You might also like

- Cdet Card Profiles v2 3Document178 pagesCdet Card Profiles v2 3Carlos Augusto Calderón De La Barca NeiraNo ratings yet

- Computer Fundamentals TutorialDocument93 pagesComputer Fundamentals TutorialJoy MaryNo ratings yet

- Computer Asisted AccoungtingDocument43 pagesComputer Asisted AccoungtingBosz icon DyliteNo ratings yet

- Computer Script1Document29 pagesComputer Script1AbhinawNo ratings yet

- Introduction To Computer & Emerging TechnologiesDocument30 pagesIntroduction To Computer & Emerging TechnologiesAmv MasterNo ratings yet

- Class 11th Computer Notes Ch1Document30 pagesClass 11th Computer Notes Ch1ashutoshdwivedi968No ratings yet

- Computarised Accounting BestDocument59 pagesComputarised Accounting Bestwambualucas74No ratings yet

- PC Package Unit 1 Introduction To ComputerDocument28 pagesPC Package Unit 1 Introduction To ComputerrameshNo ratings yet

- Computer Computer A AW Wareness Areness: Chapter - 1 Chapter - 1Document13 pagesComputer Computer A AW Wareness Areness: Chapter - 1 Chapter - 1uppaliNo ratings yet

- FOAC Unit-1Document16 pagesFOAC Unit-1krishnapandey77733No ratings yet

- LN 1Document7 pagesLN 1matarabdullah61No ratings yet

- Pptpresentationoncomputerfundamemntal 170831052423Document111 pagesPptpresentationoncomputerfundamemntal 170831052423yaswanthNo ratings yet

- IT Application in BusinessDocument24 pagesIT Application in Businesskodnya.meenuNo ratings yet

- Bcastudyguide Com Computer Fundamental Office Automation CfoaDocument10 pagesBcastudyguide Com Computer Fundamental Office Automation Cfoadharmista p DumasiyaNo ratings yet

- Chapter - 2Document28 pagesChapter - 2oplizoixnNo ratings yet

- Css 111 Lect - 1Document85 pagesCss 111 Lect - 1Darren MgayaNo ratings yet

- Computer FundamentalDocument63 pagesComputer Fundamentalpriyanka groverNo ratings yet

- Computer and Computerised Accounting System: ObjectivesDocument27 pagesComputer and Computerised Accounting System: ObjectivesASILAZA FELIXNo ratings yet

- Computer - ApplicationsDocument61 pagesComputer - ApplicationsJoji Ann UayanNo ratings yet

- Chapter - 1 - BaisDocument27 pagesChapter - 1 - BaisNahom MelakuNo ratings yet

- Accountancy Notes Computer in AccountingDocument3 pagesAccountancy Notes Computer in AccountingYashKhanijo100% (1)

- Chapter One: What Is Computer?Document27 pagesChapter One: What Is Computer?Biniyam DameneNo ratings yet

- Computer AssignmentDocument7 pagesComputer Assignmentaroosh16No ratings yet

- CIS FinalDocument103 pagesCIS FinalAayush ShresthaNo ratings yet

- Comp. Hardware 1stDocument7 pagesComp. Hardware 1stpriyanka groverNo ratings yet

- Itm 1Document24 pagesItm 1chavsNo ratings yet

- Computer: Fundamentals of Computer and IT (BCAC0002) (MODULE-1)Document32 pagesComputer: Fundamentals of Computer and IT (BCAC0002) (MODULE-1)Naman MalikNo ratings yet

- Living in The IT EraDocument12 pagesLiving in The IT EraLilian May MalfartaNo ratings yet

- Fundamental Ch1Document12 pagesFundamental Ch1SubhashreeswainNo ratings yet

- Computer Computer A AW Wareness Areness: Chapter - 1 Chapter - 1Document13 pagesComputer Computer A AW Wareness Areness: Chapter - 1 Chapter - 1hotniliNo ratings yet

