You might also like

- Financial Statements Formate 3.2Document21 pagesFinancial Statements Formate 3.2vkvivekkm163No ratings yet

- Think of Words That Best Describe Revenues. Expenses Statement of Comprehensive IncomeDocument30 pagesThink of Words That Best Describe Revenues. Expenses Statement of Comprehensive IncomeJasy Nupt GilloNo ratings yet

- Unit 1 Book Keeping, Accounting, AS & IFRS PDFDocument43 pagesUnit 1 Book Keeping, Accounting, AS & IFRS PDFShreyash PardeshiNo ratings yet

- Business Studies Form Four NotesDocument66 pagesBusiness Studies Form Four Notestimothy muyumbiNo ratings yet

- Accounting For Lawyers Part 2: Parvesh AghiDocument46 pagesAccounting For Lawyers Part 2: Parvesh AghiUnknown UnknownNo ratings yet

- Calculating_Profits_for_a_Retailing_BusineSSDocument4 pagesCalculating_Profits_for_a_Retailing_BusineSSRealGenius (Carl)No ratings yet

- Week 5 NotesDocument9 pagesWeek 5 NotescalebNo ratings yet

- Final accounts of sole traderDocument32 pagesFinal accounts of sole tradervickramravi16No ratings yet

- Final AccountDocument47 pagesFinal Accountsakshi tomarNo ratings yet

- B203B-Week 6 - (Accounting-3) Updated 31-10Document38 pagesB203B-Week 6 - (Accounting-3) Updated 31-10ahmed helmyNo ratings yet

- Final Accounts Without AdjustmentsDocument22 pagesFinal Accounts Without AdjustmentsFaizan MisbahuddinNo ratings yet

- Chapter 2. Financial Mangerial ReportingDocument9 pagesChapter 2. Financial Mangerial Reportingnaveen728No ratings yet

- Module 4Document12 pagesModule 4aishwaryaNo ratings yet

- Chapter - 5 Final Accounts: Learning Objectives After Learning This Chapter, You Will Be Able ToDocument41 pagesChapter - 5 Final Accounts: Learning Objectives After Learning This Chapter, You Will Be Able ToPranav SreeNo ratings yet

- Profitability RatioDocument17 pagesProfitability Ratioaayushiji789No ratings yet

- Chapter 6 - MerchandisingDocument44 pagesChapter 6 - MerchandisingMaria FransiscaNo ratings yet

- Review: - Investment? - Return of Investment (ROI) ?Document36 pagesReview: - Investment? - Return of Investment (ROI) ?AthinaNo ratings yet

- CBSE Class 11 Accounting-End of Period AccountsDocument34 pagesCBSE Class 11 Accounting-End of Period AccountsRudraksh PareyNo ratings yet

- Financial, Managerial Accounting and ReportingDocument29 pagesFinancial, Managerial Accounting and ReportingleenajaiswalNo ratings yet

- Sole Proprietorship Final AccountsDocument23 pagesSole Proprietorship Final Accountsjaiccha420No ratings yet

- Lesson: 3.0 Aims and ObjectivesDocument20 pagesLesson: 3.0 Aims and ObjectivesismailakramNo ratings yet

- Final Account 1Document45 pagesFinal Account 1ajaykumar05144375% (4)

- Trial BalanceDocument6 pagesTrial BalanceLefulesele MasiaNo ratings yet

- Fundamentals in Accountancy and Business Management Ii: Specialized Subject: (GRADE 12 First Semester)Document11 pagesFundamentals in Accountancy and Business Management Ii: Specialized Subject: (GRADE 12 First Semester)MarielLee Ramos VillarealNo ratings yet

- Class Notes: Class: XI Topic: Financial StatementDocument3 pagesClass Notes: Class: XI Topic: Financial StatementRajeev ShuklaNo ratings yet

- Manufacturing Account NotesDocument7 pagesManufacturing Account Notesdayna davisNo ratings yet

- 9 Financial Statement - Part ADocument33 pages9 Financial Statement - Part AMariam AhmedNo ratings yet

