You might also like

- StatementDocument4 pagesStatementAaron Montoya100% (1)

- General Principles of LendingDocument3 pagesGeneral Principles of LendingSNo ratings yet

- HOW TO BUY GOOD - LIVE CC FROM SHOP by DC PDFDocument26 pagesHOW TO BUY GOOD - LIVE CC FROM SHOP by DC PDFВиталий Мак100% (7)

- Loan ForgivenessDocument2 pagesLoan Forgivenessslr06dNo ratings yet

- RBI Act 1934 NDocument42 pagesRBI Act 1934 NRohit SinghNo ratings yet

- Sanjay Srinivaas, Sadasiv and KishoreDocument43 pagesSanjay Srinivaas, Sadasiv and KishoreSanjay SrinivaasNo ratings yet

- Credit Markets1Document45 pagesCredit Markets1David Raju GollapudiNo ratings yet

- Jamii Sacco Lipanampesa CodesDocument2 pagesJamii Sacco Lipanampesa CodesKeifer Kaspersky O'brianNo ratings yet

- Documentary CreditDocument29 pagesDocumentary CreditSudershan ThaibaNo ratings yet

- Principles of Sound LendingDocument2 pagesPrinciples of Sound LendingRajat Das100% (1)

- All 18 QSS in One-1 PDFDocument314 pagesAll 18 QSS in One-1 PDFkishan23100% (1)

- Getting Paid On Time 2 EditionDocument104 pagesGetting Paid On Time 2 EditionZipporah NjorogeNo ratings yet

- Chapter 7 Why Do Financial Institutions PDFDocument47 pagesChapter 7 Why Do Financial Institutions PDFHông HoaNo ratings yet

- Credit Score Lecture NotesDocument5 pagesCredit Score Lecture NotesGeri Leine0% (1)

- Report On Consumer Loan Services System of IDLCDocument51 pagesReport On Consumer Loan Services System of IDLCisraatNo ratings yet

- Customer Credit PolicyDocument7 pagesCustomer Credit PolicyMazhar Ali JoyoNo ratings yet

- Terms of PaymentDocument14 pagesTerms of PaymentAnkit VermaNo ratings yet

- Moodys Prodegree EbrochureDocument6 pagesMoodys Prodegree EbrochureJayakumarNo ratings yet

- Assignment Retail BankingDocument3 pagesAssignment Retail BankingSNEHA MARIYAM VARGHESE SIM 16-18No ratings yet

- Secured Loans Vs Unsecured Loans Which Is Right For YouDocument8 pagesSecured Loans Vs Unsecured Loans Which Is Right For YouCredit TriangleNo ratings yet

- Documentary CreditDocument15 pagesDocumentary CreditArmantoCepongNo ratings yet

- Credit Bureau Development in The PhilippinesDocument18 pagesCredit Bureau Development in The PhilippinesRuben Carlo Asuncion100% (4)

- STUDENT Capital and Bond Market UNITDocument24 pagesSTUDENT Capital and Bond Market UNITTetiana VozniukNo ratings yet

- Credit and Collection For The Small Entrepreneur: By: John Xavier S. Chavez, MFMDocument46 pagesCredit and Collection For The Small Entrepreneur: By: John Xavier S. Chavez, MFMRheneir MoraNo ratings yet

- Statutory and Other RestrictionsDocument15 pagesStatutory and Other Restrictionsrgovindan123No ratings yet

- Hire Purchase Meaning - Defination, Nature, ProcessDocument7 pagesHire Purchase Meaning - Defination, Nature, ProcessEkta chodankar67% (3)

- Loan Portfolio Managment JournalDocument1 pageLoan Portfolio Managment Journalwain synergyNo ratings yet

- Loan Application and Agreement Form (Revised October 2018)Document6 pagesLoan Application and Agreement Form (Revised October 2018)Pst Elisha Olando AfwataNo ratings yet

- Treasury Management Report (Grp. 2)Document27 pagesTreasury Management Report (Grp. 2)Dezza Mae GantongNo ratings yet

- Borrowing Powers of CompanyDocument37 pagesBorrowing Powers of CompanyRohan NambiarNo ratings yet

