You might also like

- 3 "C'S" of Credit: Personal FinanceDocument43 pages3 "C'S" of Credit: Personal FinanceJack RichardsonNo ratings yet

- Repair Your Credit Score: The Ultimate Personal Finance Guide. Learn Effective Credit Repair Strategies, Fix Bad Debt and Improve Your Score.From EverandRepair Your Credit Score: The Ultimate Personal Finance Guide. Learn Effective Credit Repair Strategies, Fix Bad Debt and Improve Your Score.No ratings yet

- Credit Score: The Beginners Guide for Building, Repairing, Raising and Maintaining a Good Credit Score. Includes a Step-by-Step Program to Improve and Boost Your Bank Rating.From EverandCredit Score: The Beginners Guide for Building, Repairing, Raising and Maintaining a Good Credit Score. Includes a Step-by-Step Program to Improve and Boost Your Bank Rating.No ratings yet

- Credit Repair Secrets Learn Proven Steps To Fix And Boost Your Credit Score To 100 Points in 30 days Or LessFrom EverandCredit Repair Secrets Learn Proven Steps To Fix And Boost Your Credit Score To 100 Points in 30 days Or LessNo ratings yet

- Repair and Boost Your Credit Score in 30 Days: How Anyone Can Fix, Repair, and Boost Their Credit Ratings in Less Than 30 DaysFrom EverandRepair and Boost Your Credit Score in 30 Days: How Anyone Can Fix, Repair, and Boost Their Credit Ratings in Less Than 30 DaysNo ratings yet

- ARE YOU SMARTER THAN A CAR DEALER: What Is the DiscountFrom EverandARE YOU SMARTER THAN A CAR DEALER: What Is the DiscountRating: 3.5 out of 5 stars3.5/5 (3)

- Credit Secrets: Learn the concepts of Credit Scores, How to Boost them and Take Advantages from Your Credit CardsFrom EverandCredit Secrets: Learn the concepts of Credit Scores, How to Boost them and Take Advantages from Your Credit CardsNo ratings yet

- Converted: Uncover the Hidden Strategies You Need to Easily Achieve Massive Credit Score Success (Business Edition)From EverandConverted: Uncover the Hidden Strategies You Need to Easily Achieve Massive Credit Score Success (Business Edition)No ratings yet

- Attorney General Letter To Student Loan RepaymentDocument7 pagesAttorney General Letter To Student Loan RepaymentWWMTNo ratings yet

- Letter of Credit (Terms& Conditions& Exhibits)Document3 pagesLetter of Credit (Terms& Conditions& Exhibits)Rnaidoo1972No ratings yet

- Naked Guide to Bonds: What You Need to Know -- Stripped Down to the Bare EssentialsFrom EverandNaked Guide to Bonds: What You Need to Know -- Stripped Down to the Bare EssentialsNo ratings yet

- Constitution of the State of Minnesota — 1974 VersionFrom EverandConstitution of the State of Minnesota — 1974 VersionNo ratings yet

- Credit DeniedDocument2 pagesCredit DeniedAaron SpeareNo ratings yet

- Business Tax Credit For Research And Development A Complete Guide - 2020 EditionFrom EverandBusiness Tax Credit For Research And Development A Complete Guide - 2020 EditionNo ratings yet

- The Insider Secret of Business: Growing Successful Financially and ProductivelyFrom EverandThe Insider Secret of Business: Growing Successful Financially and ProductivelyNo ratings yet

- Quick Tips For Managing Your MoneyDocument12 pagesQuick Tips For Managing Your MoneyRazvanNo ratings yet

- Safe Guarding Your Future: Financial Literacy How a Trusts Can Shield Your Assets & Reduce TaxesFrom EverandSafe Guarding Your Future: Financial Literacy How a Trusts Can Shield Your Assets & Reduce TaxesNo ratings yet

- Power of Attorney and Declaration of RepresentativeDocument2 pagesPower of Attorney and Declaration of Representativepreston_402003No ratings yet

- Constitution of the State of Minnesota — 1876 VersionFrom EverandConstitution of the State of Minnesota — 1876 VersionNo ratings yet

- Credit Report Secrets: How to Understand What Your Credit Report Says About You and What You Can Do About It!From EverandCredit Report Secrets: How to Understand What Your Credit Report Says About You and What You Can Do About It!Rating: 1 out of 5 stars1/5 (1)

- How to Make Your Credit Card Rights Work for You: Save MoneyFrom EverandHow to Make Your Credit Card Rights Work for You: Save MoneyNo ratings yet

- How To File Your Own Bankruptcy: The Step-by-Step Handbook to Filing Your Own Bankruptcy PetitionFrom EverandHow To File Your Own Bankruptcy: The Step-by-Step Handbook to Filing Your Own Bankruptcy PetitionNo ratings yet

- 2018 Bond Official StatementDocument192 pages2018 Bond Official Statementthe kingfishNo ratings yet

- DBA-104-Statutory Durable Power of AttorneyDocument6 pagesDBA-104-Statutory Durable Power of AttorneyIrene HernandezNo ratings yet

- Complainant AffidavitDocument5 pagesComplainant AffidavitMia Steyn100% (1)

- How To Structure Your Business For Success: Everything You Need To Know To Get Started Building Business CreditFrom EverandHow To Structure Your Business For Success: Everything You Need To Know To Get Started Building Business CreditNo ratings yet

- Assignment of Personal FinancingDocument11 pagesAssignment of Personal FinancingRimpy GeraNo ratings yet

- Lawfully Yours: The Realm of Business, Government and LawFrom EverandLawfully Yours: The Realm of Business, Government and LawNo ratings yet

