You might also like

- Study On HRM Practices Followed in Power Generation Sector in IndiaDocument25 pagesStudy On HRM Practices Followed in Power Generation Sector in IndiaSujith ParavannoorNo ratings yet

- Adani Power Strategic Analysis.Document22 pagesAdani Power Strategic Analysis.hihimanshu700% (1)

- Report of Working Group On Power: 12th Five Year Plan (2012 - 17) IndiaDocument466 pagesReport of Working Group On Power: 12th Five Year Plan (2012 - 17) IndiaRaghvendra UpadhyaNo ratings yet

- NTPC Internship ReportDocument52 pagesNTPC Internship ReportbarkhavermaNo ratings yet

- Book Summary of Bloom of DesertDocument27 pagesBook Summary of Bloom of DesertSambhranta MishraNo ratings yet

- Project On Industrial Analysis: Energy Sector: BY: Abhishek Kumar Sinha Kumari Priya Shreel Dwivedi Anwesha ChatterjeeDocument12 pagesProject On Industrial Analysis: Energy Sector: BY: Abhishek Kumar Sinha Kumari Priya Shreel Dwivedi Anwesha ChatterjeesibbipriyaNo ratings yet

- Adani 1Document3 pagesAdani 1Puneeta RaniNo ratings yet

- India's Power Sector: Ambitious Goals and Massive Investment NeedsDocument20 pagesIndia's Power Sector: Ambitious Goals and Massive Investment Needsyadavmihir63No ratings yet

- Indian Power SectorDocument38 pagesIndian Power SectorAbhay Singh ChandelNo ratings yet

- Edited 2Document23 pagesEdited 2Mahesh majji100% (1)

- A Study On Diesel Generator Sets in IndiaDocument44 pagesA Study On Diesel Generator Sets in IndiaRoyal ProjectsNo ratings yet

- India's Power Sector Growth and Future PlansDocument6 pagesIndia's Power Sector Growth and Future PlansDivya ParvathaneniNo ratings yet

- Financial Analysis of Adani Power Limited and NHPC LimitedDocument19 pagesFinancial Analysis of Adani Power Limited and NHPC LimitedSandeep MandalNo ratings yet

- WG PowerDocument427 pagesWG PowerDebanjan DasNo ratings yet

- CSR 3Document37 pagesCSR 3Balakrishna ChakaliNo ratings yet

- India's Growing Power Demand and the Rise of NTPCDocument13 pagesIndia's Growing Power Demand and the Rise of NTPCBindal HeenaNo ratings yet

- Financial Analysis NPTCDocument20 pagesFinancial Analysis NPTCNakul SharmaNo ratings yet

- NTPC's CSR and Power GenerationDocument20 pagesNTPC's CSR and Power GenerationMukesh ManwaniNo ratings yet

- Caso de Estudio DukeDocument75 pagesCaso de Estudio DukeFernando MirandaNo ratings yet

- Improving Electric Power Supply Using Distributed Generation For Sustainable Entrepreneurship Development in NigeriaDocument9 pagesImproving Electric Power Supply Using Distributed Generation For Sustainable Entrepreneurship Development in NigeriaInternational Journal of Innovative Science and Research TechnologyNo ratings yet

- Finance Report SecBDocument26 pagesFinance Report SecBnickysweet21No ratings yet

- Indian Power IndustryDocument10 pagesIndian Power IndustryuttamrungtaNo ratings yet

- Energy Handbook IndiaDocument10 pagesEnergy Handbook Indiaashoku_s01No ratings yet

- BCML II EnclosuresDocument46 pagesBCML II Enclosurespradeepika04No ratings yet

- Industry Analysis Power SectorDocument19 pagesIndustry Analysis Power SectorKomali GuthikondaNo ratings yet

- Power and Energy Industry in IndiaDocument16 pagesPower and Energy Industry in IndiaSayan MaitiNo ratings yet

