You might also like

- Housing Snapshot - October 2011Document11 pagesHousing Snapshot - October 2011economicdelusionNo ratings yet

- Personal Finance 101 Canada’S Housing Market Analysis Buying Vs Renting a Home: A Case StudyFrom EverandPersonal Finance 101 Canada’S Housing Market Analysis Buying Vs Renting a Home: A Case StudyNo ratings yet

- 49 - Moody's Analytics-StressTesting Australias Housing Market Mar2014Document17 pages49 - Moody's Analytics-StressTesting Australias Housing Market Mar2014girishrajsNo ratings yet

- RBNZ Perspectives On Housing (April 2013)Document12 pagesRBNZ Perspectives On Housing (April 2013)leithvanonselenNo ratings yet

- Aust House Prices OI 21 2012Document2 pagesAust House Prices OI 21 2012TihoNo ratings yet

- The Great Divide: Australia's Housing Mess and How to Fix It; Quarterly Essay 92From EverandThe Great Divide: Australia's Housing Mess and How to Fix It; Quarterly Essay 92No ratings yet

- Median House Price Report 2001-2011Document28 pagesMedian House Price Report 2001-2011ABC News OnlineNo ratings yet

- Property Report MelbourneDocument0 pagesProperty Report MelbourneMichael JordanNo ratings yet

- NZ Housing Outlook Drives InflationDocument3 pagesNZ Housing Outlook Drives InflationjomanousNo ratings yet

- ANZ Property Industry Confidence Survey December 2013Document7 pagesANZ Property Industry Confidence Survey December 2013leithvanonselenNo ratings yet

- BIS Shrapnel OutlookDocument64 pagesBIS Shrapnel OutlookshengizNo ratings yet

- Global Real Estate Trends (Oct 2009)Document10 pagesGlobal Real Estate Trends (Oct 2009)mintcornerNo ratings yet

- Economic Focus 9-26-11Document1 pageEconomic Focus 9-26-11Jessica Kister-LombardoNo ratings yet

- ANZ Economics Toolbox 20111507Document14 pagesANZ Economics Toolbox 20111507Khoa TranNo ratings yet

- Housing and The Economy: AUTUMN 2013Document16 pagesHousing and The Economy: AUTUMN 2013faidras2No ratings yet

- A Closer Look at Housing Loan Arrears: Box CDocument4 pagesA Closer Look at Housing Loan Arrears: Box CeconomicdelusionNo ratings yet

- February Housing FinanceDocument7 pagesFebruary Housing FinanceBelinda WinkelmanNo ratings yet

- Home Economic Report Oct 21Document2 pagesHome Economic Report Oct 21Adam WahedNo ratings yet

- LSL Acad Scotland HPI News Release May 12Document10 pagesLSL Acad Scotland HPI News Release May 12Stephen EmersonNo ratings yet

- RP Data Rismark Home Value Index Nov 30 2011 FINALwedDocument5 pagesRP Data Rismark Home Value Index Nov 30 2011 FINALwedABC News OnlineNo ratings yet

- Bienville Macro Review (U.S. Housing Update)Document22 pagesBienville Macro Review (U.S. Housing Update)bienvillecapNo ratings yet

- RPData SeptDocument5 pagesRPData SepteconomicdelusionNo ratings yet

- Quarterly Review NOV11Document22 pagesQuarterly Review NOV11ftforee2No ratings yet

- Weekly Sentiment Paper: Distributed By: One Financial Written By: Andrei WogenDocument14 pagesWeekly Sentiment Paper: Distributed By: One Financial Written By: Andrei WogenAndrei Alexander WogenNo ratings yet

- Weekly Economic Commentary 3-26-12Document11 pagesWeekly Economic Commentary 3-26-12monarchadvisorygroupNo ratings yet

- Weekly Economic Commentary 3-26-12Document6 pagesWeekly Economic Commentary 3-26-12monarchadvisorygroupNo ratings yet

- Domain Property Guide 2013Document56 pagesDomain Property Guide 2013El RuloNo ratings yet

- University of Gloucestershire: MBA-1 (GROUP-D)Document13 pagesUniversity of Gloucestershire: MBA-1 (GROUP-D)Nikunj PatelNo ratings yet