- Banker and CustomerDocument23 pagesBanker and CustomerAnkan Pattanayak100% (1)

- Internship Report On RBBDocument32 pagesInternship Report On RBBAmrit sanjyalNo ratings yet

- Online Reservation SystemDocument1 pageOnline Reservation SystemLavisha DhingraNo ratings yet

- Ans Quiz On Cheques ForMBAsDocument5 pagesAns Quiz On Cheques ForMBAsArpan VishwakarmaNo ratings yet

- Bank ManagementDocument36 pagesBank ManagementMohammed ShaffanNo ratings yet

- Credit Builder ProductsDocument4 pagesCredit Builder ProductsOsborne StricklandNo ratings yet

- Presentation On Financial InstrumentsDocument20 pagesPresentation On Financial InstrumentsMehak BhallaNo ratings yet

- SecuritisationDocument11 pagesSecuritisationamu231286No ratings yet

- Debt Recovery AgentDocument16 pagesDebt Recovery AgentrameshNo ratings yet

- CompendiumDocument18 pagesCompendiumpranithroyNo ratings yet

- Electronic Benefits Transfer (Ebt) Cardholder Frequently Asked QuestionsDocument5 pagesElectronic Benefits Transfer (Ebt) Cardholder Frequently Asked QuestionsBrandon McCainNo ratings yet

- External Commercial BorrowingDocument14 pagesExternal Commercial BorrowingKK SinghNo ratings yet

- Principles For Management of Credit RiskDocument16 pagesPrinciples For Management of Credit RiskZindgiKiKhatirNo ratings yet

- Law Relating To BailmentDocument40 pagesLaw Relating To BailmentTony George PuthucherrilNo ratings yet

- Banking & Financial Markets: Bülent ŞenverDocument73 pagesBanking & Financial Markets: Bülent ŞenverjamesburdenNo ratings yet

- Buyers CreditDocument2 pagesBuyers Creditrao_gmailNo ratings yet

- Factoring ServicesDocument22 pagesFactoring Servicestuktukmaji100% (1)

- Loan Policy of A BanksDocument17 pagesLoan Policy of A Bankssajid bhattiNo ratings yet

- Factors For Rise in NpasDocument10 pagesFactors For Rise in NpasRakesh KushwahNo ratings yet

- Prodigy Finance Brochure (Oct 2017) - 18Document26 pagesProdigy Finance Brochure (Oct 2017) - 18dubstepoNo ratings yet

- Sources of Banks FundDocument21 pagesSources of Banks FundSatendra DubeyNo ratings yet

- AUTO-LOAN FlowchartDocument3 pagesAUTO-LOAN FlowchartArniel Joseph Gerzan GiloNo ratings yet

- CHAPTER I Principles of Lending Types of Credit FacilitiesDocument6 pagesCHAPTER I Principles of Lending Types of Credit Facilitiesanand.action0076127No ratings yet

- Banking FinanceDocument9 pagesBanking FinanceAstik TripathiNo ratings yet

- The Negotiable Instruments Act, 1881Document33 pagesThe Negotiable Instruments Act, 1881Atul JhariyaNo ratings yet

- Question & Answer On CreditDocument60 pagesQuestion & Answer On CreditSubarna palNo ratings yet

- Factoring in Finance ArrangementsDocument9 pagesFactoring in Finance Arrangementsduncanmac200777No ratings yet

- Final Project For Print Out of Fullerton IndiaDocument51 pagesFinal Project For Print Out of Fullerton IndiaVinay Bairagi100% (1)

- Short Sale Seminar Bakersfield, CADocument22 pagesShort Sale Seminar Bakersfield, CAMiguel GarciaNo ratings yet

- Chapter 11 The Money MarketsDocument8 pagesChapter 11 The Money Marketslasha KachkachishviliNo ratings yet

- Treasury Operations In Turkey and Contemporary Sovereign Treasury ManagementFrom EverandTreasury Operations In Turkey and Contemporary Sovereign Treasury ManagementNo ratings yet

- Essentials of Credit, Collections, and Accounts ReceivableFrom EverandEssentials of Credit, Collections, and Accounts ReceivableNo ratings yet

