaNo ratings yet

- Estate and Donors TaxesDocument19 pagesEstate and Donors TaxesMiraflor Sanchez BiñasNo ratings yet

- Tax2 L02 NotesDocument14 pagesTax2 L02 NotesSavage KongNo ratings yet

- Topic 8 - Gross EstateDocument5 pagesTopic 8 - Gross EstateNicole Daphne FigueroaNo ratings yet

- Taxation Law II Green NotesDocument126 pagesTaxation Law II Green NotesNewCovenantChurchNo ratings yet

- Tax-2-Recits Estate Tax Donors TaxDocument5 pagesTax-2-Recits Estate Tax Donors TaxEmmanuel MabolocNo ratings yet

- Taxation Ii Atty. Shirley Tuazon I. Taxation Under The NircDocument4 pagesTaxation Ii Atty. Shirley Tuazon I. Taxation Under The NircRonnel DeinlaNo ratings yet

- Estate Taxation Gross Estate: Adjusted Net Asset MethodDocument12 pagesEstate Taxation Gross Estate: Adjusted Net Asset MethodMae NamocNo ratings yet

- Estate Tax: Transfer TaxesDocument7 pagesEstate Tax: Transfer TaxesElla QuiNo ratings yet

- Prelims ReviewerDocument78 pagesPrelims ReviewerAndrea IvanneNo ratings yet

- Tax 2 ReviewerDocument78 pagesTax 2 ReviewerAndrea IvanneNo ratings yet

- Estate TaxDocument4 pagesEstate TaxLovely Jane Raut CabiltoNo ratings yet

- Transfer Taxes: A. Estate TaxDocument31 pagesTransfer Taxes: A. Estate TaxAna MarieNo ratings yet

- Taxation Ii Atty. Shirley Tuazon I. Taxation Under The NircDocument5 pagesTaxation Ii Atty. Shirley Tuazon I. Taxation Under The NircRonnel DeinlaNo ratings yet

- Gross EstateDocument63 pagesGross EstateMark Angelo SibayanNo ratings yet

- Notes in EstateDocument5 pagesNotes in EstateESTRADA, Angelica T.No ratings yet

- Transfer TaxesDocument87 pagesTransfer TaxesMyka FloresNo ratings yet

- Transfer TaxesDocument7 pagesTransfer TaxesDesiree Ann MiralNo ratings yet

- Section 85. Gross Estate. - The Value of The Gross Estate of TheDocument6 pagesSection 85. Gross Estate. - The Value of The Gross Estate of TheCharles RiveraNo ratings yet

- Tax MidtermsDocument13 pagesTax MidtermsCharles RiveraNo ratings yet

- Tax MidtermsDocument23 pagesTax MidtermsCharles RiveraNo ratings yet

- Orca Share Media1520856036149Document19 pagesOrca Share Media1520856036149Aybern BawtistaNo ratings yet

- Material 11 Estate TaxDocument20 pagesMaterial 11 Estate Taxnodnel salonNo ratings yet

- Annex A - Allowable Deductions From The Gross EstateDocument4 pagesAnnex A - Allowable Deductions From The Gross EstateダニエルNo ratings yet

- Business Tax MODULEDocument32 pagesBusiness Tax MODULEDanica GeneralaNo ratings yet

- TAX Tax Law 2Document158 pagesTAX Tax Law 2iamtikalonNo ratings yet

- Supplemental Notes Transfer and Business Taxation: Transfer Tax Income TaxDocument6 pagesSupplemental Notes Transfer and Business Taxation: Transfer Tax Income TaxanonymousjoeyNo ratings yet

- Taxation II Transfer Taxes: SEC. 84. Rate of Estate Tax. - There Shall Be Levied, Assessed, CollectedDocument10 pagesTaxation II Transfer Taxes: SEC. 84. Rate of Estate Tax. - There Shall Be Levied, Assessed, CollectedBianca LaderaNo ratings yet

- Gross Estate ReviewerDocument8 pagesGross Estate ReviewerCharles RiveraNo ratings yet

- Resident Citizen, Non-Resident Citizen & Resident Alien Decedents Deductions From Gross Estate Nirc Train LawDocument5 pagesResident Citizen, Non-Resident Citizen & Resident Alien Decedents Deductions From Gross Estate Nirc Train LawMarianne SironNo ratings yet

- 3 Estate Tax-Gross EstateDocument2 pages3 Estate Tax-Gross Estateyatot carbonelNo ratings yet

