You might also like

- Shona Module - ChiShona Vol 1 - FINAL4WEBDocument272 pagesShona Module - ChiShona Vol 1 - FINAL4WEBNomsa Muradzi76% (37)

- 2005 Ikea CatalogDocument28 pages2005 Ikea Catalograhmani bagherNo ratings yet

- AIS6e.ab - Az Ch01Document89 pagesAIS6e.ab - Az Ch01RewardMaturureNo ratings yet

- Bis - System 2 1 1Document42 pagesBis - System 2 1 1Dave NNo ratings yet

- Chapter 3Document22 pagesChapter 3garashi jumaNo ratings yet

- Bis SystemDocument50 pagesBis SystemDave NNo ratings yet

- Week 2Document22 pagesWeek 2api-3737023No ratings yet

- System Analysis and Design: Archit VermaDocument198 pagesSystem Analysis and Design: Archit Vermaawmeesh mishraNo ratings yet

- Introduction To System ConceptsDocument52 pagesIntroduction To System ConceptsRahulNo ratings yet

- Unit 2-Introduction To Information Systems DevelopmentDocument32 pagesUnit 2-Introduction To Information Systems Developmentjaq hit coolNo ratings yet

- Pharmacy Lecture (System Analysis and Design)Document25 pagesPharmacy Lecture (System Analysis and Design)Aimen NaeemNo ratings yet

- The System Environment: What Is A SYSTEM?Document47 pagesThe System Environment: What Is A SYSTEM?Ailyn CuentasNo ratings yet

- Chapter IntroductionDocument38 pagesChapter Introductionsohad aldeekNo ratings yet

- Nature of Systems and System Analysis ConceptsDocument35 pagesNature of Systems and System Analysis ConceptsSer IvanNo ratings yet

- Analysis and Design: of E-Commerce SystemsDocument27 pagesAnalysis and Design: of E-Commerce SystemshamedskyNo ratings yet

- SystemsDocument33 pagesSystemsStuti Aggarwal 2K21/BBA/148No ratings yet

- Computer Programming and Applications CIM 102Document16 pagesComputer Programming and Applications CIM 102Sami MurshedNo ratings yet

- Management Information System (OMC 401) - Assignment ADocument4 pagesManagement Information System (OMC 401) - Assignment ASaurabhChaudhary100% (1)

- Lecture Handouts and Assignment IDocument54 pagesLecture Handouts and Assignment IsurangauorNo ratings yet

- System Analysis and DesignDocument50 pagesSystem Analysis and DesignDarrius Dela PeñaNo ratings yet

- Chapter 1Document55 pagesChapter 1garashi jumaNo ratings yet

- Unit 3Document31 pagesUnit 3abc defNo ratings yet

- ISAD Unit-IDocument10 pagesISAD Unit-INikhil KachhawahNo ratings yet

- Mis Co4Document12 pagesMis Co4sreeram saipranithaNo ratings yet

- Chapter One System DevelopmentDocument37 pagesChapter One System Developmentabduwasi ahmedNo ratings yet

- An Overview - Enterprise: Prepare By: Dr. Usman Tariq 08 January 2020Document26 pagesAn Overview - Enterprise: Prepare By: Dr. Usman Tariq 08 January 2020Faisal AlharbiNo ratings yet

- Types of System: by Ankita KishoreDocument12 pagesTypes of System: by Ankita KishoreAnviNo ratings yet

- Systems Analysis and Design-INTRODUCTION 2Document19 pagesSystems Analysis and Design-INTRODUCTION 2Rowell SalapareNo ratings yet

- Introduction To ERPDocument57 pagesIntroduction To ERPArfa ShaikhNo ratings yet

- Management Information SystemsDocument87 pagesManagement Information SystemsLicio Lentimo100% (1)

- CHAPTER 3 - Systems Concepts & AccountingDocument35 pagesCHAPTER 3 - Systems Concepts & AccountingHendriMaulanaNo ratings yet

- Lesson 2: System Framework: ObjectiveDocument3 pagesLesson 2: System Framework: ObjectivedearsaswatNo ratings yet

- Chapter One Introduction To SADDocument26 pagesChapter One Introduction To SADCali Cali100% (1)

- Chapter 2Document54 pagesChapter 2Mostafa HossamNo ratings yet

- Bi Unit 1Document87 pagesBi Unit 1Rahul SharmaNo ratings yet

- ISM Unit-4Document18 pagesISM Unit-4upkeeratspamNo ratings yet

- Information System Analysis and DesignDocument26 pagesInformation System Analysis and DesignAnania Kapala SauloNo ratings yet

- Introduction To Accounting Information SystemDocument34 pagesIntroduction To Accounting Information SystemSeiza FurukawaNo ratings yet

- The Information System An Accountant's PerspectiveDocument71 pagesThe Information System An Accountant's PerspectiveGUDATA ABARANo ratings yet

