You might also like

- Financial Accounting - Want to Become Financial Accountant in 30 Days?From EverandFinancial Accounting - Want to Become Financial Accountant in 30 Days?Rating: 5 out of 5 stars5/5 (1)

- 2-Concepts, Coventions and PrinciplesDocument34 pages2-Concepts, Coventions and PrinciplesVasu NarangNo ratings yet

- Accounting Concepts, Conventions & PrinciplesDocument34 pagesAccounting Concepts, Conventions & PrincipleskaleabNo ratings yet

- Generally Accepted Accounting Principles GAAP12Document9 pagesGenerally Accepted Accounting Principles GAAP12Rojesh BasnetNo ratings yet

- Accounting Concepts and ConventionsDocument30 pagesAccounting Concepts and ConventionsSheba Mary SamNo ratings yet

- FA Model Exam NotesDocument30 pagesFA Model Exam NotesBell BottleNo ratings yet

- Local Media203070640845348906Document64 pagesLocal Media203070640845348906xzekelsNo ratings yet

- Foa NotesDocument6 pagesFoa NotesdhruvNo ratings yet

- Principles of AccountingDocument11 pagesPrinciples of AccountingMariel MagraciaNo ratings yet

- ACCOUNTING CONCEPTS, CONVENTIONS AND PRINCIPLES EXPLAINEDDocument42 pagesACCOUNTING CONCEPTS, CONVENTIONS AND PRINCIPLES EXPLAINEDSheetal NafdeNo ratings yet

- Foa NotesDocument6 pagesFoa NotesdhruvNo ratings yet

- FMS Chapter OneDocument19 pagesFMS Chapter OneEyael ShimleasNo ratings yet

- Accounting Principles and ConceptsDocument31 pagesAccounting Principles and ConceptskunyangNo ratings yet

- 'O'_Level__Accounting_concepts-1Document7 pages'O'_Level__Accounting_concepts-1marshallchips2006No ratings yet

- Accounting Concepts and ConventionsDocument18 pagesAccounting Concepts and ConventionsRoshani ChaudhariNo ratings yet

- Accounting Principles and ConceptsDocument9 pagesAccounting Principles and Conceptsmarissa casareno almueteNo ratings yet

- Introduction To AccountingDocument34 pagesIntroduction To AccountingDhruv BhagatNo ratings yet

- Accounting Concepts: They Are Useful in Preparing Financial StatementsDocument9 pagesAccounting Concepts: They Are Useful in Preparing Financial StatementsUdaypal Singh Rawat100% (1)

- BANA MainDocument77 pagesBANA MainHonrada-Remoto JunrielNo ratings yet

- Accounting ConceptsDocument16 pagesAccounting Conceptsumerceo100% (1)

- Accounting For Manager: Accounting Period April and Ends On 31 March Every Year Unless Otherwise Specifically MentionedDocument66 pagesAccounting For Manager: Accounting Period April and Ends On 31 March Every Year Unless Otherwise Specifically Mentionedbaburao1762No ratings yet

- Study Materials: Vedantu Innovations Pvt. Ltd. Score High With A Personal Teacher, Learn LIVE Online!Document11 pagesStudy Materials: Vedantu Innovations Pvt. Ltd. Score High With A Personal Teacher, Learn LIVE Online!Yogendra ShuklaNo ratings yet

- Acc PresentationDocument24 pagesAcc PresentationjainrinkiNo ratings yet

- Accounting PrinciplesDocument17 pagesAccounting PrinciplesAbhijay AnoopNo ratings yet

- Accounting PrinciplesDocument74 pagesAccounting PrinciplesSehjad PadaniyaNo ratings yet

- Theory Based Accounting - Short Notes - (Aarambh 2.0 2024)Document17 pagesTheory Based Accounting - Short Notes - (Aarambh 2.0 2024)sidhant singhNo ratings yet

- Revised Accounting For LawyersDocument67 pagesRevised Accounting For Lawyersvinay rakshithNo ratings yet

- Fin GyaanDocument80 pagesFin Gyaanmayank patelNo ratings yet

- Accounting concepts explainedDocument23 pagesAccounting concepts explainedVibhuti MoreNo ratings yet

- CU DR Balwinder Singh 03112022 PDFDocument64 pagesCU DR Balwinder Singh 03112022 PDFAkshat Sharma Roll no 21No ratings yet

- What Is AccountingDocument29 pagesWhat Is AccountingTanaa SulimanNo ratings yet

