You might also like

- Drilling Fluids Processing HandbookFrom EverandDrilling Fluids Processing HandbookRating: 4.5 out of 5 stars4.5/5 (4)

- QC OnlyDocument5 pagesQC OnlyIyad RabanastaNo ratings yet

- OA Landed CalculationDocument36 pagesOA Landed CalculationAnonymous D8oxvPegNo ratings yet

- Syndicate 2 - Krakatau Steel (A) - PT Berau CoalDocument6 pagesSyndicate 2 - Krakatau Steel (A) - PT Berau CoalSaeful AzizNo ratings yet

- Sadguru Nagrik Sahkari Bank Maryadit, Bhopal: Submitted To: Submitted byDocument43 pagesSadguru Nagrik Sahkari Bank Maryadit, Bhopal: Submitted To: Submitted byAmreen KhanNo ratings yet

- Unit 8&9, Cstps Chandrapur: MERC ParametersDocument15 pagesUnit 8&9, Cstps Chandrapur: MERC ParametersEE POG-III CSTPSNo ratings yet

- Conference15 05Document21 pagesConference15 05David Budi SaputraNo ratings yet

- Facts+Stats: Ski and Snowboard Industry 2014-15Document15 pagesFacts+Stats: Ski and Snowboard Industry 2014-15PatrickLnanduNo ratings yet

- DataDocument16 pagesDataعثمان سلیمNo ratings yet

- Pakistan Energy DataDocument5 pagesPakistan Energy DataNasar RiazNo ratings yet

- Complete Business Plan Handloom - Karpunpuli Muga ClusterDocument48 pagesComplete Business Plan Handloom - Karpunpuli Muga ClusterKashmiri BaruahNo ratings yet

- Sector Briefing - Steel Industry Overview: Fig.2 Major Steel-Producing CountriesDocument2 pagesSector Briefing - Steel Industry Overview: Fig.2 Major Steel-Producing CountriesHimadri SNo ratings yet

- Finance League - Keshav BansalDocument15 pagesFinance League - Keshav BansalJohn DoeNo ratings yet

- Data ImportDocument24 pagesData ImportAnkit VermaNo ratings yet

- Steel SectorDocument38 pagesSteel SectorKamta Prasad SahuNo ratings yet

- BharatBenz Strategy Game Changer AnalysisDocument56 pagesBharatBenz Strategy Game Changer Analysissinharic100% (1)

- Maxime Project ReportDocument60 pagesMaxime Project ReportMOHD GULZARNo ratings yet

- Adipic Market 2Document39 pagesAdipic Market 2John Leonard FazNo ratings yet

- 06 - PT Krakatau PoscoDocument34 pages06 - PT Krakatau PoscoRoyceJONo ratings yet

- Case Study #2 - Ocean CarriersDocument11 pagesCase Study #2 - Ocean CarriersrtrickettNo ratings yet

- IOL Chemicals and Pharmaceuticals LimitedDocument70 pagesIOL Chemicals and Pharmaceuticals Limitedpreshu12No ratings yet

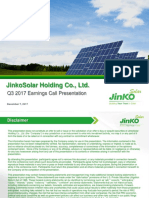

- Jinkosolar Holding Co., LTD.: Q3 2017 Earnings Call PresentationDocument10 pagesJinkosolar Holding Co., LTD.: Q3 2017 Earnings Call PresentationAshutosh KumarNo ratings yet

- 2016 09 Nickel Market Developments PDFDocument12 pages2016 09 Nickel Market Developments PDFsupriNo ratings yet

- Blanko UTDocument5 pagesBlanko UTnovi antiNo ratings yet

- Bronch AdDocument23 pagesBronch AdAbdelrahman NazmiNo ratings yet

- Andritz Presentation GCC Conference 2023 DataDocument11 pagesAndritz Presentation GCC Conference 2023 DataAdam MooseNo ratings yet

- Revenue Cost Profit - 100 AcresDocument26 pagesRevenue Cost Profit - 100 AcresAzhar Ahmad50% (2)

- PT Cost Rate Total Lit Mileage Total KM ('E) Km/Rev Rev ('E) Net RevenueDocument11 pagesPT Cost Rate Total Lit Mileage Total KM ('E) Km/Rev Rev ('E) Net RevenueagraladnNo ratings yet

- Welding Consumable Calculation (WCC) : Doc. No P.O No Rev. No Project Details Technical Requirement ConsumablesDocument10 pagesWelding Consumable Calculation (WCC) : Doc. No P.O No Rev. No Project Details Technical Requirement Consumableskeymal9195No ratings yet

- MODEC, Inc. 2019 Half-Year Financial Results Analysts PresentationDocument16 pagesMODEC, Inc. 2019 Half-Year Financial Results Analysts Presentationfle92No ratings yet

- Indian Steel Industry - An: 69th OECD Steel Committee Meeting Paris 2-3 December 2010Document7 pagesIndian Steel Industry - An: 69th OECD Steel Committee Meeting Paris 2-3 December 2010utsav_8710No ratings yet