- Digital Banking in India 2016Document21 pagesDigital Banking in India 2016Prof Dr Chowdari Prasad100% (3)

- Consumer Protection Act 1986Document41 pagesConsumer Protection Act 1986Prof Dr Chowdari Prasad100% (1)

- Second Innings September 2019Document52 pagesSecond Innings September 2019Prof Dr Chowdari PrasadNo ratings yet

- 10 International Conference On Problem and Possibilities in Online Education in ManagementDocument39 pages10 International Conference On Problem and Possibilities in Online Education in ManagementProf Dr Chowdari PrasadNo ratings yet

- Prof Chowdari Prasad CV 26112018Document11 pagesProf Chowdari Prasad CV 26112018Prof Dr Chowdari PrasadNo ratings yet

- A Strategy To Connect The Dots For A Big Picture of Indian B-SchoolsDocument15 pagesA Strategy To Connect The Dots For A Big Picture of Indian B-SchoolsProf Dr Chowdari PrasadNo ratings yet

- Performance of Crowd Funding in India: Issues and ChallengesDocument19 pagesPerformance of Crowd Funding in India: Issues and ChallengesProf Dr Chowdari Prasad100% (1)

- Social Entrepreneurship2015Document45 pagesSocial Entrepreneurship2015Prof Dr Chowdari PrasadNo ratings yet

- Lean and Green Banking in India 2012Document20 pagesLean and Green Banking in India 2012Prof Dr Chowdari Prasad100% (2)

- Recent Trends of PE Funding in IndiaDocument38 pagesRecent Trends of PE Funding in IndiaProf Dr Chowdari PrasadNo ratings yet

- HR As A Strategic Business PartnerDocument36 pagesHR As A Strategic Business PartnerProf Dr Chowdari PrasadNo ratings yet

- List of Books On Micro FinanceDocument32 pagesList of Books On Micro FinanceProf Dr Chowdari Prasad71% (7)

- Tapmi Update 2013Document120 pagesTapmi Update 2013Prof Dr Chowdari PrasadNo ratings yet

- Women Achievers Ebook2Document95 pagesWomen Achievers Ebook2Prof Dr Chowdari PrasadNo ratings yet

- Sibm, RBCBDocument20 pagesSibm, RBCBProf Dr Chowdari PrasadNo ratings yet

- Myths of Microfinance - Global South Development Magazine JAN 2011Document42 pagesMyths of Microfinance - Global South Development Magazine JAN 2011Silver Lining CreationNo ratings yet

- Profile of Banks 2010-11Document99 pagesProfile of Banks 2010-11Vishesh KumarNo ratings yet

- The Development Perspective of Finance and Microfinance Sector in China: How Far Is Microfinance Regulations?Document11 pagesThe Development Perspective of Finance and Microfinance Sector in China: How Far Is Microfinance Regulations?Prof Dr Chowdari PrasadNo ratings yet

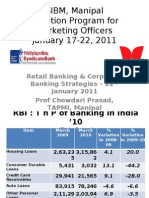

- Syndicate Institute of Bank Management, ManipalDocument67 pagesSyndicate Institute of Bank Management, ManipalProf Dr Chowdari PrasadNo ratings yet

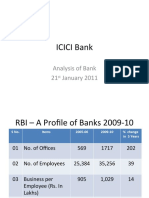

- Icici Bank: Analysis of Bank 21 January 2011Document6 pagesIcici Bank: Analysis of Bank 21 January 2011Prof Dr Chowdari PrasadNo ratings yet

- TAPMI ManipalDocument18 pagesTAPMI ManipalProf Dr Chowdari Prasad100% (1)

- MFI National ConferenceDocument12 pagesMFI National ConferenceProf Dr Chowdari PrasadNo ratings yet

- Economics Project Format: TitleDocument18 pagesEconomics Project Format: TitleKisha OswalNo ratings yet

