You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5819)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1092)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (845)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (348)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Your PRIMARY SAVINGS JUNIOR Account Summary Your PRIMARY SAVINGS JUNIOR Account SummaryDocument3 pagesYour PRIMARY SAVINGS JUNIOR Account Summary Your PRIMARY SAVINGS JUNIOR Account SummaryDj262022/ /DaviePlaysNo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Invoice No.: 380500045: Payment ReferenceDocument1 pageInvoice No.: 380500045: Payment ReferencePablo Barrio CarvajalNo ratings yet

- Chapter 01 - Introduction To Federal Taxation in CanadaDocument40 pagesChapter 01 - Introduction To Federal Taxation in CanadaDonna So100% (2)

- BIR Ruling 033-00Document3 pagesBIR Ruling 033-00RB Balanay0% (1)

- Income Tax Department: Computerized Payment Receipt (CPR - It)Document3 pagesIncome Tax Department: Computerized Payment Receipt (CPR - It)naeem1990No ratings yet

- Income Tax On Individual TaxpayersDocument7 pagesIncome Tax On Individual TaxpayersYoite MiharuNo ratings yet

- Tax-2Document118 pagesTax-2ethel hyugaNo ratings yet

- Request For Transcript of Tax ReturnDocument2 pagesRequest For Transcript of Tax Returnapi-268415505No ratings yet

- Law of TaxationDocument13 pagesLaw of TaxationRameshNadarNo ratings yet

- Priyanka Salt 1Document46 pagesPriyanka Salt 1Raj GuptaNo ratings yet

- Contoh Report TextDocument1 pageContoh Report TextRandi naufNo ratings yet

- Federal Tax Research 11th Edition Sawyers Test BankDocument35 pagesFederal Tax Research 11th Edition Sawyers Test Bankfactivesiennesewwz2jj100% (24)

- PT Kino Indonesia Tbk. Pay Slip Juli - 2020Document4 pagesPT Kino Indonesia Tbk. Pay Slip Juli - 2020Ananta SaoryNo ratings yet

- Lewis Printing Has Projected Its Sales For The First 8Document1 pageLewis Printing Has Projected Its Sales For The First 8Amit PandeyNo ratings yet

- Invoice Template 5 WordDocument2 pagesInvoice Template 5 WordGuardian Network BangladeshNo ratings yet

- AUSL LMT TaxDocument16 pagesAUSL LMT TaxMaria GarciaNo ratings yet

- 6 Pro InvoiceDocument1 page6 Pro InvoicesanthulohithaNo ratings yet

- Principles of Economics 12Th Edition Case Solutions Manual Full Chapter PDFDocument35 pagesPrinciples of Economics 12Th Edition Case Solutions Manual Full Chapter PDFmirabeltuyenwzp6f100% (9)

- The Purpose of An Interperiod Income Tax Allocation Is ToDocument2 pagesThe Purpose of An Interperiod Income Tax Allocation Is ToAllen Kate100% (1)

- TAX05 - First Preboard ExaminationDocument13 pagesTAX05 - First Preboard ExaminationMIMI LANo ratings yet

- 1st Semester Transfer Taxation Module 3 Estate Taxation - DeductionsDocument13 pages1st Semester Transfer Taxation Module 3 Estate Taxation - DeductionsNah HamzaNo ratings yet

- Reverse Charge MechanismDocument3 pagesReverse Charge MechanismARJUNNo ratings yet

- CMR Payroll On VBA 8.1 - Design by Mr. MBEDocument7 pagesCMR Payroll On VBA 8.1 - Design by Mr. MBEMbecha BenedictNo ratings yet

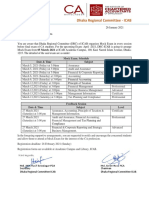

- Dhaka Regional Committee - ICAB: Mock Exam. Schedule Date & Time Subject LevelDocument1 pageDhaka Regional Committee - ICAB: Mock Exam. Schedule Date & Time Subject LevelMd MirazNo ratings yet

- Coursebook Chapter 8 AnswersDocument4 pagesCoursebook Chapter 8 AnswersAhmed Zeeshan100% (9)

- ManojDocument1 pageManojAjit pratap singh BhadauriyaNo ratings yet

- Tax Residence TutorialDocument11 pagesTax Residence TutorialHazlina HusseinNo ratings yet

- 2006 RMO 18-2006 LOA CriteriaDocument3 pages2006 RMO 18-2006 LOA Criteriaedong the greatNo ratings yet

- SOCIAL ArithmeticDocument5 pagesSOCIAL ArithmeticAdek Teguh Rachmawan Anar-qNo ratings yet

- Diskusi 7 Bahasa Inggris NiagaDocument2 pagesDiskusi 7 Bahasa Inggris NiagaRamdhaniNo ratings yet