- BBAC304 AssessmentDocument17 pagesBBAC304 Assessmentsherryy619No ratings yet

- Weekly Sentiment Paper: Distributed By: One Financial Written By: Andrei WogenDocument17 pagesWeekly Sentiment Paper: Distributed By: One Financial Written By: Andrei WogenAndrei Alexander WogenNo ratings yet

- PRDnationwide Quarterly Economic and Property Report Ed 2 2012Document28 pagesPRDnationwide Quarterly Economic and Property Report Ed 2 2012ashd9410No ratings yet

- Investor IQ One-Page Report - 1Document1 pageInvestor IQ One-Page Report - 1John McClellandNo ratings yet

- 1 2017 - CSRM - WP1 - 2017 - Housing - SupplyDocument30 pages1 2017 - CSRM - WP1 - 2017 - Housing - Supplyharris_saragihNo ratings yet

- Er 20111014 Bull AusconshsepriceexpDocument2 pagesEr 20111014 Bull Ausconshsepriceexpdavid_llewellyn4726No ratings yet

- Factors that could influence residential home prices across United States over the next decadeDocument45 pagesFactors that could influence residential home prices across United States over the next decadeK JagannathNo ratings yet

- ANZ Property Focus Survey Finds Investor Confidence Remains HighDocument16 pagesANZ Property Focus Survey Finds Investor Confidence Remains HighshreyakarNo ratings yet

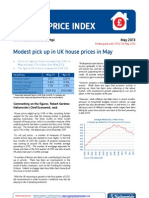

- Modest Pick Up in UK House Prices in MayDocument3 pagesModest Pick Up in UK House Prices in Mayapi-219138607No ratings yet

- Weekly Sentiment Paper: Distributed By: One Financial Written By: Andrei WogenDocument13 pagesWeekly Sentiment Paper: Distributed By: One Financial Written By: Andrei WogenAndrei Alexander WogenNo ratings yet

- AA What Goes Up Often Comes Down Sunday Independent 091005Document2 pagesAA What Goes Up Often Comes Down Sunday Independent 091005BruegelNo ratings yet

- Homebuilding Industry SurveyDocument45 pagesHomebuilding Industry SurveyAhmad So MadNo ratings yet

- Weekly Sentiment Paper: Distributed By: One Financial Written By: Andrei WogenDocument15 pagesWeekly Sentiment Paper: Distributed By: One Financial Written By: Andrei WogenAndrei Alexander WogenNo ratings yet

- Assignment No 8Document12 pagesAssignment No 8Tasneem ShafiqNo ratings yet

- Final Housing Affordability ReportDocument343 pagesFinal Housing Affordability ReportBen RossNo ratings yet

- Onsumer Atch Anada: Canadian Housing Prices - Beware of The AverageDocument4 pagesOnsumer Atch Anada: Canadian Housing Prices - Beware of The AverageSteve LadurantayeNo ratings yet

- ANZ Greater China Weekly Insight 2 April 2013Document13 pagesANZ Greater China Weekly Insight 2 April 2013leithvanonselenNo ratings yet

- Australian Housing Market Causes and Effects of RiDocument13 pagesAustralian Housing Market Causes and Effects of RiNima MoaddeliNo ratings yet

- US Housing Turning the CornerDocument2 pagesUS Housing Turning the CornerJeffNo ratings yet

- Australian Housing Market Causes and Effects of RiDocument12 pagesAustralian Housing Market Causes and Effects of RiNima MoaddeliNo ratings yet

- Crockers Market Research: Further Growth For House Sales, in TimeDocument2 pagesCrockers Market Research: Further Growth For House Sales, in Timepathanfor786No ratings yet

- Economic Focus 1-16-12Document1 pageEconomic Focus 1-16-12Jessica Kister-LombardoNo ratings yet

- Freddie Mac August 2012 Economic OutlookDocument5 pagesFreddie Mac August 2012 Economic OutlookTamara InzunzaNo ratings yet

- Ministry of Finance - Potential Implications of Reducing Foreign Ownership of BC's Housing MarketDocument10 pagesMinistry of Finance - Potential Implications of Reducing Foreign Ownership of BC's Housing MarketCKNW980No ratings yet

