You might also like

- Fiscal Policy, Public Debt Management and Government Bond Markets: The Case For The PhilippinesDocument15 pagesFiscal Policy, Public Debt Management and Government Bond Markets: The Case For The Philippinesashish1981No ratings yet

- Government Borrowing From The Banking System: Implications For Monetary and Financial StabilityDocument26 pagesGovernment Borrowing From The Banking System: Implications For Monetary and Financial StabilitySana NazNo ratings yet

- Lecture 10 - Public DebtDocument34 pagesLecture 10 - Public DebtSidra NazirNo ratings yet

- Economic Outlook: Table 1.1: Macroeconomic IndicatorsDocument9 pagesEconomic Outlook: Table 1.1: Macroeconomic IndicatorsBilal SolangiNo ratings yet

- Analytical Review 2016 17 Budget UKRSDocument31 pagesAnalytical Review 2016 17 Budget UKRSTakhleeq AkhterNo ratings yet

- Domestic & External Debt: 6.1 OverviewDocument12 pagesDomestic & External Debt: 6.1 OverviewSaba JogezaiNo ratings yet

- External Debt and LiabilitiesDocument22 pagesExternal Debt and Liabilitieslaiba SultanNo ratings yet

- 09 External DebtDocument14 pages09 External DebtAmanullah Bashir GilalNo ratings yet

- Fiscal Policy of PakistanDocument9 pagesFiscal Policy of PakistanRehanAdil100% (1)

- 11 Finance and DevelopmentDocument6 pages11 Finance and DevelopmentM IshaqNo ratings yet

- Pakistan: Macroeconomic Assessment and Outlook: Report SeriesDocument8 pagesPakistan: Macroeconomic Assessment and Outlook: Report SeriesHassan Mehmood JamatiNo ratings yet

- External Debt08.pdDocument7 pagesExternal Debt08.pdUmme RubabNo ratings yet

- Fiscal Development: Pakistan Economy 5Document29 pagesFiscal Development: Pakistan Economy 5Danish Riaz ShaikhNo ratings yet

- Chap 4Document9 pagesChap 4Mostofa Mahbub UllahNo ratings yet

- MPD May 11 (Eng)Document3 pagesMPD May 11 (Eng)Osama ZiaNo ratings yet

- Budget DeficitDocument13 pagesBudget DeficitshaziadurraniNo ratings yet

- OverviewDocument9 pagesOverviewsaeed abbasiNo ratings yet

- Domestic and External Debt: 6.2) - The Falling TDL To GDP Ratio ClearlyDocument3 pagesDomestic and External Debt: 6.2) - The Falling TDL To GDP Ratio ClearlySyed Ali ShakeelNo ratings yet

- Budget of Bangladesh FINALDocument4 pagesBudget of Bangladesh FINALSumaiya HoqueNo ratings yet

- The Causes of Economic Crisis in PakistanDocument6 pagesThe Causes of Economic Crisis in PakistanHaris Arif100% (1)

- Monetary Policy of Pakistan: Submitted To: Mirza Aqeel BaigDocument9 pagesMonetary Policy of Pakistan: Submitted To: Mirza Aqeel BaigAli AmjadNo ratings yet

- Analysis of Pakistan's Debt Situation: 2000 2017Document22 pagesAnalysis of Pakistan's Debt Situation: 2000 2017Ayaz Ahmed KhanNo ratings yet

- Debt & Econmy of PaistanDocument15 pagesDebt & Econmy of PaistanSajjad Ahmed ShaikhNo ratings yet

- Monetary Policy Statement: State Bank of PakistanDocument42 pagesMonetary Policy Statement: State Bank of PakistanScorpian MouniehNo ratings yet

- Economic Development: A. GeneralDocument10 pagesEconomic Development: A. GeneralFRankie Bin GRanuleNo ratings yet

- Debt Policy StatementDocument50 pagesDebt Policy StatementMahreen EllahiNo ratings yet

- ICMA Policy Note - Can Pakistan Avert Looming DefaultDocument7 pagesICMA Policy Note - Can Pakistan Avert Looming DefaultJamil KhanNo ratings yet

- Analysis of The Presidents 2012 BudgetDocument9 pagesAnalysis of The Presidents 2012 BudgetCommittee For a Responsible Federal BudgetNo ratings yet

- MPS Apr 2012 EngDocument3 pagesMPS Apr 2012 Engbeyond_ecstasyNo ratings yet

- Economic Survey Pakistan 2007 2008Document132 pagesEconomic Survey Pakistan 2007 2008mrA1mindNo ratings yet

- Monetary Policy Statement: State Bank of PakistanDocument32 pagesMonetary Policy Statement: State Bank of Pakistanbenicepk1329No ratings yet

- DBRS Morningstar Changes Trend On Uruguay To Positive, Confirms at BBB (Low)Document11 pagesDBRS Morningstar Changes Trend On Uruguay To Positive, Confirms at BBB (Low)SubrayadoHDNo ratings yet