- Gross Estate ReviewerDocument9 pagesGross Estate ReviewerAiziel OrenseNo ratings yet

- Estate and Donor'sDocument20 pagesEstate and Donor'sBar2012No ratings yet

- Taxation Ii NotesDocument16 pagesTaxation Ii NotesAudrey Kristina MaypaNo ratings yet

- Chapter 2 - Gross Estate PDFDocument6 pagesChapter 2 - Gross Estate PDFVanessa Castor GasparNo ratings yet

- Gross Estate InclusionDocument4 pagesGross Estate InclusionAlaineNo ratings yet

- Module 2 Estate TaxDocument14 pagesModule 2 Estate TaxClarissa Atillano FababairNo ratings yet

- Transfer TaxDocument60 pagesTransfer Taxandrei jim100% (6)

- Tax 2 Module 2Document7 pagesTax 2 Module 2jakeNo ratings yet

- Estate Taxes 2Document56 pagesEstate Taxes 2Patrick TanNo ratings yet

- Taxation Ii Notes PDFDocument16 pagesTaxation Ii Notes PDFAudrey Kristina MaypaNo ratings yet

- Every Character. Held: There Could Not Be Partial Reciprocity. It WouldDocument7 pagesEvery Character. Held: There Could Not Be Partial Reciprocity. It WouldJia FriasNo ratings yet

- Enhancement Estate Tax2Document35 pagesEnhancement Estate Tax2Kathleen Tabasa ManuelNo ratings yet

- Estate TaxDocument65 pagesEstate TaxXiu MinNo ratings yet

- CPAR Estate-TaxationDocument18 pagesCPAR Estate-Taxationwendygilbuela2022No ratings yet

- Gross Estate IntroductionDocument2 pagesGross Estate IntroductionJustz LimNo ratings yet

- Business Tax Chapter 2 ReviewerDocument4 pagesBusiness Tax Chapter 2 ReviewerMurien LimNo ratings yet

- 06 Chap 13 14 Mamalateo 2019 Tax BookDocument65 pages06 Chap 13 14 Mamalateo 2019 Tax BookJeremias CusayNo ratings yet

- Estate TaxDocument10 pagesEstate Taxlamborghini aventadorNo ratings yet

- Gross EstateDocument74 pagesGross EstateDonghae FishdaNo ratings yet

- Taxation Law Ii Review: Transfer TaxesDocument59 pagesTaxation Law Ii Review: Transfer TaxesDevilleres Eliza DenNo ratings yet

- Securitized Real Estate and 1031 ExchangesFrom EverandSecuritized Real Estate and 1031 ExchangesNo ratings yet

- Estate and Business Succession Planning: A Legal Guide to Wealth TransferFrom EverandEstate and Business Succession Planning: A Legal Guide to Wealth TransferNo ratings yet

- Purple Illustrated Cute Cake Daily MemoDocument1 pagePurple Illustrated Cute Cake Daily MemoAilyn AñanoNo ratings yet

- Facher's PleaDocument1 pageFacher's PleaAilyn AñanoNo ratings yet

- Week 5 - CaseDocument53 pagesWeek 5 - CaseAilyn AñanoNo ratings yet

- People v. Sensano, 58 Phil. 73Document2 pagesPeople v. Sensano, 58 Phil. 73Ailyn AñanoNo ratings yet

- WCL 2022 Q6Document4 pagesWCL 2022 Q6Ailyn AñanoNo ratings yet

- Pet RevDocument21 pagesPet RevAilyn AñanoNo ratings yet

- WCL Q3 2022Document16 pagesWCL Q3 2022Ailyn AñanoNo ratings yet

- People v. BokingcoDocument4 pagesPeople v. BokingcoAilyn AñanoNo ratings yet

- Solla Vs AscuetaDocument2 pagesSolla Vs AscuetaAilyn AñanoNo ratings yet

- People Vs CasabuenaDocument3 pagesPeople Vs CasabuenaAilyn AñanoNo ratings yet

- Report PPT Fria 2010Document80 pagesReport PPT Fria 2010Ailyn AñanoNo ratings yet

- Digests Feb 12Document58 pagesDigests Feb 12Ailyn AñanoNo ratings yet

- Umil V Ramos - 1991Document18 pagesUmil V Ramos - 1991Ailyn AñanoNo ratings yet

- Minutes of The MeetingDocument3 pagesMinutes of The MeetingAilyn AñanoNo ratings yet

- 1legal Research Assignment 19 - Appellants BriefDocument31 pages1legal Research Assignment 19 - Appellants BriefAilyn AñanoNo ratings yet