- Australian Rental Market Discussion PaperDocument7 pagesAustralian Rental Market Discussion PaperBob odenkirkNo ratings yet

- Housing Tax Reform: Is There A Way Forward? : Special Section - TaxationDocument15 pagesHousing Tax Reform: Is There A Way Forward? : Special Section - TaxationSainada OsaNo ratings yet

- AA Bubble Bursts Sun Business Post 091005Document4 pagesAA Bubble Bursts Sun Business Post 091005BruegelNo ratings yet

- Optimistic Sharon Doop Short StoryDocument5 pagesOptimistic Sharon Doop Short StoryscribdooNo ratings yet

- Hurricane Garage DoorDocument14 pagesHurricane Garage DoorkrisaustinNo ratings yet

- Trends in Track Forecasting For Tropical Cyclones Threatening The UNITED STATES, 1970-2001Document7 pagesTrends in Track Forecasting For Tropical Cyclones Threatening The UNITED STATES, 1970-2001Adam HarperNo ratings yet

- Hurricanes and Global Warming: R. A. P J ., C. L, M. M, J. L, R. PDocument5 pagesHurricanes and Global Warming: R. A. P J ., C. L, M. M, J. L, R. PAdam HarperNo ratings yet

- Hurricane Season Opener MediaAdv FINALDocument1 pageHurricane Season Opener MediaAdv FINAL03h cssNo ratings yet

- Adobe General Terms of Use-20180605 PDFDocument54 pagesAdobe General Terms of Use-20180605 PDFscribdooNo ratings yet

- Adobe General Terms of Use-20180605 PDFDocument54 pagesAdobe General Terms of Use-20180605 PDFscribdooNo ratings yet

- Australian Housing Chartbook July 2012Document13 pagesAustralian Housing Chartbook July 2012scribdooNo ratings yet

- Overview of Adobe Photoshop CS5 WorkspaceDocument10 pagesOverview of Adobe Photoshop CS5 WorkspacescribdooNo ratings yet

- Test Upload 1test Upload 1Document1 pageTest Upload 1test Upload 1scribdooNo ratings yet

- LicenseDocument2 pagesLicensescribdooNo ratings yet

- VMware Business Case For Desktop Virtualization Information GuideDocument33 pagesVMware Business Case For Desktop Virtualization Information GuidescribdooNo ratings yet

- Adobe General Terms of Use-20180605 PDFDocument54 pagesAdobe General Terms of Use-20180605 PDFscribdooNo ratings yet

- ReadmeDocument2 pagesReadmefurious_eNo ratings yet

- LicenseDocument6 pagesLicensexakep_lilNo ratings yet

- Put Unused Plug-Ins in The Optional Directory.Document1 pagePut Unused Plug-Ins in The Optional Directory.andias04No ratings yet

- LicenseDocument6 pagesLicensexakep_lilNo ratings yet

- Higher Algebra - Hall & KnightDocument593 pagesHigher Algebra - Hall & KnightRam Gollamudi100% (2)

- The Warmth of Other Suns: The Epic Story of America's Great MigrationFrom EverandThe Warmth of Other Suns: The Epic Story of America's Great MigrationRating: 4.5 out of 5 stars4.5/5 (1569)

- City of Dreams: The 400-Year Epic History of Immigrant New YorkFrom EverandCity of Dreams: The 400-Year Epic History of Immigrant New YorkRating: 4.5 out of 5 stars4.5/5 (23)

- The Long Way Home: An American Journey from Ellis Island to the Great WarFrom EverandThe Long Way Home: An American Journey from Ellis Island to the Great WarNo ratings yet

- Unforgetting: A Memoir of Family, Migration, Gangs, and Revolution in the AmericasFrom EverandUnforgetting: A Memoir of Family, Migration, Gangs, and Revolution in the AmericasRating: 3.5 out of 5 stars3.5/5 (3)

- The German Genius: Europe's Third Renaissance, the Second Scientific Revolution, and the Twentieth CenturyFrom EverandThe German Genius: Europe's Third Renaissance, the Second Scientific Revolution, and the Twentieth CenturyNo ratings yet