- Principle of Accounting - Bachelor 1 Updated Latest (Autosaved)Document58 pagesPrinciple of Accounting - Bachelor 1 Updated Latest (Autosaved)chrismanax80No ratings yet

- Principles of AccountingDocument70 pagesPrinciples of AccountingCassandra UmaliNo ratings yet

- Accounting Principles, Concepts and PoliciesDocument21 pagesAccounting Principles, Concepts and PoliciesClayton Johnson0% (1)

- Accounting Concepts &Document15 pagesAccounting Concepts &Boi NonoNo ratings yet

- Accounting Principles or ConceptsDocument15 pagesAccounting Principles or ConceptsHelen B. EvansNo ratings yet

- Lesson-2 Generally Accepted Accounting Principles and Accounting StandardsDocument10 pagesLesson-2 Generally Accepted Accounting Principles and Accounting StandardsKarthigeyan Balasubramaniam100% (1)

- Role of Accounting in SocietyDocument9 pagesRole of Accounting in SocietyAbdul GafoorNo ratings yet

- Lecture 1 - Introduction To AccountingDocument19 pagesLecture 1 - Introduction To AccountingVivien NgNo ratings yet

- Chapter 2 Accounting Concepts - ConventionsDocument32 pagesChapter 2 Accounting Concepts - ConventionsfaaNo ratings yet

- 1ST Onlinemodule 1-3Document32 pages1ST Onlinemodule 1-3Jennifer De Leon100% (1)

- Pe 6009 Engineering EconomyDocument55 pagesPe 6009 Engineering EconomyAbhishek BhattNo ratings yet

- Assignment #1: Submitted by Submitted ToDocument5 pagesAssignment #1: Submitted by Submitted Toabdullah akhtarNo ratings yet

- 29ACCOUNTING Concepts ConventionsDocument34 pages29ACCOUNTING Concepts ConventionsAnkit GuptaNo ratings yet

- Accountingformanagers Reference NotesDocument52 pagesAccountingformanagers Reference NotesGopika SatheesanNo ratings yet

- Fundamentals OF Accounting: Accounting by Meigs, Williams, Haka, BettnerDocument64 pagesFundamentals OF Accounting: Accounting by Meigs, Williams, Haka, BettnerAliya SaeedNo ratings yet

- Accounting As A SystemDocument10 pagesAccounting As A SystemFrankoy RuttyNo ratings yet

- Orca Share Media1679236592806 7043228758154205937 PDFDocument24 pagesOrca Share Media1679236592806 7043228758154205937 PDFHeaven SyNo ratings yet

- Basics of Financial Accounting ExplainedDocument30 pagesBasics of Financial Accounting ExplainedSAURABH PATELNo ratings yet

- Lecture One Role of Accounting in SocietyDocument10 pagesLecture One Role of Accounting in SocietyJagadeep Reddy BhumireddyNo ratings yet

- ACCOUNTING KEY CONCEPTS AND CONVENTIONSDocument25 pagesACCOUNTING KEY CONCEPTS AND CONVENTIONSawaezNo ratings yet

- Accounting ConceptsDocument13 pagesAccounting ConceptsdeepshrmNo ratings yet

- Theory Base of AccountingDocument11 pagesTheory Base of AccountingEshuNo ratings yet

- 10business Module4 AccountingDocument117 pages10business Module4 Accountingchris100% (1)

- Accountancy Notes ch-2Document4 pagesAccountancy Notes ch-2Ansh JaiswalNo ratings yet

- GAAPs: Theory base of accountingDocument22 pagesGAAPs: Theory base of accountingDivija MalhotraNo ratings yet

- Chapter 4 - Income Measurement & Accrual Accounting: Recognition & Measurement in Financial StatementsDocument5 pagesChapter 4 - Income Measurement & Accrual Accounting: Recognition & Measurement in Financial StatementsHareem Zoya WarsiNo ratings yet

- Introduction To AccountingDocument51 pagesIntroduction To Accountingmonkey bean100% (1)

- Accounting PrinciplesDocument11 pagesAccounting PrinciplesPiyush AjmeraNo ratings yet

- Assignment On Accouting Prin-Assum-RulesDocument4 pagesAssignment On Accouting Prin-Assum-RulesNazimRezaNo ratings yet

- MixDocument32 pagesMixUnnecessary BuyingNo ratings yet

- Session 7 Case StudyDocument4 pagesSession 7 Case StudyDiajal HooblalNo ratings yet