- Topic 2 - Assets, Equities and Liabilities (1)Document29 pagesTopic 2 - Assets, Equities and Liabilities (1)ahmadamsyar083No ratings yet

- Week 11 Sole Trader AccountsDocument24 pagesWeek 11 Sole Trader AccountsGaba RieleNo ratings yet

- Principles of AccountingDocument19 pagesPrinciples of AccountingDarryl HungweNo ratings yet

- AccountancyDocument45 pagesAccountancyBRISTI SAHANo ratings yet

- Final AccountsDocument7 pagesFinal Accountssubhasishmajumdar0% (2)

- Financial StatementsDocument24 pagesFinancial Statementstranlamtuyen1911No ratings yet

- Final AccountDocument13 pagesFinal AccountBiranchi KumarNo ratings yet

- Cost AccountingDocument17 pagesCost AccountingFaisal RafiqNo ratings yet

- Session 5 Measuring and Reporting Financial PerformanceDocument19 pagesSession 5 Measuring and Reporting Financial PerformanceHoang Tram AnhNo ratings yet

- Financial Statements: I. Income StatementDocument3 pagesFinancial Statements: I. Income StatementKen MateyowNo ratings yet

- M3 T5 Financial StatementsDocument15 pagesM3 T5 Financial StatementsPrshnt MishraNo ratings yet

- Prep Trading - Profit-And-Loss-Ac Balance SheetDocument25 pagesPrep Trading - Profit-And-Loss-Ac Balance Sheetfaltumail379100% (1)

- Final Accouts of Sole Trader FIMS NOTE No - 1Document3 pagesFinal Accouts of Sole Trader FIMS NOTE No - 1arshadpcmongam9895No ratings yet

- Income Statement, Further ConsiderationsDocument26 pagesIncome Statement, Further ConsiderationsRashik RayatNo ratings yet

- Manufacturing - Actual Costing - JBJDocument9 pagesManufacturing - Actual Costing - JBJAlexis Jaina TinaanNo ratings yet

- Inventories Notes2 170419181823Document28 pagesInventories Notes2 170419181823Ebsa AdemeNo ratings yet

- Session 7 and 8 Valuation of InventoryDocument48 pagesSession 7 and 8 Valuation of InventoryReyaan ModhNo ratings yet

- Financial & Managerial AccountingDocument28 pagesFinancial & Managerial AccountingPrabir Kumer RoyNo ratings yet

- 2.preparation of Financial StatementsDocument5 pages2.preparation of Financial StatementsAshutosh MhatreNo ratings yet

- Fingyaan PNLDocument32 pagesFingyaan PNLDeep PadhNo ratings yet

- The Journal of Transactions Type I: No. Date Source Document Account Name Amount DT Amount CT NotesDocument5 pagesThe Journal of Transactions Type I: No. Date Source Document Account Name Amount DT Amount CT NotesGuillermo Oscoz VirtoNo ratings yet

- 3 Statement of IncomeDocument16 pages3 Statement of IncomeMarlon LadesmaNo ratings yet

- Financial Statements Guide for BusinessesDocument6 pagesFinancial Statements Guide for BusinessesRaaghav SrinivasanNo ratings yet

- Income Statement AnalysisDocument5 pagesIncome Statement AnalysisjaneNo ratings yet

- VU Lesson 8Document5 pagesVU Lesson 8ranawaseem100% (1)

- F3 ACCA Financial Accounting - Inventory by MOCDocument10 pagesF3 ACCA Financial Accounting - Inventory by MOCMunyaradzi Onismas Chinyukwi100% (1)

- Final AccountsDocument25 pagesFinal Accountsbarakkat7275% (4)

- Financial StatementsDocument8 pagesFinancial Statementsmanthansaini8923No ratings yet

- MEFA 5 UnitDocument30 pagesMEFA 5 UnitSuhasNo ratings yet

- Comprehensive Income and EquityDocument2 pagesComprehensive Income and EquityLouiseNo ratings yet

- Accounting and Finance Formulas: A Simple IntroductionFrom EverandAccounting and Finance Formulas: A Simple IntroductionRating: 4 out of 5 stars4/5 (8)

- Cash Flow Statement AnalysisDocument11 pagesCash Flow Statement Analysisrscjat100% (1)