- Systems Analysis and Design Notes Complete Lecture NotesDocument67 pagesSystems Analysis and Design Notes Complete Lecture Notesbasma.mostafa1No ratings yet

- Ais Hall 7e Chap1Document41 pagesAis Hall 7e Chap1tipo_de_incognitoNo ratings yet

- Lesson 1 Overview of IT AuditDocument42 pagesLesson 1 Overview of IT AuditMCDABCNo ratings yet

- Ism IntroDocument13 pagesIsm Intropascal ianNo ratings yet

- Chapter1 System DevelopmentDocument18 pagesChapter1 System DevelopmentJohn Wanyoike MakauNo ratings yet

- ICTService Management Review QuestionsDocument28 pagesICTService Management Review QuestionsYINQI LIANGNo ratings yet

- Mis Slide 04Document68 pagesMis Slide 04Ismatullah ZazaiNo ratings yet

- Management Information System Fundamentals of Information SystemsDocument53 pagesManagement Information System Fundamentals of Information SystemsShobhit ShuklaNo ratings yet

- Introduction To Systems Analysis and DesignDocument51 pagesIntroduction To Systems Analysis and DesignDev RahaNo ratings yet

- Session 1 and 2 CompleteDocument72 pagesSession 1 and 2 Completedavid nduatiNo ratings yet

- DSSDocument39 pagesDSSNarender Saini0% (1)

- TFM Module 1Document121 pagesTFM Module 1Abhi HemaNo ratings yet

- Mis NotesDocument5 pagesMis Notesmayank barsenaNo ratings yet

- Accounting Information Systems: John Wiley & Sons, IncDocument25 pagesAccounting Information Systems: John Wiley & Sons, Inclfp_912No ratings yet

- Unit01 Part02Document16 pagesUnit01 Part02Kabir SinghNo ratings yet

- Information Gathering: Interactive Methods: SummaryDocument12 pagesInformation Gathering: Interactive Methods: SummaryEmerighon CagubcobNo ratings yet

- 1.what Is System Decomposition?Document39 pages1.what Is System Decomposition?Emma WatsonNo ratings yet

- Q) What Is A System?: - S: I. II. Iii. IV. VDocument41 pagesQ) What Is A System?: - S: I. II. Iii. IV. VkrishnaamallilkNo ratings yet

- The Systems Development Life Cycle: Jasmin Rose A. DalesDocument29 pagesThe Systems Development Life Cycle: Jasmin Rose A. DalesJasmin Rose Arriesgado DalesNo ratings yet

- IS Unit 3Document73 pagesIS Unit 3poyipiyuNo ratings yet

- Unit 1Document71 pagesUnit 1api-3834497No ratings yet

- Chapter 8 Basic Sytems Concepts and ToolsDocument14 pagesChapter 8 Basic Sytems Concepts and ToolsfroteemusicNo ratings yet

- Zero To Mastery In Cybersecurity- Become Zero To Hero In Cybersecurity, This Cybersecurity Book Covers A-Z Cybersecurity Concepts, 2022 Latest EditionFrom EverandZero To Mastery In Cybersecurity- Become Zero To Hero In Cybersecurity, This Cybersecurity Book Covers A-Z Cybersecurity Concepts, 2022 Latest EditionNo ratings yet

- DCLM Daily Manna Devotional 3rd March 2024 - Go Again Seven TimesDocument4 pagesDCLM Daily Manna Devotional 3rd March 2024 - Go Again Seven TimesPamela MabizaNo ratings yet

- DCLM Daily Manna Devotional 3rd March 2024 - Go Again Seven TimesDocument4 pagesDCLM Daily Manna Devotional 3rd March 2024 - Go Again Seven TimesPamela MabizaNo ratings yet

- 3 Excel Formulas IFRSCPDboxDocument7 pages3 Excel Formulas IFRSCPDboxPamela MabizaNo ratings yet

- IFRS16 Accounting Lessees CPDboxDocument3 pagesIFRS16 Accounting Lessees CPDboxPamela MabizaNo ratings yet

- Chart - Investment in Other Entitties Under IFRSDocument1 pageChart - Investment in Other Entitties Under IFRShaihoangvNo ratings yet

- AIS6e ch03Document50 pagesAIS6e ch03Jecca JamonNo ratings yet

- AIS6e.ab - Az ch04Document46 pagesAIS6e.ab - Az ch04Pamela MabizaNo ratings yet

- Accounting Information System (Chapter 5)Document41 pagesAccounting Information System (Chapter 5)Cassie100% (1)

- Introduction To Transaction Processing: Accounting Information Systems, James A. HallDocument39 pagesIntroduction To Transaction Processing: Accounting Information Systems, James A. HallDiane MagnayeNo ratings yet

