You might also like

- Credit Secrets: Learn the concepts of Credit Scores, How to Boost them and Take Advantages from Your Credit CardsFrom EverandCredit Secrets: Learn the concepts of Credit Scores, How to Boost them and Take Advantages from Your Credit CardsNo ratings yet

- Improve and Increase Your Credit Score: Credit Management Strategies that Will Save You ThousandsFrom EverandImprove and Increase Your Credit Score: Credit Management Strategies that Will Save You ThousandsNo ratings yet

- 2010 BB Brochure EngDocument2 pages2010 BB Brochure EngjoswaroopNo ratings yet

- Banking: What You Should Know About..Document16 pagesBanking: What You Should Know About..Muhammad Fahad AkhterNo ratings yet

- Bank ProductsDocument14 pagesBank ProductsJuhi AgrawalNo ratings yet

- SCR Banking GJKJ - HJHDocument31 pagesSCR Banking GJKJ - HJHamitguptaujjNo ratings yet

- Discover Bank ReviewDocument7 pagesDiscover Bank ReviewyadavrajeNo ratings yet

- Bank, Credit or Thrift? Which One Is Right For MeDocument7 pagesBank, Credit or Thrift? Which One Is Right For MeAnna TrimbleNo ratings yet

- Secrets of Banking IndustryDocument5 pagesSecrets of Banking IndustryFreeman Lawyer100% (2)

- Chapter 4: Money and Banking: Why Use A Bank?Document23 pagesChapter 4: Money and Banking: Why Use A Bank?Jojilyn DabloNo ratings yet

- 2011 BankingBasic Class enDocument55 pages2011 BankingBasic Class enJeevan DeeshaNo ratings yet

- Banking Is Described As The Business of Taking and Securing Money Held by Other People and CompaniesDocument8 pagesBanking Is Described As The Business of Taking and Securing Money Held by Other People and CompaniesTasnim ZaraNo ratings yet

- FM 202 Finals3Document34 pagesFM 202 Finals3sudariodaisyre19No ratings yet

- Current Issues ProjectDocument5 pagesCurrent Issues ProjectSteven SallanderNo ratings yet

- File 1641790871 0004738 BLPDocument118 pagesFile 1641790871 0004738 BLPwww.ishusingh4420No ratings yet

- All The Common Terms and How Bank Makes Money PDFDocument3 pagesAll The Common Terms and How Bank Makes Money PDFMBNo ratings yet

- Banking Organizer & Note TakingDocument8 pagesBanking Organizer & Note TakingRashid DannettNo ratings yet

- Summer 2012 ColorDocument8 pagesSummer 2012 Colorapi-309082881No ratings yet

- Current Issues ProjectDocument6 pagesCurrent Issues ProjectSteven SallanderNo ratings yet

- BankingDocument32 pagesBankingapi-173610472No ratings yet

- Chapter 6 Introduction To Consumer CreditDocument25 pagesChapter 6 Introduction To Consumer CreditshitalNo ratings yet

- BCOM Financial LiteracyDocument11 pagesBCOM Financial LiteracyVivek GabbuerNo ratings yet

- Day To Day Banking Companion Booklet - Scotiabank PDFDocument74 pagesDay To Day Banking Companion Booklet - Scotiabank PDFNhân MaximusNo ratings yet

- l5 - Credit and DebtDocument14 pagesl5 - Credit and Debtapi-190085695No ratings yet

- Muthoot FinanceDocument36 pagesMuthoot FinanceviralNo ratings yet

- 10 Ways To Increase Your Chances of Getting A Credit Card ApprovedDocument1 page10 Ways To Increase Your Chances of Getting A Credit Card ApprovedBhanuka SamarakoonNo ratings yet

- Spring 2014 ColoraDocument8 pagesSpring 2014 Coloraapi-309082881No ratings yet

- Financial Institution Financial IntermediaryDocument15 pagesFinancial Institution Financial IntermediarySayed Nadeem A. KazmiNo ratings yet

- Banking AwarenessDocument18 pagesBanking AwarenessKritika T100% (1)

- Kokan BankDocument20 pagesKokan BankramshaNo ratings yet

- 1 Introduction To BankingDocument8 pages1 Introduction To BankingGurnihalNo ratings yet

