You might also like

- Ic 11 Top4sure Most Important 'Last Day Revision' Test 1Document27 pagesIc 11 Top4sure Most Important 'Last Day Revision' Test 1Kalyani JayakrishnanNo ratings yet

- Advanced Financial Accounting & Reporting Business CombinationDocument12 pagesAdvanced Financial Accounting & Reporting Business CombinationJunel PlanosNo ratings yet

- Business Combination and Consolidation PDFDocument21 pagesBusiness Combination and Consolidation PDFP.Fabie100% (2)

- Intermediate Accounting 1: a QuickStudy Digital Reference GuideFrom EverandIntermediate Accounting 1: a QuickStudy Digital Reference GuideNo ratings yet

- LGR Finite Ch5Document42 pagesLGR Finite Ch5FrancoSuperNo ratings yet

- Capital Budgeting HandoutDocument15 pagesCapital Budgeting HandoutJoshua Cabinas100% (1)

- Pfrs 3 Business CombinationDocument44 pagesPfrs 3 Business CombinationLindsay MadeloNo ratings yet

- Business Combinations (Part 1)Document21 pagesBusiness Combinations (Part 1)Darryl AgustinNo ratings yet

- Profe03 - Chapter 1 Business Combinations Recognition and MeasurementDocument19 pagesProfe03 - Chapter 1 Business Combinations Recognition and MeasurementSteffany Roque100% (1)

- Accounting For Business For Business CombinationDocument5 pagesAccounting For Business For Business CombinationCharleene GutierrezNo ratings yet

- Accounting Methods For BCDocument7 pagesAccounting Methods For BCFantayNo ratings yet

- 4 DP Business Combination - Acquisition DateDocument6 pages4 DP Business Combination - Acquisition DateYapi BallersNo ratings yet

- AFAR 201808 1 Business Combination Statutory MergersDocument6 pagesAFAR 201808 1 Business Combination Statutory MergersAlarich Catayoc0% (1)

- Business Combinations : Ifrs 3Document45 pagesBusiness Combinations : Ifrs 3alemayehu100% (1)

- 1 PFRS 3 Business CombinationDocument30 pages1 PFRS 3 Business CombinationCharles MateoNo ratings yet

- Summary of IFRS 3 Business CombinationDocument5 pagesSummary of IFRS 3 Business CombinationAbdullah Al RaziNo ratings yet

- BOSCOMDocument18 pagesBOSCOMArah Opalec100% (1)

- Guide To Business CombinationsDocument6 pagesGuide To Business CombinationsClarize R. MabiogNo ratings yet

- PFRS 3, Business Combination: A) Formation of A Joint Venture - PFRS 11, Joint ArrangementsDocument7 pagesPFRS 3, Business Combination: A) Formation of A Joint Venture - PFRS 11, Joint ArrangementsBhosx KimNo ratings yet

- Business Combination - LNDocument9 pagesBusiness Combination - LNAnalyn CenizaNo ratings yet

- Business CombinationDocument36 pagesBusiness CombinationRisalyn BiongNo ratings yet

- Chapter 1 Business Combination - Statutory Merger and Statutory Consolidation - As of 7.13Document4 pagesChapter 1 Business Combination - Statutory Merger and Statutory Consolidation - As of 7.13EyngelNo ratings yet

- Acquirer Obtains Control of One or More Businesses.: ConceptDocument6 pagesAcquirer Obtains Control of One or More Businesses.: ConceptJohn Lexter MacalberNo ratings yet

- Prelim Module 1 Introduction To Business Combination StudentDocument4 pagesPrelim Module 1 Introduction To Business Combination StudentjoshreydugyononNo ratings yet

- Business Combinations: Associate Professor Parmod ChandDocument32 pagesBusiness Combinations: Associate Professor Parmod ChandSunila DeviNo ratings yet

- Business Combination and ConsolidationDocument21 pagesBusiness Combination and ConsolidationRacez Gabon93% (14)

- PFRS 3, Business CombinationsDocument39 pagesPFRS 3, Business Combinationsjulia4razoNo ratings yet

- Business Combination and ConsolidationDocument21 pagesBusiness Combination and ConsolidationCristel TannaganNo ratings yet

- Accbusc Module 1Document20 pagesAccbusc Module 1KATHRYN CLAUDETTE RESENTENo ratings yet

- Ifrs 3Document4 pagesIfrs 3Ken ZafraNo ratings yet

- 3 - Business CombinationDocument28 pages3 - Business Combinationjecille magalongNo ratings yet

- Business CombinationsDocument2 pagesBusiness Combinationsssslll2No ratings yet

- IFRS 3 Business CombinationDocument52 pagesIFRS 3 Business CombinationRusselle Therese DaitolNo ratings yet

- Consolidated Financial Statements by MR - Abdullatif EssajeeDocument37 pagesConsolidated Financial Statements by MR - Abdullatif EssajeeSantoshNo ratings yet