- What Is A Credit Line?: Compare and ContrastDocument5 pagesWhat Is A Credit Line?: Compare and Contrastvivekananda RoyNo ratings yet

- Master Your Debt: Slash Your Monthly Payments and Become Debt FreeFrom EverandMaster Your Debt: Slash Your Monthly Payments and Become Debt FreeRating: 5 out of 5 stars5/5 (1)

- What Is Revolving Credit?Document3 pagesWhat Is Revolving Credit?Niño Rey LopezNo ratings yet

- Be the Bank: "When the Bank Says No or Moves Too Slow" You Are the Bank!From EverandBe the Bank: "When the Bank Says No or Moves Too Slow" You Are the Bank!No ratings yet

- Letter of Credit InstructionsDocument2 pagesLetter of Credit InstructionsHenry Franks100% (2)

- Freedom in Credit Cards: How to Take Charge of Your Life, Your Credit, and Your FutureFrom EverandFreedom in Credit Cards: How to Take Charge of Your Life, Your Credit, and Your FutureNo ratings yet

- 40168collections Lawyer: The Good, The Bad, and The UglyDocument3 pages40168collections Lawyer: The Good, The Bad, and The UglyheldazddsnNo ratings yet

- IAS 12 Income Taxes Standard ExplainedDocument40 pagesIAS 12 Income Taxes Standard ExplainedfurqanNo ratings yet

- Individual Taxpayer 1atax2Document21 pagesIndividual Taxpayer 1atax2Joneric RamosNo ratings yet

- Purchase Unit 116 Tierra Verde TownhomeDocument2 pagesPurchase Unit 116 Tierra Verde Townhomeshrine obenietaNo ratings yet

- De Leon, Misha Laine - CFAS BokkeepingDocument10 pagesDe Leon, Misha Laine - CFAS BokkeepingMisha Laine de LeonNo ratings yet

- East European Wonders Summer 10N-11D International Group Tour Package With FlightDocument10 pagesEast European Wonders Summer 10N-11D International Group Tour Package With FlightFenil ShahNo ratings yet

- Mxbar - PL - Oper: Auto Invoice Execution and Validation ReportDocument4 pagesMxbar - PL - Oper: Auto Invoice Execution and Validation ReportAntonio Arroyo SolanoNo ratings yet

- RA Sushi Bar RestaurantDocument1 pageRA Sushi Bar Restaurantkartheeka3No ratings yet

- Assignment Income Taxation 1 Version 2Document13 pagesAssignment Income Taxation 1 Version 2Juwed Mark TawaliNo ratings yet

- Nairawise Mass MRKT Tier3: First City Monument Bank LimitedDocument3 pagesNairawise Mass MRKT Tier3: First City Monument Bank LimitedJoshua Akorewaye ArigbedeNo ratings yet

- TaxationDocument188 pagesTaxationNikolajay MarrenoNo ratings yet

- SolutionsDocument2 pagesSolutionsJan Aldrin AfosNo ratings yet

- Emirates NBD RatesDocument1 pageEmirates NBD Ratesmanish450inNo ratings yet

- Chapter 3 Accounting For Labor: Review SummaryDocument12 pagesChapter 3 Accounting For Labor: Review SummaryRoann Noguerraza BorjaNo ratings yet

- By Phone: To Contact U.S. Bank: P.O. Box 1800 Saint Paul, Minnesota 55101-0800 9222 IMG S X ST01Document6 pagesBy Phone: To Contact U.S. Bank: P.O. Box 1800 Saint Paul, Minnesota 55101-0800 9222 IMG S X ST01Anna Alexander-BurnfieldNo ratings yet

- LNG Competitors Wages - Aug 2015Document11 pagesLNG Competitors Wages - Aug 2015OctavianNo ratings yet

- Hesco Online BillDocument2 pagesHesco Online BillKiailash KumarNo ratings yet

- American Bureau of Shipping: Atoh Ntumngia ADocument1 pageAmerican Bureau of Shipping: Atoh Ntumngia AhansNo ratings yet

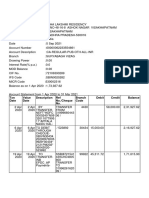

- TXN Date Value Date Description Ref No./Cheque No. Branch Code Debit Credit BalanceDocument28 pagesTXN Date Value Date Description Ref No./Cheque No. Branch Code Debit Credit Balancesv netNo ratings yet

- Client Funds Transfer RequestDocument1 pageClient Funds Transfer RequestAmura FXNo ratings yet

- Affidavits of lossDocument10 pagesAffidavits of lossNorhian Almeron0% (1)

- Est Mai PayDocument21 pagesEst Mai Payeliyas mohammedNo ratings yet

- Tax Problem 2020Document9 pagesTax Problem 2020Justine Ashley SavetNo ratings yet

- Credit Card Processing System UML Use Case DiagramDocument2 pagesCredit Card Processing System UML Use Case DiagramTushar TariNo ratings yet

- Castorama 3DDocument4 pagesCastorama 3Dmarc johanNo ratings yet

- Tax1-Revenue Administrative Order No. 2-2001Document4 pagesTax1-Revenue Administrative Order No. 2-2001SuiNo ratings yet

- Gift Card Hack MethodDocument8 pagesGift Card Hack MethodEphantus0% (1)

- Estimated Duties and Taxes PDFDocument1 pageEstimated Duties and Taxes PDFDianne Bernadeth Cos-agonNo ratings yet

- Use case diagram for payroll systemDocument3 pagesUse case diagram for payroll systemtondeInno100% (2)

- Ra 9504Document5 pagesRa 9504MRose SerranoNo ratings yet

- FRFRDocument3 pagesFRFRNaeem AhmadNo ratings yet