- Safari - Oct 13, 2020 at 6:15 PMDocument1 pageSafari - Oct 13, 2020 at 6:15 PMJaboris JohnNo ratings yet

- Unit 4 Banking MbaDocument18 pagesUnit 4 Banking MbaBadal JaiswalNo ratings yet

- 10 Reasons Your Loan Is RejectedDocument11 pages10 Reasons Your Loan Is RejectedSyahmie Ramley100% (1)

- Convenient Monsters: City FinanceDocument11 pagesConvenient Monsters: City FinanceSarthak GargNo ratings yet

- A Project On: "Unethical Business Practices"Document11 pagesA Project On: "Unethical Business Practices"Sampada KadamNo ratings yet

- How To Open A Bank AccountDocument10 pagesHow To Open A Bank AccountKabano CoNo ratings yet

- 2016 Personal Schedule FeesDocument24 pages2016 Personal Schedule FeescampeonpcNo ratings yet

- Chapter 3 - Retail DepositsDocument115 pagesChapter 3 - Retail Depositssudpost4uNo ratings yet

- General InfoDocument15 pagesGeneral Infodhuni143No ratings yet

- The 10 Best Free Bank Accounts: Credit Cards Budgeting Loans & Mortgages Investing Taxes InsuranceDocument19 pagesThe 10 Best Free Bank Accounts: Credit Cards Budgeting Loans & Mortgages Investing Taxes Insurancerhoshelle beleganioNo ratings yet

- Credit ReportsDocument5 pagesCredit ReportscolonelcashNo ratings yet

- What Is A Banking SystemDocument5 pagesWhat Is A Banking SystemDanna MartinezNo ratings yet

- Money and Banking ProjectDocument11 pagesMoney and Banking Projectshahroze ALINo ratings yet

- Checking AccountDocument1 pageChecking AccountWLAMORIE77No ratings yet

- Acca Fundamentals of Accounting (FA1)Document24 pagesAcca Fundamentals of Accounting (FA1)Paredes FlozerenziNo ratings yet

- 10K PrimariesDocument25 pages10K PrimariesCarol67% (3)

- The Essentials. Our Guide To CreditDocument16 pagesThe Essentials. Our Guide To CreditHands OffNo ratings yet

- l5 - Credit and Debt 4Document14 pagesl5 - Credit and Debt 4api-290878974No ratings yet

- Credit FundamentalsDocument15 pagesCredit FundamentalsCody Long100% (2)

- Opening A Bank Account Can Seem IntimidatingDocument9 pagesOpening A Bank Account Can Seem IntimidatingtriratnacomNo ratings yet

- Saving AccountDocument9 pagesSaving AccountpalkhinNo ratings yet

- Credit Cards: Personal FinanceDocument36 pagesCredit Cards: Personal FinanceAmara MaduagwuNo ratings yet

- Equifax (Nyse:: EFX News PeopleDocument4 pagesEquifax (Nyse:: EFX News PeopleMahesh Kumar SomalingaNo ratings yet

- What Is A BankDocument5 pagesWhat Is A BankmanojdunnhumbyNo ratings yet

- Owing WorksheetDocument7 pagesOwing Worksheetapi-273999449No ratings yet

- Barclays Bank ReviewDocument6 pagesBarclays Bank ReviewyadavrajeNo ratings yet

- Reportg6 Soft Copy CreditfinancepracticesDocument10 pagesReportg6 Soft Copy CreditfinancepracticesCEA CardsNo ratings yet

- Understanding Credit: 5 Do's and Don'ts To Getting A Better ScoreDocument2 pagesUnderstanding Credit: 5 Do's and Don'ts To Getting A Better ScoreSean Patrick SmithNo ratings yet

- Dirty Little Secrets: What the Credit Reporting Agencies Won't Tell YouFrom EverandDirty Little Secrets: What the Credit Reporting Agencies Won't Tell YouRating: 3.5 out of 5 stars3.5/5 (3)

- Advanced Accounting - 2015 (Chapter 17) Multiple Choice Solution (Part K)Document1 pageAdvanced Accounting - 2015 (Chapter 17) Multiple Choice Solution (Part K)John Carlos DoringoNo ratings yet