- AIS6e ch03Document50 pagesAIS6e ch03Jecca JamonNo ratings yet

- Lbex-Docid 194031Document27 pagesLbex-Docid 194031Pamela MabizaNo ratings yet

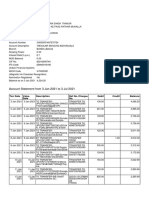

- Account Statement From 3 Jan 2021 To 3 Jul 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument8 pagesAccount Statement From 3 Jan 2021 To 3 Jul 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceSanatan ThakurNo ratings yet

- Platform General Vxworks Migration Guide 3.6Document124 pagesPlatform General Vxworks Migration Guide 3.6Ding YueNo ratings yet

- AN1009: Driving MOSFET and IGBT Switches Using The Si828x: Key FeaturesDocument22 pagesAN1009: Driving MOSFET and IGBT Switches Using The Si828x: Key FeaturesNikolas AugustoNo ratings yet

- Guide To Computer Forensics and Investigations 5th Edition Bill Test BankDocument11 pagesGuide To Computer Forensics and Investigations 5th Edition Bill Test Bankshelleyrandolphikeaxjqwcr100% (30)

- Soalan Sebenar Sejarah STPM Penggal 2 PDFDocument1 pageSoalan Sebenar Sejarah STPM Penggal 2 PDFFatins FilzaNo ratings yet

- How To Automatically Backup phpMyAdmin - SQLBackupAndFTP's BlogDocument6 pagesHow To Automatically Backup phpMyAdmin - SQLBackupAndFTP's BlogIbn KhaledNo ratings yet

- Basic Passport Checks: Cyan Magenta BlackDocument23 pagesBasic Passport Checks: Cyan Magenta BlackRakesh KanniNo ratings yet

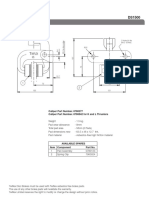

- MS Disc Brake CaliperDocument2 pagesMS Disc Brake Caliperghgh140No ratings yet

- Comprehensive Comparison of 99 Efficient Totem-Pole PFC With Fixed PWM or Variable TCM Switching FrequencyDocument8 pagesComprehensive Comparison of 99 Efficient Totem-Pole PFC With Fixed PWM or Variable TCM Switching FrequencyMuhammad Arsalan FarooqNo ratings yet

- Cambridge International AS and A Level Economics Coursebook CD ROMDocument5 pagesCambridge International AS and A Level Economics Coursebook CD ROMNana Budu Kofi HAYFORDNo ratings yet

- Usurface IIIDocument2 pagesUsurface IIIjanurNo ratings yet

- Java Lab RecordDocument29 pagesJava Lab RecordCyberDootNo ratings yet

- Grade 9: Tle - Ict Computer Systems Servicing Quarter 2 - Module 1 Install Network CablesDocument6 pagesGrade 9: Tle - Ict Computer Systems Servicing Quarter 2 - Module 1 Install Network CablesSharmaine Paragas FaustinoNo ratings yet

- BargeboardsDocument1 pageBargeboardsDavid O'MearaNo ratings yet

- BM3 PlusDocument2 pagesBM3 Pluscicik wijayantiNo ratings yet

- AERVOE 41197pdsDocument2 pagesAERVOE 41197pdsJamer CruzadoNo ratings yet

- Pelina PositionPaperDocument4 pagesPelina PositionPaperJohn Tristan HilaNo ratings yet

- Seminar Topic On Compuetr ForensicsDocument11 pagesSeminar Topic On Compuetr ForensicsS17IT1207Hindu Madhavi100% (1)

- C1 Unit 2Document4 pagesC1 Unit 2Omar AlfaroNo ratings yet

- Huawei FusionServer RH8100 V3 Data SheetDocument4 pagesHuawei FusionServer RH8100 V3 Data Sheetpramod BhattNo ratings yet

- Gyproc Regular BoardsDocument6 pagesGyproc Regular BoardsRadhika Veerala100% (1)

- GE TVSS Specification Data Sheet (TME 65ka - 100ka - Wall Monut)Document3 pagesGE TVSS Specification Data Sheet (TME 65ka - 100ka - Wall Monut)Angela TienNo ratings yet

- 5 HANDGREPEN 1 Horizon - Eng - 0Document28 pages5 HANDGREPEN 1 Horizon - Eng - 0FORLINE nuiNo ratings yet

- AE 321 - Module 07 - FinalDocument14 pagesAE 321 - Module 07 - FinalJohn Client Aclan RanisNo ratings yet

- Do 254 Explained WP PDFDocument6 pagesDo 254 Explained WP PDFmechawebNo ratings yet

- Iso 17632 2015 en PDFDocument11 pagesIso 17632 2015 en PDFalok9870% (1)

- New Gen Trunnion Soft Seat Ball ValveDocument7 pagesNew Gen Trunnion Soft Seat Ball ValvedirtylsuNo ratings yet

- Ecrin 4.0 - Petro BlogDocument4 pagesEcrin 4.0 - Petro BlogReynold AvgNo ratings yet

- Construction Planning and SchedulingDocument70 pagesConstruction Planning and SchedulingDessalegn AyenewNo ratings yet