- They Came for Freedom: The Forgotten, Epic Adventure of the PilgrimsFrom EverandThey Came for Freedom: The Forgotten, Epic Adventure of the PilgrimsRating: 4.5 out of 5 stars4.5/5 (11)

- Shackled: One Woman’s Dramatic Triumph Over Persecution, Gender Abuse, and a Death SentenceFrom EverandShackled: One Woman’s Dramatic Triumph Over Persecution, Gender Abuse, and a Death SentenceRating: 5 out of 5 stars5/5 (17)

- The Hard Road Out: One Woman’s Escape From North KoreaFrom EverandThe Hard Road Out: One Woman’s Escape From North KoreaRating: 4.5 out of 5 stars4.5/5 (18)

- Reborn in the USA: An Englishman's Love Letter to His Chosen HomeFrom EverandReborn in the USA: An Englishman's Love Letter to His Chosen HomeRating: 4 out of 5 stars4/5 (17)

- LatinoLand: A Portrait of America's Largest and Least Understood MinorityFrom EverandLatinoLand: A Portrait of America's Largest and Least Understood MinorityNo ratings yet

- You Sound Like a White Girl: The Case for Rejecting AssimilationFrom EverandYou Sound Like a White Girl: The Case for Rejecting AssimilationNo ratings yet

- Fútbol in the Park: Immigrants, Soccer, and the Creation of Social TiesFrom EverandFútbol in the Park: Immigrants, Soccer, and the Creation of Social TiesNo ratings yet

- The Book of Rosy: A Mother's Story of Separation at the BorderFrom EverandThe Book of Rosy: A Mother's Story of Separation at the BorderRating: 4 out of 5 stars4/5 (10)

- Adios, America: The Left's Plan to Turn Our Country into a Third World HellholeFrom EverandAdios, America: The Left's Plan to Turn Our Country into a Third World HellholeRating: 3.5 out of 5 stars3.5/5 (35)

- You Sound Like a White Girl: The Case for Rejecting AssimilationFrom EverandYou Sound Like a White Girl: The Case for Rejecting AssimilationRating: 4.5 out of 5 stars4.5/5 (44)

- A Place at the Nayarit: How a Mexican Restaurant Nourished a CommunityFrom EverandA Place at the Nayarit: How a Mexican Restaurant Nourished a CommunityNo ratings yet

- Titanic Lives: Migrants and Millionaires, Conmen and CrewFrom EverandTitanic Lives: Migrants and Millionaires, Conmen and CrewRating: 4 out of 5 stars4/5 (91)

- Somewhere We Are Human \ Donde somos humanos (Spanish edition): Historias genuinas sobre migración, sobrevivencia y renaceresFrom EverandSomewhere We Are Human \ Donde somos humanos (Spanish edition): Historias genuinas sobre migración, sobrevivencia y renaceresNo ratings yet

- Border and Rule: Global Migration, Capitalism, and the Rise of Racist NationalismFrom EverandBorder and Rule: Global Migration, Capitalism, and the Rise of Racist NationalismRating: 4.5 out of 5 stars4.5/5 (22)

- Dear America: Notes of an Undocumented CitizenFrom EverandDear America: Notes of an Undocumented CitizenRating: 4.5 out of 5 stars4.5/5 (106)

- The Latino Threat: Constructing Immigrants, Citizens, and the Nation, Second EditionFrom EverandThe Latino Threat: Constructing Immigrants, Citizens, and the Nation, Second EditionRating: 5 out of 5 stars5/5 (1)

- We Are Not Refugees: True Stories of the DisplacedFrom EverandWe Are Not Refugees: True Stories of the DisplacedRating: 4.5 out of 5 stars4.5/5 (30)

- The Book of Rosy: A Mother’s Story of Separation at the BorderFrom EverandThe Book of Rosy: A Mother’s Story of Separation at the BorderRating: 4.5 out of 5 stars4.5/5 (28)

- The Border Crossed Us: The Case for Opening the US-Mexico BorderFrom EverandThe Border Crossed Us: The Case for Opening the US-Mexico BorderRating: 5 out of 5 stars5/5 (1)