- Dividend Policy and Its Impact On Share PriceDocument12 pagesDividend Policy and Its Impact On Share PriceDestiny Tuition CentreNo ratings yet

- Power Sector Analysis in IndiaDocument8 pagesPower Sector Analysis in IndiaSimranNo ratings yet

- Sapm Psda - Eic AnalysisDocument12 pagesSapm Psda - Eic AnalysisAkash SinghNo ratings yet

- Open-Letter-on-Energy-ReformsDocument6 pagesOpen-Letter-on-Energy-ReformsFaizan AliNo ratings yet

- Stress Management at NTPC 2Document44 pagesStress Management at NTPC 2Aditya Rana100% (1)

- Policy Brief On "Development and Governance of The Energy Sector"Document53 pagesPolicy Brief On "Development and Governance of The Energy Sector"tajreen01No ratings yet

- Chaos in Power Pakistan's Electricity CrisisDocument15 pagesChaos in Power Pakistan's Electricity CrisisUsman AhmadNo ratings yet

- Literature Review On Power Sector in IndiaDocument5 pagesLiterature Review On Power Sector in Indiaafmzfmeeavndqe100% (1)

- Emailing Independent Power Production-Converted - 5Document12 pagesEmailing Independent Power Production-Converted - 5Abdullah AhmadNo ratings yet

- Measures To Be Taken by Government To Improve The Industrial Sector of PakistanDocument8 pagesMeasures To Be Taken by Government To Improve The Industrial Sector of PakistanRaheel RaufNo ratings yet

- Project Report On JSPLDocument26 pagesProject Report On JSPLSunny KeshriNo ratings yet

- Strategic Management: MPBA G508Document6 pagesStrategic Management: MPBA G508Test UserNo ratings yet

- India Power Sector ReportDocument37 pagesIndia Power Sector ReportSahil MatteNo ratings yet

- India's power sector holds huge potentialDocument2 pagesIndia's power sector holds huge potentialsumit.avistarNo ratings yet

- Change Management With Implimentation of ErpDocument34 pagesChange Management With Implimentation of ErpBINAYAK SHANKARNo ratings yet

- Eng Nkea Oil Gas EnergyDocument16 pagesEng Nkea Oil Gas EnergytanboemNo ratings yet

- Financial Statement Analysis of Power CompaniesDocument45 pagesFinancial Statement Analysis of Power CompaniesSuraj ParmarNo ratings yet

- Technical Assistance Report: Project Number: 41125 July 2007Document11 pagesTechnical Assistance Report: Project Number: 41125 July 2007M P ChakravortyNo ratings yet

- Energy Scenario in IndiaDocument13 pagesEnergy Scenario in IndiaTado LehnsherrNo ratings yet

- Health, Safety, and Environment For Power IndustryDocument106 pagesHealth, Safety, and Environment For Power Industrysundaram upadhyayNo ratings yet

- Market Size and Investment in India's Power SectorDocument13 pagesMarket Size and Investment in India's Power SectorajayNo ratings yet

- INDUSTRY PROFILE RajatDocument47 pagesINDUSTRY PROFILE RajatArun SharmaNo ratings yet

- Mozambique Power CrisisDocument34 pagesMozambique Power CrisisYouzhnyNo ratings yet

- FINANCIAL ANALYSISDocument86 pagesFINANCIAL ANALYSISrevannamahadevammaNo ratings yet

- NTPC Organization Structure and FunctionsDocument60 pagesNTPC Organization Structure and FunctionsRavindra Chowdary GudapatiNo ratings yet

- Renewable 0 Energy 0 ReportDocument94 pagesRenewable 0 Energy 0 ReportTara Sinha100% (1)

- Mnre PDFDocument171 pagesMnre PDFPadhu PadmaNo ratings yet

- MNRE Annual Report 2019-20Document192 pagesMNRE Annual Report 2019-204u.nandaNo ratings yet