- LMI Mixing Digester TanksDocument49 pagesLMI Mixing Digester TanksNicole FelicianoNo ratings yet

- Financials of StartupDocument31 pagesFinancials of StartupJanine PadillaNo ratings yet

- Welding Consumable Calculation (WCC) : Doc. No P.O No Rev. No Project Details Technical Requirement ConsumablesDocument10 pagesWelding Consumable Calculation (WCC) : Doc. No P.O No Rev. No Project Details Technical Requirement Consumableskeymal9195No ratings yet

- Welding Consumable Calculation (WCC) : Doc. No P.O No Rev. No Project Details Technical Requirement ConsumablesDocument10 pagesWelding Consumable Calculation (WCC) : Doc. No P.O No Rev. No Project Details Technical Requirement Consumableskeymal9195No ratings yet

- Fixed Asset Register, MethodsDocument6 pagesFixed Asset Register, Methodsuzma qadirNo ratings yet

- Advisory Altitudes - 19 (2.6 Deg) Advisory Altitudes - 19 (3.0 Deg)Document5 pagesAdvisory Altitudes - 19 (2.6 Deg) Advisory Altitudes - 19 (3.0 Deg)vikas2kNo ratings yet

- So61 - Daily Work Done - Apr 2022Document74 pagesSo61 - Daily Work Done - Apr 2022Purnomo AlfajiNo ratings yet

- Ocean CarriersDocument17 pagesOcean CarriersMridula Hari33% (3)

- Weekly ProgressDocument1 pageWeekly Progresscandex10No ratings yet

- Book 112Document32 pagesBook 112Aditi BhaniramkaNo ratings yet

- D&M Resut CheckDocument25 pagesD&M Resut Checkosama aldresyNo ratings yet

- Calpine SolutionDocument5 pagesCalpine SolutionDarshan GosaliaNo ratings yet

- Turkish Non-Ferrous Foundry Directory 2019Document33 pagesTurkish Non-Ferrous Foundry Directory 2019Kaan KızılkayaNo ratings yet

- UPE Secpropsdimsprops Eurocode3 UK 16-11-2023Document8 pagesUPE Secpropsdimsprops Eurocode3 UK 16-11-2023Zack DaveNo ratings yet

- FIRMS Aggregate Swat Fisheries Production 20101105Document21 pagesFIRMS Aggregate Swat Fisheries Production 20101105Drew SchneiderNo ratings yet

- NewsDocument31 pagesNewsIcc AsrNo ratings yet

- Kawasaki 4 Stroke Vertical EnginesDocument12 pagesKawasaki 4 Stroke Vertical Enginesraja.maharaja789No ratings yet

- Business PlanDocument12 pagesBusiness PlanPapa HarjaiNo ratings yet

- Textiles Gran Fe TextileDocument17 pagesTextiles Gran Fe TextileCanche Adriano DiazNo ratings yet

- Welding Consumable Calculation (WCC) : Doc. No P.O No Rev. No Project Details Technical Requirement ConsumablesDocument10 pagesWelding Consumable Calculation (WCC) : Doc. No P.O No Rev. No Project Details Technical Requirement ConsumablesAhmad KamilNo ratings yet

- Relationship Between Hedge Profit and Jet Fuel PriceDocument4 pagesRelationship Between Hedge Profit and Jet Fuel PriceThomasNo ratings yet

- Strategy SisDocument65 pagesStrategy SisVarunNo ratings yet

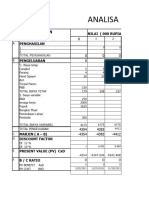

- Solar Roof Top Roi Calculation TemplateDocument5 pagesSolar Roof Top Roi Calculation TemplateSarath Chandra VNo ratings yet

- Filter Media Page 1dimapurDocument10 pagesFilter Media Page 1dimapurAkash SarkarNo ratings yet

- Cash - Cost - EBITDA 2017-2022 FVDocument7 pagesCash - Cost - EBITDA 2017-2022 FVJulian Brescia2No ratings yet

- Specification Sheet: CBB21 Metallized Polypropylene Film CapacitorDocument6 pagesSpecification Sheet: CBB21 Metallized Polypropylene Film Capacitorömer güneşNo ratings yet

- 2017 Annual Report EN PDFDocument160 pages2017 Annual Report EN PDFYuk SimNo ratings yet

- Nouman Sarfaraz: Group Members: - Zaka Ul HassanDocument22 pagesNouman Sarfaraz: Group Members: - Zaka Ul HassanZaka Ul Hassan100% (1)

- Rupsha Power Plant PDFDocument19 pagesRupsha Power Plant PDFHossain Mohammad MahbubNo ratings yet

- Ibps Specialist Officer Cwe Ibps Specialist Officer CweDocument12 pagesIbps Specialist Officer Cwe Ibps Specialist Officer CweGaurav SharmaNo ratings yet

- Brand HierarchyDocument36 pagesBrand HierarchyPrabal SenNo ratings yet

- IntelDocument1 pageIntelPrabal SenNo ratings yet

- Steel Industry in IndiaDocument20 pagesSteel Industry in Indiaranjit pisharodyNo ratings yet

