You might also like

- Group 3 - Master Budget-Earrings UnlimitedDocument8 pagesGroup 3 - Master Budget-Earrings UnlimitedLorena Mae LasquiteNo ratings yet

- Project Case 9-30 Master BudgetDocument6 pagesProject Case 9-30 Master Budgetleizalm29% (7)

- Chapter-7 Pracrice Exercise (Seatwork) Marato, Jedediah SamuelDocument3 pagesChapter-7 Pracrice Exercise (Seatwork) Marato, Jedediah SamuelJedediah Samuel Marato0% (1)

- Includes $2,000 Depreciation Each MonthDocument3 pagesIncludes $2,000 Depreciation Each MonthLynnard Philip Panes100% (1)

- Exercise 1Document5 pagesExercise 1Jade Y80% (5)

- OREN - AC 102 (Quiz 2F)Document4 pagesOREN - AC 102 (Quiz 2F)Leslie Joy OrenNo ratings yet

- Cost Accounting Digos CompanyDocument2 pagesCost Accounting Digos Companyannewilson100% (1)

- Total Excess of Cost Over Book Value Acquired $4,000,000Document5 pagesTotal Excess of Cost Over Book Value Acquired $4,000,000SAHRINDA YUNIAWATINo ratings yet

- Total Excess of Cost Over Book Value Acquired $4,000,000Document5 pagesTotal Excess of Cost Over Book Value Acquired $4,000,000SAHRINDA YUNIAWATINo ratings yet

- A031191120 - Rezky Aprilianti (Latihan Soal P.2-5 & P.2-8)Document2 pagesA031191120 - Rezky Aprilianti (Latihan Soal P.2-5 & P.2-8)Rezky ApriliantiNo ratings yet

- Pertemuan 7Document8 pagesPertemuan 7Sagita RajagukgukNo ratings yet

- 8 Cash Budget Example Solution PDFDocument3 pages8 Cash Budget Example Solution PDFmoss roffattNo ratings yet

- Course Project ADocument9 pagesCourse Project AJay PatelNo ratings yet

- Sazkiya Aldina - Lat Soal AKL 1 Chapter 2Document3 pagesSazkiya Aldina - Lat Soal AKL 1 Chapter 2sazkiyaNo ratings yet

- Multinational Finance Eiteman CH 19 No 5Document4 pagesMultinational Finance Eiteman CH 19 No 5Anugrah Juwita SariNo ratings yet

- Activity OperationsDocument9 pagesActivity OperationsJethro GutlayNo ratings yet

- Raihan Rohadatul 'Aisy - 205154055 - Tugas Consolidations-Changes in Ownership InterestsDocument4 pagesRaihan Rohadatul 'Aisy - 205154055 - Tugas Consolidations-Changes in Ownership InterestsRaihan Rohadatul 'AisyNo ratings yet

- BVPS ReviewerDocument4 pagesBVPS ReviewerDegracia Mia AbegailNo ratings yet

- "Fete N Fiesta" Management Team: Names ShareholdingDocument9 pages"Fete N Fiesta" Management Team: Names ShareholdingMuskan AliNo ratings yet

- December 31 Capital Balance P 180,000 P 120,000: Chi ChuDocument3 pagesDecember 31 Capital Balance P 180,000 P 120,000: Chi ChuBerna LagradaNo ratings yet

- Advanced Accounting CH 14, 15Document16 pagesAdvanced Accounting CH 14, 15jessicaNo ratings yet

- Chapter 8Document3 pagesChapter 8Yasmeen YoussefNo ratings yet

- Book 1Document8 pagesBook 1Alejandra LamasNo ratings yet

- Assignment 3 ACC 401Document9 pagesAssignment 3 ACC 401ShannonNo ratings yet

- Partnership AccountingDocument46 pagesPartnership AccountingAether SkywardNo ratings yet

- Cost Method Vs Equity MethodDocument5 pagesCost Method Vs Equity MethodRahman Ari MulyajiNo ratings yet

- Financial Plan: Start-Up Capital:: Profit Loss StatementDocument6 pagesFinancial Plan: Start-Up Capital:: Profit Loss Statementparthi 23No ratings yet