- Deloitte HCAS Report - Talent Management &Document16 pagesDeloitte HCAS Report - Talent Management &Jagadeesh RamaswamyNo ratings yet

- BBDIT-Conference 22mar2014 PDFDocument34 pagesBBDIT-Conference 22mar2014 PDFK S MEERANo ratings yet

- Knowledge and Power: Lessons from ADB Energy ProjectsFrom EverandKnowledge and Power: Lessons from ADB Energy ProjectsNo ratings yet

- Philippines: Energy Sector Assessment, Strategy, and Road MapFrom EverandPhilippines: Energy Sector Assessment, Strategy, and Road MapNo ratings yet

- Improving Skills for the Electricity Sector in IndonesiaFrom EverandImproving Skills for the Electricity Sector in IndonesiaNo ratings yet

- Wipro's Audit Repo Add IntroDocument33 pagesWipro's Audit Repo Add IntroDeepika KalimuthuNo ratings yet

- Final Projact of Cost ButgetDocument35 pagesFinal Projact of Cost ButgetDeepika KalimuthuNo ratings yet

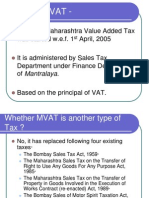

- Maharashtra Value Added Taxact, 2002 (Mvat) : Basic Concepts: Vivek College of CommerceDocument35 pagesMaharashtra Value Added Taxact, 2002 (Mvat) : Basic Concepts: Vivek College of CommerceDeepika KalimuthuNo ratings yet

- Financial 1Document41 pagesFinancial 1Deepika KalimuthuNo ratings yet

- University of Mumbai RM Sem 4Document5 pagesUniversity of Mumbai RM Sem 4Deepika KalimuthuNo ratings yet

- 634357469811641250Document23 pages634357469811641250Deepika KalimuthuNo ratings yet

- FM Ratio ProjectDocument39 pagesFM Ratio ProjectDeepika KalimuthuNo ratings yet

- University of Mumbai RM Sem 4Document5 pagesUniversity of Mumbai RM Sem 4Deepika KalimuthuNo ratings yet

- Indirect Taxes: Matushri Pushpaben Vinubhai Valia College of Commerce (Affiliated To University of Mumbai)Document20 pagesIndirect Taxes: Matushri Pushpaben Vinubhai Valia College of Commerce (Affiliated To University of Mumbai)Deepika KalimuthuNo ratings yet

- Consumer Behaviour: Business PurposeDocument30 pagesConsumer Behaviour: Business PurposeDeepika KalimuthuNo ratings yet

- Projectonshampoo 101107134213 Phpapp01 DeepikaDocument30 pagesProjectonshampoo 101107134213 Phpapp01 DeepikaDeepika KalimuthuNo ratings yet

- Consumer Behaviour Towards Shampoos: Vivek College of CommersDocument37 pagesConsumer Behaviour Towards Shampoos: Vivek College of CommersDeepika KalimuthuNo ratings yet

- Projectonshampoo 101107134213 Phpapp01 DeepikaDocument30 pagesProjectonshampoo 101107134213 Phpapp01 DeepikaDeepika KalimuthuNo ratings yet

- Deepika ShampooDocument8 pagesDeepika ShampooThilaga Senthilmurugan100% (1)

- Salary IncomeDocument8 pagesSalary IncomeAshis karmakarNo ratings yet

- Tax ProDocument34 pagesTax ProDeepika KalimuthuNo ratings yet

- AccDocument35 pagesAccDeepika KalimuthuNo ratings yet

- Business Strategy For ITC LTDDocument32 pagesBusiness Strategy For ITC LTDDeepika KalimuthuNo ratings yet

- Financial Ratio Analysis of SBI and ICICI BankDocument32 pagesFinancial Ratio Analysis of SBI and ICICI BankDeepika KalimuthuNo ratings yet

- 1Document1 page1Deepika KalimuthuNo ratings yet