- Performance Highlights - FY 2006: Steel Authority of India LimitedDocument36 pagesPerformance Highlights - FY 2006: Steel Authority of India LimitedPrabal SenNo ratings yet

- Presentation: Sriparna Saha Satya Anvesh Sudheer PrabalDocument16 pagesPresentation: Sriparna Saha Satya Anvesh Sudheer PrabalPrabal SenNo ratings yet

- Leather PuppetryDocument8 pagesLeather PuppetryAnushree BhattacharyaNo ratings yet

- HDO OpeationsDocument28 pagesHDO OpeationsAtif NadeemNo ratings yet

- Revenue Memorandum Circular No. 55-2016: For ExampleDocument2 pagesRevenue Memorandum Circular No. 55-2016: For ExampleFedsNo ratings yet

- Answer: C: Exam Name: Exam Type: Exam Code: Total QuestionsDocument26 pagesAnswer: C: Exam Name: Exam Type: Exam Code: Total QuestionsMohammed S.GoudaNo ratings yet

- Unit-Ii Syllabus: Basic Elements in Solid Waste ManagementDocument14 pagesUnit-Ii Syllabus: Basic Elements in Solid Waste ManagementChaitanya KadambalaNo ratings yet

- Post Renaissance Architecture in EuropeDocument10 pagesPost Renaissance Architecture in Europekali_007No ratings yet

- MEMORANDUM OF AGREEMENT DraftsDocument3 pagesMEMORANDUM OF AGREEMENT DraftsRichard Colunga80% (5)

- Energy Production From Speed BreakerDocument44 pagesEnergy Production From Speed BreakerMuhammad Bilal67% (3)

- DP-1520 PMDocument152 pagesDP-1520 PMIon JardelNo ratings yet

- The Phases of The Moon Station Activity Worksheet Pa2Document3 pagesThe Phases of The Moon Station Activity Worksheet Pa2api-284353863100% (1)

- Properties of WaterDocument23 pagesProperties of WaterNiken Rumani100% (1)

- Legrand Price List-01 ST April-2014Document144 pagesLegrand Price List-01 ST April-2014Umesh SutharNo ratings yet

- Diagnosis ListDocument1 pageDiagnosis ListSenyorita KHayeNo ratings yet

- ID25bc8b496-2013 Dse English PaperDocument2 pagesID25bc8b496-2013 Dse English PaperSimpson WainuiNo ratings yet

- Method Statement FINALDocument61 pagesMethod Statement FINALshareyhou67% (3)

- Art Integrated ProjectDocument14 pagesArt Integrated ProjectSreeti GangulyNo ratings yet

- FluteDocument13 pagesFlutefisher3910% (1)

- Work Sample 2 - Eoc and CrucibleDocument35 pagesWork Sample 2 - Eoc and Crucibleapi-259791703No ratings yet

- The New Art of Photographing Nature - ExcerptDocument15 pagesThe New Art of Photographing Nature - ExcerptCrown Publishing GroupNo ratings yet

- Wordbank 15 Coffee1Document2 pagesWordbank 15 Coffee1akbal13No ratings yet

- Ubicomp PracticalDocument27 pagesUbicomp Practicalvikrant sharmaNo ratings yet

- Prediction of CBR From Index Properties of Cohesive Soils: Magdi ZumrawiDocument1 pagePrediction of CBR From Index Properties of Cohesive Soils: Magdi Zumrawidruwid6No ratings yet

- Painters Rates PDFDocument86 pagesPainters Rates PDFmanthoexNo ratings yet

- Financial Institutions Markets and ServicesDocument2 pagesFinancial Institutions Markets and ServicesPavneet Kaur Bhatia100% (1)

- SCIENCE 11 WEEK 6c - Endogenic ProcessDocument57 pagesSCIENCE 11 WEEK 6c - Endogenic ProcessChristine CayosaNo ratings yet

- (Problem Books in Mathematics) Antonio Caminha Muniz Neto - An Excursion Through Elementary Mathematics, Volume III - Discrete Mathematics and Polynomial Algebra (2018, Springer)Document647 pages(Problem Books in Mathematics) Antonio Caminha Muniz Neto - An Excursion Through Elementary Mathematics, Volume III - Discrete Mathematics and Polynomial Algebra (2018, Springer)Anonymous iH6noeaX7100% (2)

- Acceptable Use Policy 08 19 13 Tia HadleyDocument2 pagesAcceptable Use Policy 08 19 13 Tia Hadleyapi-238178689No ratings yet

- What Is The PCB Shelf Life Extending The Life of PCBsDocument9 pagesWhat Is The PCB Shelf Life Extending The Life of PCBsjackNo ratings yet

- Kiraan Supply Mesin AutomotifDocument6 pagesKiraan Supply Mesin Automotifjamali sadatNo ratings yet

- Dynamic Study of Parabolic Cylindrical Shell A Parametric StudyDocument4 pagesDynamic Study of Parabolic Cylindrical Shell A Parametric StudyEditor IJTSRDNo ratings yet