- (Atillo v. Bombay, G.R. No. 136096, (February 7, 2001) )Document2 pages(Atillo v. Bombay, G.R. No. 136096, (February 7, 2001) )Ailyn AñanoNo ratings yet

- Velayo v. Shell CompanyDocument2 pagesVelayo v. Shell CompanyAilyn AñanoNo ratings yet

- Articles of Incorporation A. AñanoDocument5 pagesArticles of Incorporation A. AñanoAilyn AñanoNo ratings yet

- The Contemporary World: Joanna Marie C. Rodil Instructor I Cas-DsshDocument21 pagesThe Contemporary World: Joanna Marie C. Rodil Instructor I Cas-DsshAilyn AñanoNo ratings yet

- HW No. 1 - CDDocument20 pagesHW No. 1 - CDAilyn AñanoNo ratings yet

- Nature of ListeningDocument18 pagesNature of ListeningAilyn AñanoNo ratings yet

- Legal DocumentDocument2 pagesLegal DocumentAilyn AñanoNo ratings yet

- Cometa vs. CADocument6 pagesCometa vs. CAjegel23No ratings yet

- STATCON G3 - Case DigestsDocument24 pagesSTATCON G3 - Case DigestsFrench TemplonuevoNo ratings yet

- Sale of Immovable PropertyDocument6 pagesSale of Immovable PropertyRuchita Kaundal100% (1)

- Chattel MortgageDocument2 pagesChattel MortgageRepolyo Ket Cabbage100% (1)

- Indpendent Auditor's Report - SampleDocument2 pagesIndpendent Auditor's Report - SampleBambi Cultura100% (1)

- Abrams vs. USDocument7 pagesAbrams vs. USMhay A. EsllvanoreNo ratings yet

- Kawooya RoscoDocument2 pagesKawooya RoscoMwesigwa SamuelNo ratings yet

- PoliDocument222 pagesPoliFai Meile100% (1)

- In Re EpiPen - Mylan Defendants' Opposition To Class Certification 2019-06-18Document98 pagesIn Re EpiPen - Mylan Defendants' Opposition To Class Certification 2019-06-18The Type 1 Diabetes Defense FoundationNo ratings yet

- Contract Tutorial 2 FinalDocument40 pagesContract Tutorial 2 FinalWendy Chye100% (1)

- Module 1 - Topic No. 1 - Part2Document10 pagesModule 1 - Topic No. 1 - Part2Limuel MacasaetNo ratings yet

- Jacksonian Democrats EssayDocument5 pagesJacksonian Democrats EssayAndrew BridgesNo ratings yet

- Barons Marketing Corp V Court of AppealsDocument3 pagesBarons Marketing Corp V Court of AppealsCesar CoNo ratings yet

- BEDIA v. WHITE G.R. No. 94050. November 21, 1991Document2 pagesBEDIA v. WHITE G.R. No. 94050. November 21, 1991SSNo ratings yet

- Natural Law Theories - LAW 531 Natural Law Theories - LAW 531Document8 pagesNatural Law Theories - LAW 531 Natural Law Theories - LAW 531Atimango JaneNo ratings yet

- The Philippine American General Insurance Company, Inc., vs. Court of AppealsDocument1 pageThe Philippine American General Insurance Company, Inc., vs. Court of AppealsperlitainocencioNo ratings yet

- Managerial Remuneration Checklist FinalDocument4 pagesManagerial Remuneration Checklist FinaldhuvadpratikNo ratings yet

- Nego Case DoctrinesDocument4 pagesNego Case DoctrinesFlorence RoseteNo ratings yet

- Effective Prior Art SearchDocument6 pagesEffective Prior Art SearchAmit Sudarsan/ VideaimIPNo ratings yet

- Martinez v. Rep of The PHDocument7 pagesMartinez v. Rep of The PHAerith AlejandreNo ratings yet

- G.R. No. L-11658 / February 15, 1918Document3 pagesG.R. No. L-11658 / February 15, 1918Simon James SemillaNo ratings yet

- ART 2176-2177 Culpa Aquillana Vs Culpa CriminalDocument16 pagesART 2176-2177 Culpa Aquillana Vs Culpa CriminalIzo BellosilloNo ratings yet

- ARBITRATION BY BESTFRIENDS - Snehal Tulsaney, Alvira KhanDocument15 pagesARBITRATION BY BESTFRIENDS - Snehal Tulsaney, Alvira KhanSNEHAL TULSANEY 2130172No ratings yet