- Methods of Accounting For MergersDocument6 pagesMethods of Accounting For MergersAnwar KhanNo ratings yet

- Business CombinationDocument7 pagesBusiness CombinationJae DenNo ratings yet

- What Is A Business CombinationDocument2 pagesWhat Is A Business CombinationReika OgaliscoNo ratings yet

- CH 2 - Group Financial StatmentDocument47 pagesCH 2 - Group Financial StatmentWedaje AlemayehuNo ratings yet

- Module 1 - Business Combination (IFRS 3)Document15 pagesModule 1 - Business Combination (IFRS 3)MILBERT DE GRACIANo ratings yet

- CRP - Unit Ii - Lecture 1Document26 pagesCRP - Unit Ii - Lecture 1Mudasir KhanNo ratings yet

- Consolidations SummaryDocument9 pagesConsolidations Summaryu22541617No ratings yet

- Accounting For Business CombinationDocument14 pagesAccounting For Business CombinationmiguelroschelleNo ratings yet

- Financial Accounting Sem 4 - CompressedDocument15 pagesFinancial Accounting Sem 4 - CompressedSiddharth SagarNo ratings yet

- Advanced Financial Accounting-I: By: Teshale Berhane (Ass - Prof.)Document58 pagesAdvanced Financial Accounting-I: By: Teshale Berhane (Ass - Prof.)FackallofyouNo ratings yet

- Lecture NotesDocument7 pagesLecture Noteskaren perrerasNo ratings yet

- UNIT I Business CombinationDocument22 pagesUNIT I Business CombinationDaisy TañoteNo ratings yet

- Financial Accounting Sem 4Document15 pagesFinancial Accounting Sem 4Siddharth SagarNo ratings yet

- 01 - Business Comb. - C - 1-77Document77 pages01 - Business Comb. - C - 1-77shankar k.c.No ratings yet

- 02 Acctng-For-Business-Combination-Merger-And-ConsolidationDocument5 pages02 Acctng-For-Business-Combination-Merger-And-ConsolidationMa Jessa Kathryl Alar IINo ratings yet

- Business Combination - Part 1Document5 pagesBusiness Combination - Part 1cpacpacpaNo ratings yet

- ACCO 30023 - Accounting For Business Combination (IM)Document74 pagesACCO 30023 - Accounting For Business Combination (IM)rachel banana hammockNo ratings yet

- Article On Ifrs 3Document8 pagesArticle On Ifrs 3Yagnesh DesaiNo ratings yet

- Chapter 3: Business Combination: Based On IFRS 3Document38 pagesChapter 3: Business Combination: Based On IFRS 3ሔርሞን ይድነቃቸውNo ratings yet

- Business Combinations Part 1Document15 pagesBusiness Combinations Part 1GraciasNo ratings yet

- ProjectDocument23 pagesProjectRACHEL KEDIRNo ratings yet

- bcg02 PDFDocument108 pagesbcg02 PDFAnonymous 4n3M0oHmNo ratings yet

- I. 1. Acquisition Method: Non-Controlling Interest Consolidated StatementDocument14 pagesI. 1. Acquisition Method: Non-Controlling Interest Consolidated StatementCookies And CreamNo ratings yet

- Module1 BuscomDocument27 pagesModule1 BuscomRENZ ALFRED ASTRERONo ratings yet

- 1040 Exam Prep Module III: Items Excluded from Gross IncomeFrom Everand1040 Exam Prep Module III: Items Excluded from Gross IncomeRating: 1 out of 5 stars1/5 (1)

- Textbook of Urgent Care Management: Chapter 46, Urgent Care Center FinancingFrom EverandTextbook of Urgent Care Management: Chapter 46, Urgent Care Center FinancingNo ratings yet

- Financial Intelligence Center - CompressedDocument22 pagesFinancial Intelligence Center - CompressedAbata BageyuNo ratings yet

- Risk Management Training Document For Particip 230312 180018Document226 pagesRisk Management Training Document For Particip 230312 180018Abata BageyuNo ratings yet

- Oromia State University School of Post Graduate Studies Department of Leadership and Change ManagementDocument27 pagesOromia State University School of Post Graduate Studies Department of Leadership and Change ManagementSimaleeNo ratings yet

- Chapter Three Accounting For General and Special Revenue FundsDocument22 pagesChapter Three Accounting For General and Special Revenue Fundshabtamu tadesse100% (2)

- Chapter ThreeDocument62 pagesChapter ThreeAbata BageyuNo ratings yet

- Riskmanagementprocess 231111134414 6c638801Document10 pagesRiskmanagementprocess 231111134414 6c638801Abata BageyuNo ratings yet

- FDM - Fundamentals of Digital Marketing-3-2Document1 pageFDM - Fundamentals of Digital Marketing-3-2Abata BageyuNo ratings yet