- M02-Connect Hardware PeripheralsDocument38 pagesM02-Connect Hardware PeripheralsSolomon SBNo ratings yet

- Unit 1&2 - DCFDocument38 pagesUnit 1&2 - DCF22itu218No ratings yet

- KMB 108 Unit I: Computer Application & Management Information and SystemDocument15 pagesKMB 108 Unit I: Computer Application & Management Information and SystemDeepankar singhNo ratings yet

- AGR315 (Repaired)Document36 pagesAGR315 (Repaired)musaabdullaziz781No ratings yet

- ICT NotesDocument12 pagesICT NotesLakshmi SarvaniNo ratings yet

- Unit - 5 Computer and Computerised Accounting SystemDocument7 pagesUnit - 5 Computer and Computerised Accounting SystemRobin SinghNo ratings yet

- UNIT Ichapter1 (Introduction To Computer)Document12 pagesUNIT Ichapter1 (Introduction To Computer)Vinutha SanthoshNo ratings yet

- Computer Project SEM2 MBADocument42 pagesComputer Project SEM2 MBAPriya PathariyaNo ratings yet

- BasicC NotesDocument70 pagesBasicC NotesChinmayac CnNo ratings yet

- Computer - Introduction Unit1Document7 pagesComputer - Introduction Unit1mailtoprateekk30No ratings yet

- Computer FundamentalDocument75 pagesComputer Fundamentalapi-213911742No ratings yet

- Basics of Computers - Quick Guide - TutorialspointDocument50 pagesBasics of Computers - Quick Guide - TutorialspointJames MukhwanaNo ratings yet

- CPT211 Module 1Document31 pagesCPT211 Module 1maxene jadeNo ratings yet

- IT Applications in Business UNIT I NOTESDocument50 pagesIT Applications in Business UNIT I NOTESTanmay AgrawalNo ratings yet

- Chapter 1 Computer Fundamentals (XI)Document127 pagesChapter 1 Computer Fundamentals (XI)Yohannes Busho100% (1)

- 1.basics of Computers - Quick Guide - TutorialspointDocument47 pages1.basics of Computers - Quick Guide - TutorialspointChinmoyee BiswasNo ratings yet

- Basics of Computers BBADocument14 pagesBasics of Computers BBAsaraNo ratings yet

- Computer Quick Guide - HTMDocument10 pagesComputer Quick Guide - HTMPrashant Khade100% (1)

- Basic ComDocument134 pagesBasic ComRosli MohdNo ratings yet

- Unit3 - Parts of A Computer SystemDocument45 pagesUnit3 - Parts of A Computer SystemJaren QueganNo ratings yet

- Part - 1-General IntroductionDocument19 pagesPart - 1-General IntroductionhunexNo ratings yet

- Intro To Info TechDocument33 pagesIntro To Info TechGrezel NiceNo ratings yet

- Basics of Computer and Its OperationsDocument11 pagesBasics of Computer and Its OperationsKingashiqhussainPanhwerNo ratings yet

- Introduction To ComputerDocument23 pagesIntroduction To ComputerDevid LuizNo ratings yet

- Computer AplicationDocument0 pagesComputer AplicationHareesh YadavNo ratings yet

- Computer FundamentalsDocument66 pagesComputer FundamentalsAlieu BanguraNo ratings yet

- Introduction To Computer Fundamental: April 2013Document200 pagesIntroduction To Computer Fundamental: April 2013Beverly TaniongonNo ratings yet

- Understanding Computers, Smartphones and the InternetFrom EverandUnderstanding Computers, Smartphones and the InternetRating: 5 out of 5 stars5/5 (1)

- ATM (Automated Teller Machine)Document10 pagesATM (Automated Teller Machine)Ram GaneshNo ratings yet

- AtmDocument84 pagesAtmshwetajunejaNo ratings yet

- Case Tool Lab ManualDocument139 pagesCase Tool Lab ManualPRIYA RAJI0% (1)

