0% found this document useful (0 votes)

29 views29 pagesChp.4 Supply Analysis

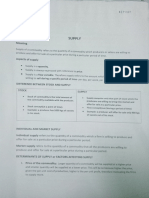

The document discusses the fundamental concepts of supply, stock, and total output in economics, emphasizing the relationship between market price and the quantity of goods producers are willing to supply. It defines key terms such as total output, stock, and supply, and explains the law of supply, which states that higher prices lead to larger quantities supplied. Additionally, it covers variations in supply, cost concepts, and revenue concepts, providing a comprehensive overview of how these elements interact in the market.

Uploaded by

senseidecodeCopyright

© © All Rights Reserved

We take content rights seriously. If you suspect this is your content, claim it here.

Available Formats

Download as PPTX, PDF, TXT or read online on Scribd

0% found this document useful (0 votes)

29 views29 pagesChp.4 Supply Analysis

The document discusses the fundamental concepts of supply, stock, and total output in economics, emphasizing the relationship between market price and the quantity of goods producers are willing to supply. It defines key terms such as total output, stock, and supply, and explains the law of supply, which states that higher prices lead to larger quantities supplied. Additionally, it covers variations in supply, cost concepts, and revenue concepts, providing a comprehensive overview of how these elements interact in the market.

Uploaded by

senseidecodeCopyright

© © All Rights Reserved

We take content rights seriously. If you suspect this is your content, claim it here.

Available Formats

Download as PPTX, PDF, TXT or read online on Scribd