- Section 18Document27 pagesSection 18Abata BageyuNo ratings yet

- Proposal-Thesis Guid January 2023Document34 pagesProposal-Thesis Guid January 2023Abata BageyuNo ratings yet

- Project Cost Management - CHAPTER 4Document28 pagesProject Cost Management - CHAPTER 4Abata BageyuNo ratings yet

- Section 11Document30 pagesSection 11Abata BageyuNo ratings yet

- Section 13Document26 pagesSection 13Abata BageyuNo ratings yet

- Section 12Document13 pagesSection 12Abata BageyuNo ratings yet

- Mutual Fund FormateDocument65 pagesMutual Fund Formatesurya prakashNo ratings yet

- Chapter 7 The Accounting Equation RevisedDocument21 pagesChapter 7 The Accounting Equation RevisedJesseca JosafatNo ratings yet

- Ficc Gov RulesDocument326 pagesFicc Gov Rulesdavid floresNo ratings yet

- Auditing Questions and AnswerDocument13 pagesAuditing Questions and AnsweryaregalNo ratings yet

- Riphah University IslamabadDocument34 pagesRiphah University IslamabadIrfy MrtNo ratings yet

- AUDITING Pre-Board 1 Instructions: Select The Correct Answer For Each of The Following Questions. Mark OnlyDocument12 pagesAUDITING Pre-Board 1 Instructions: Select The Correct Answer For Each of The Following Questions. Mark OnlyKathrine Gayle BautistaNo ratings yet

- MB20202 Corporate Finance Unit II Study MaterialsDocument18 pagesMB20202 Corporate Finance Unit II Study MaterialsSarath kumar CNo ratings yet

- Form101 Notice of New DeductionDocument1 pageForm101 Notice of New DeductionJerome BaylonNo ratings yet

- FSCM Digest Incl AdditionalDocument194 pagesFSCM Digest Incl AdditionalCA Kuldeep Pandya100% (1)

- Report On The Preparation of The Annual Financial Statements As atDocument33 pagesReport On The Preparation of The Annual Financial Statements As atElizabeth Sánchez LeónNo ratings yet

- Promissory NoteDocument4 pagesPromissory NoteSatbir TalwarNo ratings yet

- AnnexureDocument2 pagesAnnexureNILESH_373100% (1)

- PF Calculation & Challan ExcelDocument5 pagesPF Calculation & Challan ExcelRahul Dhumal50% (2)

- How To Approach BanksDocument9 pagesHow To Approach BankssohailNo ratings yet

- DR CR DR CR: 1. 2. Trial Balance 31 July 2019 General LedgerDocument1 pageDR CR DR CR: 1. 2. Trial Balance 31 July 2019 General LedgerElvaNo ratings yet

- Mini-Case 1 Ppe AnswerDocument11 pagesMini-Case 1 Ppe Answeryu choong100% (2)

- Cheque Truncation ProjectDocument26 pagesCheque Truncation ProjectReema Dawra0% (1)

- Financial Accounting 11th Edition Albrecht Test BankDocument20 pagesFinancial Accounting 11th Edition Albrecht Test BankBeckyCareyranxj100% (11)

- U85300TG2016PTC109270 T Dnblz22xyhch41Document14 pagesU85300TG2016PTC109270 T Dnblz22xyhch41Aparna DineshNo ratings yet

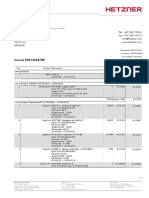

- Hetzner 2021-06-22 R0013604788Document2 pagesHetzner 2021-06-22 R0013604788Vitaliy PodobaNo ratings yet

- Richard Dennis Sonterra Capital Vs Cba Nab Anz Macquarie Gov - Uscourts.nysd.461685.1.0-1Document87 pagesRichard Dennis Sonterra Capital Vs Cba Nab Anz Macquarie Gov - Uscourts.nysd.461685.1.0-1Maverick MinitriesNo ratings yet

- Jawad Hussain: SkillsDocument2 pagesJawad Hussain: SkillsghaziaNo ratings yet

- HBL Id (Key Fact Sheet) - Jul - Dec 2020 PDFDocument1 pageHBL Id (Key Fact Sheet) - Jul - Dec 2020 PDFAli ShahNo ratings yet

- Benefits: Quick Application ProcessDocument8 pagesBenefits: Quick Application ProcessAisyah Rizki Al LathifahNo ratings yet

- Rogers - The Irrelevance of Negotiable Instruments Concepts in The Law ofDocument35 pagesRogers - The Irrelevance of Negotiable Instruments Concepts in The Law ofEins BalagtasNo ratings yet

- Momin 1408101063900Document12 pagesMomin 1408101063900mominalibaigNo ratings yet

- Arup Sinha. Topic - ACI Ltd.Document49 pagesArup Sinha. Topic - ACI Ltd.pranta senNo ratings yet