You might also like

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (842)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5807)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1091)

- Music Composer Video Game Developer Written Agreement TEMPLATEDocument2 pagesMusic Composer Video Game Developer Written Agreement TEMPLATEBabrikowski Lucas100% (1)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Tax Quiz 4Document61 pagesTax Quiz 4Seri CrisologoNo ratings yet

- Bahas TPK-TPU-TBIDocument122 pagesBahas TPK-TPU-TBIkiki89% (9)

- Payment HistoryDocument1 pagePayment HistoryRam KumarNo ratings yet

- Indirect Tax Revision Notes-CS Exe June 23 Lyst3130Document56 pagesIndirect Tax Revision Notes-CS Exe June 23 Lyst3130tskpestsolutions.chennaiNo ratings yet

- 1 Program Withdrawal & Refund Form (Merged)Document2 pages1 Program Withdrawal & Refund Form (Merged)Hartek BackupNo ratings yet

- Et Monkwe 0067 Zone 6 (Blackrock Section) Ngobi Hammanskraal 0408Document2 pagesEt Monkwe 0067 Zone 6 (Blackrock Section) Ngobi Hammanskraal 0408EstherNo ratings yet

- Welcome To Ipaymy: SSLI-1727603986-199/3.0Document26 pagesWelcome To Ipaymy: SSLI-1727603986-199/3.0Ngọc Nghĩa PhạmNo ratings yet

- Reservation Agreement 2023 08.23.23 1Document3 pagesReservation Agreement 2023 08.23.23 1Juvelyn LobingcoNo ratings yet

- Installment Sales and Security ContractDocument4 pagesInstallment Sales and Security ContractKrystelle GallegoNo ratings yet

- Mini Sport Catalogue 2008Document116 pagesMini Sport Catalogue 20084x450% (2)

- 8.4.4 EMVCo Contactless SYMBOL Reproduction RequirementsDocument4 pages8.4.4 EMVCo Contactless SYMBOL Reproduction RequirementsMilton SilvaNo ratings yet

- Assignment On NCC BankDocument44 pagesAssignment On NCC Bankhasan633100% (1)

- Acknowledging Orders: Aims: Dealing With Orders: Acknowledging and Advising of DispatchDocument13 pagesAcknowledging Orders: Aims: Dealing With Orders: Acknowledging and Advising of DispatchPecinta bobaNo ratings yet

- Pls Print - 1998 RMO 53-98 - Checklist of Documents To Be Submitted by Taxpayer Upon AuditDocument25 pagesPls Print - 1998 RMO 53-98 - Checklist of Documents To Be Submitted by Taxpayer Upon AuditJoyce CabatanNo ratings yet

- Dining Out. AdvertisingDocument6 pagesDining Out. Advertisingelman imanovNo ratings yet

- Upsc Classroom Online Courses 2023 Vajiram and RaviDocument2 pagesUpsc Classroom Online Courses 2023 Vajiram and RaviSHOUBHIK MUKHERJEENo ratings yet

- Remittance Advice: Total Amount Paid: EUR 900.00Document1 pageRemittance Advice: Total Amount Paid: EUR 900.00maxwell onyekachukwuNo ratings yet

- Debit Cards in VietnamDocument9 pagesDebit Cards in VietnamMai NguyenNo ratings yet

- 0306 Collection of ChequesDocument17 pages0306 Collection of ChequesJitendra Virahyas100% (1)

- BM 2036 I 001684694Document6 pagesBM 2036 I 001684694santhosh kumar murthikaNo ratings yet

- Lecture 3 Assignment - Clever Computer SystemsDocument12 pagesLecture 3 Assignment - Clever Computer SystemsRomeo CaitonaNo ratings yet

- Finon - Week4 - Evolution of Financial ServicesDocument26 pagesFinon - Week4 - Evolution of Financial ServicesNur Intan SariNo ratings yet

- Accounts & Finance 15 Units NOTESDocument180 pagesAccounts & Finance 15 Units NOTESSURYA PRAKASAVELNo ratings yet

- BIU Grad Services Order FormDocument1 pageBIU Grad Services Order FormINSTITUTO DE ENSINO INESPECNo ratings yet

- 102 Master List GlobalDocument3 pages102 Master List GlobalsudharpNo ratings yet

- Liquidation Forms 1Document45 pagesLiquidation Forms 1Ceasar Ryan AsuncionNo ratings yet

- Confirmation For Booking ID 666630860Document1 pageConfirmation For Booking ID 666630860Dela Cruz IrishNo ratings yet

- AIKODocument9 pagesAIKOJessel Andria CañebaNo ratings yet

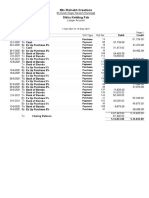

- M/s Rishabh Creations Sikka Knitting FabDocument1 pageM/s Rishabh Creations Sikka Knitting FabVarun AgarwalNo ratings yet