You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5810)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1092)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (843)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (346)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

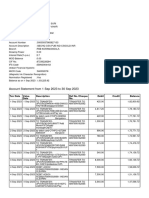

- BRAC Bank Statement 10052023 PDFDocument7 pagesBRAC Bank Statement 10052023 PDFMd Mizanur Rahman100% (1)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- TITAN Whitepaper enDocument8 pagesTITAN Whitepaper enAli ShahNo ratings yet

- CT2-PX-0 - QP-x2-x3Document22 pagesCT2-PX-0 - QP-x2-x3AmitNo ratings yet

- Actuarial Society of India: Subject 108: Finance and Financial ReportingDocument3 pagesActuarial Society of India: Subject 108: Finance and Financial ReportingAmitNo ratings yet

- Key For S108 With Marking ScheduleDocument12 pagesKey For S108 With Marking ScheduleAmitNo ratings yet

- CT2 PXS 07Document72 pagesCT2 PXS 07AmitNo ratings yet

- Actuarial Society of India: Examinations: May 2002Document7 pagesActuarial Society of India: Examinations: May 2002AmitNo ratings yet

- Actuarial Society of India: ExaminationsDocument9 pagesActuarial Society of India: ExaminationsAmitNo ratings yet

- CT1 Sol 0605Document15 pagesCT1 Sol 0605AmitNo ratings yet

- 2011-12-22 RBI Final IRB GuidelinesDocument196 pages2011-12-22 RBI Final IRB GuidelinesAmitNo ratings yet

- Dish TV India Limited: Earnings Release For The Quarter Ended December 31, 2011Document5 pagesDish TV India Limited: Earnings Release For The Quarter Ended December 31, 2011AmitNo ratings yet

- Government of India Ministry of Statistics and Programme Implementation Central Statistics OfficeDocument9 pagesGovernment of India Ministry of Statistics and Programme Implementation Central Statistics OfficeAmitNo ratings yet

- Corporate Governance in AfricaDocument23 pagesCorporate Governance in AfricaIrwan Setiawan FauziNo ratings yet

- Italian Companies Go GlobalDocument13 pagesItalian Companies Go GlobalAsdsaNo ratings yet

- M18-101 - As IndAS by CA Rajesh MakkarDocument451 pagesM18-101 - As IndAS by CA Rajesh MakkarAANo ratings yet

- Various Types of Loan Provided by Banks in Nepalese MarketDocument1 pageVarious Types of Loan Provided by Banks in Nepalese MarketNarendra KumarNo ratings yet

- FPC Pinehill Presentation 2020-06-29Document26 pagesFPC Pinehill Presentation 2020-06-29Anto BrilliantoNo ratings yet

- Ujp Fs Jun23Document72 pagesUjp Fs Jun23Mochamad AdriantoNo ratings yet

- Credit Appraisal - Financial Analysis - PPTX Day2Document52 pagesCredit Appraisal - Financial Analysis - PPTX Day2sabetaliNo ratings yet

- Velasquez v. Solidbank CorporationDocument1 pageVelasquez v. Solidbank CorporationTeff Quibod67% (3)

- Chapter 1Document3 pagesChapter 1zyl manuelNo ratings yet

- Hto 4B 22 7065327 02 000 - ScheduleDocument7 pagesHto 4B 22 7065327 02 000 - ScheduleNithin GuptaNo ratings yet

- Consolidations - Subsequent To The Date of AcquisitionDocument42 pagesConsolidations - Subsequent To The Date of AcquisitionAla'aEQahwajiʚîɞNo ratings yet

- Ias & IfrsDocument7 pagesIas & IfrsAsiful IslamNo ratings yet

- Pmba 6313 Week 2 HomeworkDocument1 pagePmba 6313 Week 2 HomeworkLucyNo ratings yet

- LeverageDocument6 pagesLeverageutkarsh.khera98No ratings yet

- Maintain Average Monthly Balance Of: Maintain Average Quarterly Balance ofDocument3 pagesMaintain Average Monthly Balance Of: Maintain Average Quarterly Balance ofyvonneNo ratings yet

- Georgia Residential Mgt. AgreementDocument4 pagesGeorgia Residential Mgt. AgreementalperNo ratings yet

- Chap. 7-9 Outline ForDocument7 pagesChap. 7-9 Outline ForMJNo ratings yet

- Financial Statement Analysis - Concept Questions and Solutions - Chapter 2Document20 pagesFinancial Statement Analysis - Concept Questions and Solutions - Chapter 2stefy934100% (2)

- Workshop 3 - MathsDocument9 pagesWorkshop 3 - MathsMABEL XIMENA GONZALEZ PEREZNo ratings yet

- Teacher Induction Program - Module 2 V1.0Document58 pagesTeacher Induction Program - Module 2 V1.0GLENNY VIZCARRANo ratings yet

- Manufacturing AccountsDocument16 pagesManufacturing AccountsKen IrokNo ratings yet

- AegonDocument2 pagesAegonIndrasen DewanganNo ratings yet

- UATQ1 ResultDocument3 pagesUATQ1 ResultramsesiNo ratings yet

- Chapter 15-Reasons For Busines Failure: Quote: 'Document26 pagesChapter 15-Reasons For Busines Failure: Quote: 'sk001100% (2)

- Z Rbup Alp 9 D Ahmc 4 PDocument5 pagesZ Rbup Alp 9 D Ahmc 4 Ppranay.suriNo ratings yet

- Realigning Estimate On Stronger Than Expected Mass Market: Bloomberry Resorts CorporationDocument8 pagesRealigning Estimate On Stronger Than Expected Mass Market: Bloomberry Resorts CorporationJajahinaNo ratings yet