- iKP - A Family of Secure Electronic Payment ProtocolsDocument18 pagesiKP - A Family of Secure Electronic Payment ProtocolstadilakshmikiranNo ratings yet

- Mobile Phone CloningDocument12 pagesMobile Phone CloningNaveen Kamboj100% (1)

- Account Terms Cards Mastercard enDocument12 pagesAccount Terms Cards Mastercard enHASSAN KocentiniNo ratings yet

- AC-B/C/D3x Family: Standalone Access Control UnitsDocument40 pagesAC-B/C/D3x Family: Standalone Access Control UnitsWinton YUNo ratings yet

- InfyMe InstallationGuide iOSDocument5 pagesInfyMe InstallationGuide iOSSrinivasa GNo ratings yet

- ATM With An EyeDocument15 pagesATM With An EyeBinoy JohnNo ratings yet

- Face Recognition and Fingerprint Based New Generation ATMDocument4 pagesFace Recognition and Fingerprint Based New Generation ATMInternational Journal of Innovative Science and Research TechnologyNo ratings yet

- Welcome To The: 1997 Mid-Atlantic Regional Programming ContestDocument16 pagesWelcome To The: 1997 Mid-Atlantic Regional Programming Contestb1757218No ratings yet

- Biometric ATMDocument17 pagesBiometric ATMSushma100% (1)

- 35c3-9383-Compromising Online Accounts by Cracking Voicemail SystemsDocument56 pages35c3-9383-Compromising Online Accounts by Cracking Voicemail SystemsAndréNo ratings yet

- SBH Bank Form PDFDocument1 pageSBH Bank Form PDFdsNo ratings yet

- Frequently Asked Questions: 1. What Is Cardless Withdrawal?Document5 pagesFrequently Asked Questions: 1. What Is Cardless Withdrawal?joyNo ratings yet

- Motorola W510: User's GuideDocument112 pagesMotorola W510: User's Guidecrysti_reyes4314100% (1)

- AUZao 3 IPv 2 LR 2 AZIDocument7 pagesAUZao 3 IPv 2 LR 2 AZIrajarao001No ratings yet

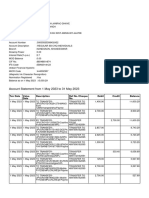

- Account Statement From 1 May 2023 To 31 May 2023: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument10 pagesAccount Statement From 1 May 2023 To 31 May 2023: TXN Date Value Date Description Ref No./Cheque No. Debit Credit Balanceavinashdeshmukh7027No ratings yet

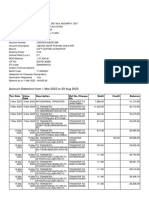

- ZTWD ELt Ne USogw FDocument10 pagesZTWD ELt Ne USogw FSouravDeyNo ratings yet

- DSE 7210 - Installation - InstructionsDocument2 pagesDSE 7210 - Installation - InstructionsAnas BasarahNo ratings yet

- .2021 Signature FormsDocument5 pages.2021 Signature FormsASHLEY GRIESEMER100% (2)

- Triton RL331X Traverse User Operator ManualDocument74 pagesTriton RL331X Traverse User Operator ManualDeezyNo ratings yet

- Form 60Document1 pageForm 60AzImmNo ratings yet

- Terms ConditionsDocument26 pagesTerms ConditionsMADHUR KULSHRESTHANo ratings yet

- User Guide: Nokia 150 Dual SIMDocument23 pagesUser Guide: Nokia 150 Dual SIMΔέσποινα ΜιχάλογλουNo ratings yet

- Fingerprint Lock User Manual: Date: April 2010Document49 pagesFingerprint Lock User Manual: Date: April 2010Markus Tri HartantaNo ratings yet

- An Implementation of NFC Based Restaurant Table ServiceDocument8 pagesAn Implementation of NFC Based Restaurant Table ServiceJunaid M FaisalNo ratings yet

- About Dhanlakshmi Bank LTDDocument16 pagesAbout Dhanlakshmi Bank LTDBanti SinghNo ratings yet