- CHP 1Document13 pagesCHP 1Gulfishan MirzaNo ratings yet

- 2007-8 Financial CrisesDocument4 pages2007-8 Financial CrisesHajira alamNo ratings yet

- 1.1 Overview: The State of Pakistan's EconomyDocument47 pages1.1 Overview: The State of Pakistan's EconomysameerghouriNo ratings yet

- Stoking Sentiments - Grp6 Sec BDocument39 pagesStoking Sentiments - Grp6 Sec BrajivNo ratings yet

- Fiscal PolicyDocument49 pagesFiscal PolicyAnum ImranNo ratings yet

- Fiscal DeficitDocument13 pagesFiscal DeficitM. JAHANZAIB UnknownNo ratings yet

- Fiscal Policy 111Document16 pagesFiscal Policy 111Syed Ahsan Hussain XaidiNo ratings yet

- Budget Financing and Debt ManagementDocument7 pagesBudget Financing and Debt ManagementHasan UL KarimNo ratings yet

- 7 TAHIR Public and External Debt SustainabilityDocument25 pages7 TAHIR Public and External Debt SustainabilityMuhammad AhmedNo ratings yet

- Case Study FinalDocument28 pagesCase Study FinalApril Rose Sobrevilla DimpoNo ratings yet

- 2011 Quick StartDocument24 pages2011 Quick StartNick ReismanNo ratings yet

- 3 Fiscal Monetary de DvnevDocument12 pages3 Fiscal Monetary de DvnevSadia WaseemNo ratings yet

- Saint Lucia's Public DebtDocument3 pagesSaint Lucia's Public DebtRichard PeterkinNo ratings yet

- Must Read BOPDocument22 pagesMust Read BOPAnushkaa DattaNo ratings yet

- VN Market Summary 201403Document3 pagesVN Market Summary 201403Giang Khả LinhNo ratings yet

- Public Finances: Outlook and Risks: Carl Emmerson, Soumaya Keynes and Gemma Tetlow (IFS)Document30 pagesPublic Finances: Outlook and Risks: Carl Emmerson, Soumaya Keynes and Gemma Tetlow (IFS)1 2No ratings yet

- Framework Paper - Jonathan Pincus 2017.12.11Document32 pagesFramework Paper - Jonathan Pincus 2017.12.11Thi Minh Hoang NguyenNo ratings yet

- Bevan 2012 Working Paper 1Document47 pagesBevan 2012 Working Paper 1Ellis ElliseusNo ratings yet

- Fiscal Policy Paper FY 2020/21: Government of JamaicaDocument112 pagesFiscal Policy Paper FY 2020/21: Government of JamaicaMecheal ThomasNo ratings yet

- Fiscal Development in PakistanDocument14 pagesFiscal Development in PakistanNasir Jamal100% (1)

- Red Jun 2014Document38 pagesRed Jun 2014hrnanaNo ratings yet

- Federal Budget 2020Document15 pagesFederal Budget 2020Muhammad FarazNo ratings yet

- Business Finance - II: Submitted To Sir Khalid Jamil AnsariDocument8 pagesBusiness Finance - II: Submitted To Sir Khalid Jamil AnsariFari ScorpianNo ratings yet

- MPS Oct 2012 EngDocument2 pagesMPS Oct 2012 EngQamar AftabNo ratings yet

- Paper 1 - Ver3 - Final Debt Profile GA - AG August FINAL 2023Document28 pagesPaper 1 - Ver3 - Final Debt Profile GA - AG August FINAL 2023AlemayehugedaNo ratings yet

- Fiscal Deficit and Forex ReservesDocument12 pagesFiscal Deficit and Forex ReservesBhupeshNo ratings yet

- The Parliamentary Budget Office's Fiscal Sustainability Report 2017Document125 pagesThe Parliamentary Budget Office's Fiscal Sustainability Report 2017caleyramsayNo ratings yet

- Strengthening Fiscal Decentralization in Nepal’s Transition to FederalismFrom EverandStrengthening Fiscal Decentralization in Nepal’s Transition to FederalismNo ratings yet

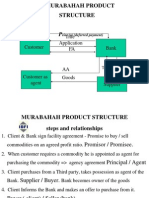

- Murabahah Product Structure: Title Application FADocument26 pagesMurabahah Product Structure: Title Application FAUmair UddinNo ratings yet

- Lab5 SPSS ChiSquareDocument14 pagesLab5 SPSS ChiSquareUmair UddinNo ratings yet

- Problem 1: Relationship Between Two Variables-1 (1) : SW318 Social Work Statistics Slide 1Document20 pagesProblem 1: Relationship Between Two Variables-1 (1) : SW318 Social Work Statistics Slide 1Umair UddinNo ratings yet