- Fae3e SM ch02Document42 pagesFae3e SM ch02JarkeeNo ratings yet

- Divine Word College of BanguedDocument3 pagesDivine Word College of BanguedAeRis Blancaflor BalsitaNo ratings yet

- Rosetta Stone Case StudyDocument3 pagesRosetta Stone Case StudyEric100% (2)

- Final Project Report of Summer Internship (VK)Document56 pagesFinal Project Report of Summer Internship (VK)Vikas Kumar PatelNo ratings yet

- Fundamentals of Auditing and Assurance Services OverviewDocument8 pagesFundamentals of Auditing and Assurance Services OverviewSkye LeeNo ratings yet

- Financial ManagementDocument11 pagesFinancial ManagementRuel VillanuevaNo ratings yet

- DD MFR FinalDocument105 pagesDD MFR Finalbig johnNo ratings yet

- Guidelines Baseline 4 - Without TTDocument297 pagesGuidelines Baseline 4 - Without TTdarin.vasilevNo ratings yet

- BSBCRT611 BriefDocument2 pagesBSBCRT611 BriefJohnNo ratings yet

- Ratio Analysis at Amararaja Batteries Limited (Arbl) A Project ReportDocument79 pagesRatio Analysis at Amararaja Batteries Limited (Arbl) A Project Reportfahim zamanNo ratings yet

- Bank PO Question and Answer CollectionDocument29 pagesBank PO Question and Answer CollectionAnoop SinghNo ratings yet

- 01 CA Inter Audit Question Bank Part 1 Chapter 0 To Chapter 3Document146 pages01 CA Inter Audit Question Bank Part 1 Chapter 0 To Chapter 3Yash SharmaNo ratings yet

- 4 Hoi and RobinDocument7 pages4 Hoi and RobinelizabetaangelovaNo ratings yet

- Lecture Outline: Share-Based Compensation and Earnings Per ShareDocument3 pagesLecture Outline: Share-Based Compensation and Earnings Per ShareFranz AppleNo ratings yet

- Iskal ArnoDocument37 pagesIskal ArnoRuan0% (1)

- Islamic Banking Situational Mcqs PDFDocument24 pagesIslamic Banking Situational Mcqs PDFNajeeb Magsi100% (1)

- Foreign Exchange Market: Unit HighlightsDocument29 pagesForeign Exchange Market: Unit HighlightsBivas MukherjeeNo ratings yet

- 1910dsycp 11600Document2 pages1910dsycp 11600brandiwinde41No ratings yet

- VPS Form SampleDocument7 pagesVPS Form SampleMuhammad ShariqNo ratings yet

- MODULE 14 Insurance Law EDITEDDocument25 pagesMODULE 14 Insurance Law EDITEDJocelyn GarnadoNo ratings yet

- 14 Reinsurance PDFDocument28 pages14 Reinsurance PDFHalfani MoshiNo ratings yet

- The Depository Trust Company: Important NoticeDocument14 pagesThe Depository Trust Company: Important Noticemehedibinmohammad mohammadNo ratings yet

- Tax Saving Schemes On Mutual FundsDocument10 pagesTax Saving Schemes On Mutual Fundskeshav chandraNo ratings yet

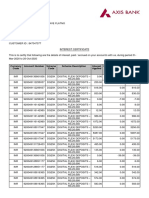

- Interest CertificateDocument2 pagesInterest CertificatesumitNo ratings yet

- BUSI 3309 W24 Assignment 1Document6 pagesBUSI 3309 W24 Assignment 1faridahrushdy5No ratings yet

- Stock Tiger RecommendationDocument11 pagesStock Tiger RecommendationRatilal M JadavNo ratings yet

- Errata Group Statements Vol 2 17th Ed Reprint 2021Document10 pagesErrata Group Statements Vol 2 17th Ed Reprint 2021THABO CLARENCE MohleleNo ratings yet

- La Salle Charter School: Statement of Assets, Liabilities and Net Assets - Modified Cash BasisDocument5 pagesLa Salle Charter School: Statement of Assets, Liabilities and Net Assets - Modified Cash BasisF. O.No ratings yet

- ESG Syllabus V3 16062021finalDocument13 pagesESG Syllabus V3 16062021finalsaabiraNo ratings yet