You might also like

- Assignment - Financial MarketsDocument9 pagesAssignment - Financial MarketsTaruntej Singh100% (3)

- Chapter Four Financial Market in The Financial SystemsDocument136 pagesChapter Four Financial Market in The Financial SystemsNatnael Asfaw100% (1)

- Indian Capital Market1Document14 pagesIndian Capital Market1anupsuchakNo ratings yet

- Capital Market Part 1Document13 pagesCapital Market Part 1Nayan Krishna SureshbabuNo ratings yet

- New Issues Market 2Document30 pagesNew Issues Market 2Will RobinsonNo ratings yet

- Financial Markets ManagementDocument15 pagesFinancial Markets ManagementAishwarya SunilkumarNo ratings yet

- Financial MarketsDocument23 pagesFinancial Marketsमहेंद्र सिंह राजपूतNo ratings yet

- Invest MetDocument18 pagesInvest MetDrashti RaichuraNo ratings yet

- Unit III Capital MarketDocument27 pagesUnit III Capital MarketAbin VargheseNo ratings yet

- Primary Market &: The Underwriting of SecurityDocument32 pagesPrimary Market &: The Underwriting of SecuritySumon100% (1)

- Newissuemarket 090919095525 Phpapp01Document31 pagesNewissuemarket 090919095525 Phpapp01Dr-Afzal Basha HSNo ratings yet

- Name:-Gohil Hitesh Roll No: - 17 Subject: - Corporate Finance - I Date: - Submitted To: - Savita MissDocument14 pagesName:-Gohil Hitesh Roll No: - 17 Subject: - Corporate Finance - I Date: - Submitted To: - Savita MissHitesh GohilNo ratings yet

- Topic-1-B New Issue MarketDocument20 pagesTopic-1-B New Issue MarketTushar BhatiNo ratings yet

- IPO Working YetDocument75 pagesIPO Working YetAkash MajjiNo ratings yet

- Primary MarketDocument15 pagesPrimary MarketKapil KumarNo ratings yet

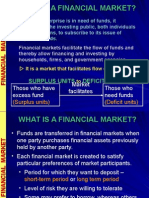

- What Is A Financial Market?Document42 pagesWhat Is A Financial Market?Foram ChhedaNo ratings yet

- IPO Working Yet With Final Edited GraphsDocument73 pagesIPO Working Yet With Final Edited GraphsAkash MajjiNo ratings yet

- Role of Merchant BanksDocument20 pagesRole of Merchant BanksSai Bhaskar Kannepalli100% (1)

- Financial Market - Capital Market - Primary MArketDocument49 pagesFinancial Market - Capital Market - Primary MArketGaurav RathaurNo ratings yet

- Institute: Usb Department: Bba Bachelor of Business AdministrationDocument27 pagesInstitute: Usb Department: Bba Bachelor of Business AdministrationPankajNo ratings yet

- Introduction To Public IssueDocument15 pagesIntroduction To Public IssuePappu ChoudharyNo ratings yet

- Invst LawDocument11 pagesInvst Lawdavissandra817No ratings yet

- New Issue MarketDocument33 pagesNew Issue MarketParul BajajNo ratings yet

- FRP FinalDocument88 pagesFRP Finalgeeta44No ratings yet

- 4th Calss - Raising Capital (IPO)Document33 pages4th Calss - Raising Capital (IPO)Shreeya SigdelNo ratings yet

- New Issue Market: Presentation ONDocument19 pagesNew Issue Market: Presentation ONkaranj321No ratings yet

- Banking DraftDocument6 pagesBanking DraftPritha Behl BhandariNo ratings yet

- Primary MKT Handout !!!Document26 pagesPrimary MKT Handout !!!Garima AroraNo ratings yet

- 3 Investment BankingDocument48 pages3 Investment BankingGigiNo ratings yet

- Newissuemarket 090919095525 Phpapp01Document31 pagesNewissuemarket 090919095525 Phpapp01vikramrajuNo ratings yet

- Investment Banking: Presentation OnDocument56 pagesInvestment Banking: Presentation OnPradeep BandiNo ratings yet

- Fin 205 Unit-3 Part ADocument5 pagesFin 205 Unit-3 Part Agauravktl18No ratings yet