- Pakistan, The United States and The IMF: Great Game or A Curious Case of Dutch Disease Without The Oil?Document23 pagesPakistan, The United States and The IMF: Great Game or A Curious Case of Dutch Disease Without The Oil?Umair UddinNo ratings yet

- InterviewsDocument13 pagesInterviewsUmair UddinNo ratings yet

- Chemical Resistance of PlasticsDocument4 pagesChemical Resistance of PlasticsUmair UddinNo ratings yet

- OrganisingDocument10 pagesOrganisingDerik NelsonNo ratings yet

- Epm Course Outline 20 - 21 Bcom-BbaDocument2 pagesEpm Course Outline 20 - 21 Bcom-BbaIanNo ratings yet

- Instructions: How To Use This TemplateDocument20 pagesInstructions: How To Use This TemplatemarsredjoNo ratings yet

- Microinsurance ProjectDocument63 pagesMicroinsurance ProjectNeeraj Kumar83% (35)

- Mergers and AcquisitionsDocument4 pagesMergers and AcquisitionsАлина ХмилевскаяNo ratings yet

- Technical Analysis - Basics - v2 PDFDocument29 pagesTechnical Analysis - Basics - v2 PDFStuart BroodNo ratings yet

- Class XII Economics CH 1 On The Eve of IndependenceDocument5 pagesClass XII Economics CH 1 On The Eve of IndependenceMagic In the airNo ratings yet

- Ishikawajma-Harima Heavy Industries Ltd. Director of Income-TaxDocument6 pagesIshikawajma-Harima Heavy Industries Ltd. Director of Income-TaxpriyaNo ratings yet

- Deamand EcoDocument11 pagesDeamand EcoUmar KundiNo ratings yet

- Entrepreneurship DevelopmentDocument3 pagesEntrepreneurship DevelopmentD06 suraj kumarNo ratings yet

- You Want To Compare The Present Value of $1000 Yearly For 13 Years With $10 000 Now. So You Want To Calculate The Present Value of An AnnuityDocument5 pagesYou Want To Compare The Present Value of $1000 Yearly For 13 Years With $10 000 Now. So You Want To Calculate The Present Value of An AnnuityBikram ChitrakarNo ratings yet

- Financial Delegated Authorities Policy: 1 PurposeDocument10 pagesFinancial Delegated Authorities Policy: 1 PurposetinmaungtheinNo ratings yet

- Session 10 (Role of The Regulatory Framework - SEBI, TRAI, RBI and Role of Board of Directors Corporate Governance - The Indian Scenario.)Document11 pagesSession 10 (Role of The Regulatory Framework - SEBI, TRAI, RBI and Role of Board of Directors Corporate Governance - The Indian Scenario.)Shubham Jaiswal (PGDM 18-20)No ratings yet

- HR ComparisonDocument4 pagesHR ComparisonNobiaWahabNo ratings yet

- Capital Mobility in Developing CountriesDocument41 pagesCapital Mobility in Developing CountriesEmir TermeNo ratings yet

- Dummy ProjectDocument42 pagesDummy Projectuday bansalNo ratings yet

- Chapter 2Document2 pagesChapter 211.15. Hoàng Nguyễn Thanh HươngNo ratings yet

- GourmetDocument12 pagesGourmetTalha RiazNo ratings yet

- Acc203 Tut On LiquidationDocument7 pagesAcc203 Tut On LiquidationShivanjani KumarNo ratings yet

- Serra GorpeDocument255 pagesSerra GorpePop L. AndreeaNo ratings yet

- Price and Volume Effects of Devaluation of CurrencyDocument3 pagesPrice and Volume Effects of Devaluation of Currencymutale besaNo ratings yet

- Handout On Losses - Part 1aDocument6 pagesHandout On Losses - Part 1aGlyds D. UrbanoNo ratings yet

- Kyzer Software - Resourcing Services v1.91Document8 pagesKyzer Software - Resourcing Services v1.91rupen.bavdhankarNo ratings yet

- Aug2023Document14 pagesAug2023Piyush NagarNo ratings yet

- Content Marketing Solution StudyDocument39 pagesContent Marketing Solution StudyDemand Metric100% (2)

- By Christopher B. Leinberger: & Patrick LynchDocument29 pagesBy Christopher B. Leinberger: & Patrick LynchSheila EnglishNo ratings yet

- Solution Ultimate Sample Paper 4Document5 pagesSolution Ultimate Sample Paper 4Karthick KarthickNo ratings yet

- CHEMICAL INDUSTRY PresentationDocument18 pagesCHEMICAL INDUSTRY PresentationPrashant MirguleNo ratings yet

- International Economics 14th Edition Robert Carbaugh Test Bank 1Document26 pagesInternational Economics 14th Edition Robert Carbaugh Test Bank 1pamela100% (44)

- Borzo Global Markets & Competition Research India Grocery SegmentDocument3 pagesBorzo Global Markets & Competition Research India Grocery Segmentpavelthai5No ratings yet