- Income Tax Law and PracticeDocument3 pagesIncome Tax Law and PracticeAbinash VeeraragavanNo ratings yet

- FA1 Financial Accounting 1 exam questionsDocument1 pageFA1 Financial Accounting 1 exam questionsSamuelNo ratings yet

- Alberta's BN# and Financial StatementsDocument24 pagesAlberta's BN# and Financial StatementsFredNo ratings yet

- FAC1601 Financial Accounting Reporting Tutorial LetterDocument15 pagesFAC1601 Financial Accounting Reporting Tutorial LetterSophie ZinyandoNo ratings yet

- Chapter 08 FINDocument32 pagesChapter 08 FINUnoNo ratings yet

- Declaration 80D 80DDBDocument1 pageDeclaration 80D 80DDBShobit0% (1)

- Basic Concepts in Economics (Notes)Document7 pagesBasic Concepts in Economics (Notes)149 Reehab ShaikhNo ratings yet

- Associate Information: Ayansys Solutions Private Limited (Payslip)Document1 pageAssociate Information: Ayansys Solutions Private Limited (Payslip)B BhaskarNo ratings yet

- The Mansab and Jagir Systems Under The Mughals in India Did Not Develop SuddenlyDocument3 pagesThe Mansab and Jagir Systems Under The Mughals in India Did Not Develop SuddenlyJubin 20hist331No ratings yet

- Pre 4 - Audit of The Gas, Petroleum, and Oil Sectors (Powerpoint)Document59 pagesPre 4 - Audit of The Gas, Petroleum, and Oil Sectors (Powerpoint)nefael lanciolaNo ratings yet

- FIN1161 - Introduction To Finance For Business - Report 2Document6 pagesFIN1161 - Introduction To Finance For Business - Report 2thunlagbd230128No ratings yet

- 1 Associate (SOFP SOCI) - Class NotesDocument9 pages1 Associate (SOFP SOCI) - Class NotesIshtiaq KhaliqNo ratings yet

- PLP Government Accounting Final ExamDocument4 pagesPLP Government Accounting Final ExamApril ManjaresNo ratings yet

- Housing Affordability Measure ExplainedDocument64 pagesHousing Affordability Measure Explainedharsha13486No ratings yet

- Master Handout CAF 8 Cost and Management AccountingDocument36 pagesMaster Handout CAF 8 Cost and Management AccountingShehrozSTNo ratings yet

- PayslipDocument1 pagePayslipsuzieebillsNo ratings yet

- Rules in Holding Period in Capital GainsDocument39 pagesRules in Holding Period in Capital GainsTrine De LeonNo ratings yet

- Accounting Standards (1 To 29)Document76 pagesAccounting Standards (1 To 29)Vipul I. PanchasaraNo ratings yet

- (ST) 02-Measuring The Cost of LivingDocument55 pages(ST) 02-Measuring The Cost of LivingThanh Ngan DuongNo ratings yet

- HEPL Financials v1.9Document16 pagesHEPL Financials v1.9A YoungNo ratings yet

- FA1 FA2 FA3 FA4 MergedDocument12 pagesFA1 FA2 FA3 FA4 MergedBhavesh GuravNo ratings yet

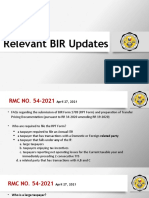

- Relevant BIR Updates on RPT Form and Transfer PricingDocument49 pagesRelevant BIR Updates on RPT Form and Transfer PricingElsha dela penaNo ratings yet

- Jasper and Anneka Rehnquist Case Study SolutionDocument5 pagesJasper and Anneka Rehnquist Case Study SolutionChintu WatwaniNo ratings yet

- Exodus Company's Trial BalanceDocument2 pagesExodus Company's Trial BalanceQueen ValleNo ratings yet

- 284911percentage Sheet-2 - Crwill - 230808 - 173504Document17 pages284911percentage Sheet-2 - Crwill - 230808 - 173504Pratap SinghNo ratings yet

- Claim Interest and HRA ExemptionDocument1 pageClaim Interest and HRA ExemptionShobitNo ratings yet

- Applied Economics Module 4Document6 pagesApplied Economics Module 4HUMSS 11-BNo ratings yet

- Bustax Chapter 1Document9 pagesBustax Chapter 1Pineda, Paula MarieNo ratings yet