- New Issue MarketDocument31 pagesNew Issue MarketAashish AnandNo ratings yet

- My PartDocument6 pagesMy Partkdoshi23No ratings yet

- Capital MarketDocument6 pagesCapital MarketVithani Bharat100% (1)

- Iapm - Unit-2 & 3 (Mba-3)Document38 pagesIapm - Unit-2 & 3 (Mba-3)Kelvin SavaliyaNo ratings yet

- Capital Primary MarketDocument45 pagesCapital Primary MarketHarsh ThakurNo ratings yet

- Further Reading On Shares and EquitiesDocument6 pagesFurther Reading On Shares and Equitiesshazlina_liNo ratings yet

- Section 1 - Primary MarketsDocument51 pagesSection 1 - Primary MarketsABHINAV AGRAWALNo ratings yet

- Chapter I - IntroductionDocument82 pagesChapter I - IntroductionSai Kumar ChidipothuNo ratings yet

- Capital MarketDocument7 pagesCapital MarketanglrNo ratings yet

- Raising CapitalDocument43 pagesRaising CapitalMuhammad AsifNo ratings yet

- IM Module 2Document57 pagesIM Module 2vanitha gkNo ratings yet

- IPO New Issue MarketDocument19 pagesIPO New Issue MarketDushyant MudgalNo ratings yet

- Capital Market-Part IDocument9 pagesCapital Market-Part ISiya ShuklaNo ratings yet

- Capital Market2Document15 pagesCapital Market2Mohit UpadhyayNo ratings yet

- Unit 3 Primary MarketDocument29 pagesUnit 3 Primary MarkettiwariaradNo ratings yet

- FINS1612 Week 3 Tutorial AnswersDocument11 pagesFINS1612 Week 3 Tutorial Answerspeter kong100% (1)

- New Issue MarketDocument13 pagesNew Issue MarketKanivarasi Hercule100% (2)

- Chp4 Financial MarketsDocument29 pagesChp4 Financial MarketsQais Qazi ZadaNo ratings yet

- The New Issue MarketDocument15 pagesThe New Issue MarketAbanti MukherjeeNo ratings yet

- Stock MarketDocument16 pagesStock MarketHades RiegoNo ratings yet

- Topic 2 - Long Term FinDocument25 pagesTopic 2 - Long Term FinAina KhairunnisaNo ratings yet

- Mod 4 1Document29 pagesMod 4 1David JohnNo ratings yet

- Fmi Unit 3Document26 pagesFmi Unit 3Cabdixakiim-Tiyari Cabdillaahi AadenNo ratings yet

- Chapter 23BBDocument27 pagesChapter 23BBTaVuKieuNhi100% (1)

- P2 Time Value of MoneyDocument45 pagesP2 Time Value of MoneyAkshita GroverNo ratings yet

- A Mini Project On SapmDocument28 pagesA Mini Project On SapmPraveen KumarNo ratings yet

- Raising Long Term FinanceDocument34 pagesRaising Long Term FinanceTiya AmuNo ratings yet

- Mastering the Market: A Comprehensive Guide to Successful Stock InvestingFrom EverandMastering the Market: A Comprehensive Guide to Successful Stock InvestingNo ratings yet

- Mastering the Markets: Advanced Trading Strategies for Success and Ethical Trading PracticesFrom EverandMastering the Markets: Advanced Trading Strategies for Success and Ethical Trading PracticesNo ratings yet

- Stat Chapter 2Document15 pagesStat Chapter 2Hamza AbduremanNo ratings yet

- Chapter Three Interest Rates in The Financial SystemDocument41 pagesChapter Three Interest Rates in The Financial SystemHamza AbduremanNo ratings yet

- Stat Chapter 1Document28 pagesStat Chapter 1Hamza AbduremanNo ratings yet

- Proposal 5Document35 pagesProposal 5Hamza AbduremanNo ratings yet

- Financial System & InstitutionsDocument168 pagesFinancial System & InstitutionsHamza AbduremanNo ratings yet

- Cost and Management Accounting I Chapter 6Document29 pagesCost and Management Accounting I Chapter 6Hamza AbduremanNo ratings yet

- Chapter-Two Money Market AND Capital Market: 2.1. MoneymarketDocument29 pagesChapter-Two Money Market AND Capital Market: 2.1. Moneymarketyared haftuNo ratings yet