- 1130 - 89 - Tugas Pribadi Akl Pertemuan 9 Dan 11Document9 pages1130 - 89 - Tugas Pribadi Akl Pertemuan 9 Dan 11Maulana AmriNo ratings yet

- 2021 CH 7 AnswersDocument8 pages2021 CH 7 AnswersMiquel VillamarinNo ratings yet

- PRACTICAL ACCOUNTING 1 Part 2Document9 pagesPRACTICAL ACCOUNTING 1 Part 2Sophia Christina BalagNo ratings yet

- Tugas 2 - AKL 1Document2 pagesTugas 2 - AKL 1Geroro D'PhoenixNo ratings yet

- Group 3 - Compensation Budget Report - Midterm PT GenMathDocument2 pagesGroup 3 - Compensation Budget Report - Midterm PT GenMathShaff LeighNo ratings yet

- Advance Accounting P14-3Document2 pagesAdvance Accounting P14-3Jeremy BastantaNo ratings yet

- Zenaida Solutions To Exercises Chap 14 15 IncompleteDocument8 pagesZenaida Solutions To Exercises Chap 14 15 IncompletekonyatanNo ratings yet

- Answers 8-1: Surname 1Document6 pagesAnswers 8-1: Surname 1Alkadir del AzizNo ratings yet

- Maria Claudine B. Fortaliza. Basic Earnings Per Share Average Shares 1. (IFRS)Document14 pagesMaria Claudine B. Fortaliza. Basic Earnings Per Share Average Shares 1. (IFRS)maria evangelistaNo ratings yet

- Chapter 14Document5 pagesChapter 14Kiminosunoo LelNo ratings yet

- Santos - Solution FinalsDocument3 pagesSantos - Solution FinalsIan SantosNo ratings yet

- Cost Accounting Assignment #2Document5 pagesCost Accounting Assignment #2BRIANNIE ASRI VIVASNo ratings yet

- CFAS2Document7 pagesCFAS2kaji cruzNo ratings yet

- Cap Table Modeling TemplateDocument11 pagesCap Table Modeling Templatericky_stwnNo ratings yet

- Cap Table Modeling TemplateDocument11 pagesCap Table Modeling TemplateAde Hk100% (1)

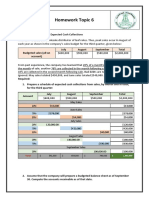

- Homework Topic 6: EXERCISE 8-1 Schedule of Expected Cash CollectionsDocument3 pagesHomework Topic 6: EXERCISE 8-1 Schedule of Expected Cash CollectionskhetamNo ratings yet

- Partnership QuizzerDocument18 pagesPartnership QuizzerJehannahBarat100% (1)

- Pre-Test 10Document2 pagesPre-Test 10BLACKPINKLisaRoseJisooJennieNo ratings yet

- Piecemeal Acquisition-With Minority Interest: Show Your Calculation For The FollowingsDocument13 pagesPiecemeal Acquisition-With Minority Interest: Show Your Calculation For The FollowingsMario KaunangNo ratings yet

- Piecemeal Acquisition-With Minority Interest: Show Your Calculation For The FollowingsDocument13 pagesPiecemeal Acquisition-With Minority Interest: Show Your Calculation For The FollowingsMario KaunangNo ratings yet

- Engineering Economy 8th Edition Blank Solutions Manual 1Document36 pagesEngineering Economy 8th Edition Blank Solutions Manual 1michellejoneskjdeacngzs100% (29)

- A. On November 27, The Board of Directors of India Star Company Declared A $.35 Per ShareDocument109 pagesA. On November 27, The Board of Directors of India Star Company Declared A $.35 Per ShareChris Jay LatibanNo ratings yet

- Acctg Solution Prelim ExamDocument3 pagesAcctg Solution Prelim ExamAbigail ConstantinoNo ratings yet

- Presentasi Kelompok 12 BAB 9Document10 pagesPresentasi Kelompok 12 BAB 9simsonNo ratings yet

- AdvAcct Chapter04 Solutions 07.13Document35 pagesAdvAcct Chapter04 Solutions 07.13Andrew Gladue100% (1)

- Materi 13Document32 pagesMateri 13Elsa RosalindaNo ratings yet

- Proforma of Dale Ct.Document3 pagesProforma of Dale Ct.Wilson4049663818No ratings yet

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsFrom EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsNo ratings yet