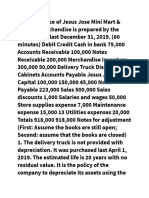

- E Trial Balance of Jesus Jose Mini MartDocument3 pagesE Trial Balance of Jesus Jose Mini Martshamsa ynnaNo ratings yet

- Mids Excel WorkDocument2 pagesMids Excel WorkMuhammad EhtishamNo ratings yet

- Solution Manual For College Accounting 14th Edition Price, Haddock, FarinaDocument18 pagesSolution Manual For College Accounting 14th Edition Price, Haddock, Farinaa289899847No ratings yet

- Accounting Concepts and PrinciplesDocument8 pagesAccounting Concepts and PrinciplesNikki BalsinoNo ratings yet

- ch12 SolDocument12 pagesch12 SolJohn Nigz PayeeNo ratings yet

- HOMEWORK 2 (No. 8&9)Document7 pagesHOMEWORK 2 (No. 8&9)Joana Trinidad100% (1)

- Financial Analysis of TNPLDocument23 pagesFinancial Analysis of TNPLarunprakaash100% (1)

- WACC, Beta, Levered Beta, and Company Financial AnalysisDocument12 pagesWACC, Beta, Levered Beta, and Company Financial AnalysisAnandNo ratings yet

- Adam Kleen's Profit and Loss for 2020Document4 pagesAdam Kleen's Profit and Loss for 2020Kharul AzharNo ratings yet

- Financial Project On Microtek (1) 2Document65 pagesFinancial Project On Microtek (1) 2Rohit Chanana0% (1)

- Gaap Graded2016Document385 pagesGaap Graded2016Venniah Musunda100% (1)

- Wema Bank Financial Statements for Q3 2020Document24 pagesWema Bank Financial Statements for Q3 2020john stonesNo ratings yet

- Parcor 3Document3 pagesParcor 3Joana Mae BalbinNo ratings yet

- Shell Pakistan Limited Balance Sheet As at December 31, 2009Document39 pagesShell Pakistan Limited Balance Sheet As at December 31, 2009Saadia Anwar AliNo ratings yet

- American ApparelDocument18 pagesAmerican Apparelshanul gawshindeNo ratings yet

- Management Accounting - Assignment - Iv (Unit-Iv)Document13 pagesManagement Accounting - Assignment - Iv (Unit-Iv)Ujwal KhanapurkarNo ratings yet

- 105 Final Quiz 4Document8 pages105 Final Quiz 4Donnelly Keith MumarNo ratings yet

- Financial Accounting 2 SummaryDocument10 pagesFinancial Accounting 2 SummaryChoong Xin WeiNo ratings yet

- Consolidation (Study Hub)Document4 pagesConsolidation (Study Hub)HammadNo ratings yet

- Midterm Examination: Accountancy DepartmentDocument15 pagesMidterm Examination: Accountancy DepartmentVincent Larrie MoldezNo ratings yet

- Valix Chapter 20Document22 pagesValix Chapter 20criszel4sobejanaNo ratings yet

- Assessment Test 2nd Cash&RecDocument6 pagesAssessment Test 2nd Cash&RecMellowNo ratings yet

- Merchandise Business Class Performance AnswersDocument14 pagesMerchandise Business Class Performance AnswersLerry RosellNo ratings yet

- Vinamilk Financial Report AnalysisDocument30 pagesVinamilk Financial Report AnalysisThảo PhạmNo ratings yet

- Finance Report 2022Document191 pagesFinance Report 2022Cam TuNo ratings yet

- Ch11 Harrison 8e GE SMDocument91 pagesCh11 Harrison 8e GE SMYeyNo ratings yet

- FIN621 Solved MCQs Finalterm Mega FileDocument23 pagesFIN621 Solved MCQs Finalterm Mega FileKashif Rana50% (4)

- Correction of ErrorsDocument4 pagesCorrection of ErrorsKris Van HalenNo ratings yet

- Accounting Adjustments ExplainedDocument17 pagesAccounting Adjustments ExplainedShiellai Mae PolintangNo ratings yet