- 1421843580461Document9 pages1421843580461Aman VermaNo ratings yet

- Act Print 46.HTMLDocument21 pagesAct Print 46.HTMLFaisalNo ratings yet

- Customer Id Gender Age Pincode Account Type KYC Status Locker Average Monthly BalanceDocument26 pagesCustomer Id Gender Age Pincode Account Type KYC Status Locker Average Monthly BalanceAnkita BhuniyaNo ratings yet

- History of BankDocument10 pagesHistory of BankSadaf KhanNo ratings yet

- Statement Details: Transaction Date Posting Date Description Debit Credit Posting Amount Posting Currency Auth CodeDocument2 pagesStatement Details: Transaction Date Posting Date Description Debit Credit Posting Amount Posting Currency Auth CodeTarek KareimNo ratings yet

- TEST-8: Lesson 3 Monetary SystemDocument26 pagesTEST-8: Lesson 3 Monetary SystemDeepak ShahNo ratings yet

- TempBillDocument1 pageTempBillNilesh UmaretiyaNo ratings yet

- Islamic Approaches To MoneyDocument12 pagesIslamic Approaches To Moneyعلي اسحاقيNo ratings yet

- Oakland14chipandskim PDFDocument16 pagesOakland14chipandskim PDFAm RaiNo ratings yet

- Professional Banker Certificate - The Business of Banking and The Economic Environment (Chapter 1)Document38 pagesProfessional Banker Certificate - The Business of Banking and The Economic Environment (Chapter 1)KALKIDAN KASSAHUNNo ratings yet

- SCC Comunicados Pi Batch0100151117a93d91eec74400Document2 pagesSCC Comunicados Pi Batch0100151117a93d91eec74400JilShethNo ratings yet

- Vietnam Central Bank: Roles and FunctionsDocument54 pagesVietnam Central Bank: Roles and FunctionsLinh LeNo ratings yet

- PRESENTED TO:Madam Soniya Ismat Presented By: M.Tashfeen Farhad Shafqat Zara BabarDocument20 pagesPRESENTED TO:Madam Soniya Ismat Presented By: M.Tashfeen Farhad Shafqat Zara BabarTashfeen ShahNo ratings yet

- Simple Loan Amortization TemplateDocument5 pagesSimple Loan Amortization TemplateGíRì BháRàťNo ratings yet

- Hetzner 2022-03-01 R0015282079Document4 pagesHetzner 2022-03-01 R0015282079antonNo ratings yet

- Commercial Transportation Working Analysis HDFC Bank - 2011Document72 pagesCommercial Transportation Working Analysis HDFC Bank - 2011rohitkh28No ratings yet

- LAW (Forgery Assignment)Document4 pagesLAW (Forgery Assignment)Ellen RaballeNo ratings yet

- Standard Chartered Bank PakistanDocument19 pagesStandard Chartered Bank PakistanMuhammad Mubasher Rafique100% (1)

- Account Statement From 21 Jul 2022 To 31 Aug 2022Document3 pagesAccount Statement From 21 Jul 2022 To 31 Aug 2022chinmoy patraNo ratings yet

- Money MarketDocument36 pagesMoney MarketPramod PatjoshiNo ratings yet

- Maharshi Arvind KailashDocument141 pagesMaharshi Arvind Kailashrahulsogani123No ratings yet

- Internship Report On MCB Bank Amc Branch Abbottabad (1320) : Government College of Management Sciences AbbottabadDocument79 pagesInternship Report On MCB Bank Amc Branch Abbottabad (1320) : Government College of Management Sciences AbbottabadFaisal AwanNo ratings yet

- Midterm Exam-Adjusting EntriesDocument5 pagesMidterm Exam-Adjusting EntriesHassanhor Guro BacolodNo ratings yet

- KDDocument5 pagesKDRajeevi parsaNo ratings yet

- NBFC Thematic On Securitisation - Spark - 25nov19Document35 pagesNBFC Thematic On Securitisation - Spark - 25nov19chetankvoraNo ratings yet

- And Dydacomp Multichannel Order Manager GuideDocument22 pagesAnd Dydacomp Multichannel Order Manager GuideDydacompNo ratings yet

- Chapter 3 (IA Proof Od Cash) PDFDocument6 pagesChapter 3 (IA Proof Od Cash) PDFBaby MushroomNo ratings yet