- Lecture Notes On Cash and Cash EquivalentsDocument4 pagesLecture Notes On Cash and Cash EquivalentsKeann BrionesNo ratings yet

- Money Markets and Capital MarketsDocument4 pagesMoney Markets and Capital MarketsEmmanuelle RojasNo ratings yet

- Fin 2 Prelim NotesDocument8 pagesFin 2 Prelim NotesChaNo ratings yet

- Money Market: TREASURY BILLS. Treasury Bills (T-Bills) Are Short-Term Notes Issued by The U.SDocument9 pagesMoney Market: TREASURY BILLS. Treasury Bills (T-Bills) Are Short-Term Notes Issued by The U.SArslan AkramNo ratings yet

- Working Capital Management'Document16 pagesWorking Capital Management'Hardeep KaurNo ratings yet

- Kebs108 PDFDocument26 pagesKebs108 PDFvasu kumarNo ratings yet

- Study On Portfolio Management TheoryDocument261 pagesStudy On Portfolio Management TheoryGunjan Resurrected Ranjan0% (1)

- Chap 8Document32 pagesChap 8huha4rever100% (3)

- Money Markets: Financial Markets and Institutions, 10e, Jeff MaduraDocument46 pagesMoney Markets: Financial Markets and Institutions, 10e, Jeff MaduraNurul FitriyahNo ratings yet

- FM 1 Short Term FinancingDocument2 pagesFM 1 Short Term FinancingCrizhae OconNo ratings yet

- Working Capital Unit 1 To 4Document103 pagesWorking Capital Unit 1 To 4tarunNo ratings yet

- Commercial Paper: Presented by Dharani Dharan.m Vijaya Kumar S.BDocument16 pagesCommercial Paper: Presented by Dharani Dharan.m Vijaya Kumar S.Budaya37No ratings yet

- CH 16 - Narrative Report-Short Term Business FinancingDocument13 pagesCH 16 - Narrative Report-Short Term Business Financingjomarybrequillo20No ratings yet

- EIOPA-14-052-Annex IV V - CIC TableDocument4 pagesEIOPA-14-052-Annex IV V - CIC Tablevireya chumputikanNo ratings yet

- Chapter Two Financial Markets and InstrumentsDocument61 pagesChapter Two Financial Markets and InstrumentsKume MezgebuNo ratings yet

- L1 R40 Fixed Income Market Issuance, Trading and Funding - Study Notes (2022)Document25 pagesL1 R40 Fixed Income Market Issuance, Trading and Funding - Study Notes (2022)sumralatifNo ratings yet

- Be 13 - 1 DKKDocument3 pagesBe 13 - 1 DKKMetolit Kelas ANo ratings yet

- Latih Soal Untuk Mhs Fin MGTDocument13 pagesLatih Soal Untuk Mhs Fin MGTnajNo ratings yet

- INVESTMENT MANAGEMENT Mod.Document142 pagesINVESTMENT MANAGEMENT Mod.Terefe DubeNo ratings yet

- Financing Your Franchised BusinessDocument17 pagesFinancing Your Franchised BusinessDanna Marie BanayNo ratings yet

- Great Asian Sales Center Corporation vs. Court of Appeals: VOL. 381, APRIL 25, 2002 557Document25 pagesGreat Asian Sales Center Corporation vs. Court of Appeals: VOL. 381, APRIL 25, 2002 557Joannah SalamatNo ratings yet

- Ipo Prospectus GsDocument164 pagesIpo Prospectus GsSehrish MushtaqNo ratings yet

- BBA Extra TopicsDocument5 pagesBBA Extra TopicsRishabNo ratings yet

- Investment Avenues AssignmentDocument8 pagesInvestment Avenues Assignmentfaisalk95No ratings yet

- Chapter 10 TestbankDocument27 pagesChapter 10 TestbankFami FamzNo ratings yet

- 11.university of Nueva CaceresDocument6 pages11.university of Nueva CaceresNina Sarah Bulanga JamitoNo ratings yet

- Ch06, Money Market Jeff MaduraDocument28 pagesCh06, Money Market Jeff Madurasarah_devinaNo ratings yet

- Busifin Final Period 2021 2022Document46 pagesBusifin Final Period 2021 2022Glenn Mark NochefrancaNo ratings yet