You might also like

- Profitability MaximizationDocument11 pagesProfitability MaximizationSanket KarNo ratings yet

- 3.3.6 Multinational CorporationsDocument32 pages3.3.6 Multinational CorporationsAli AhmedNo ratings yet

- BUS804 International Business Strategy: Lecturer - Dr. Robert JackDocument43 pagesBUS804 International Business Strategy: Lecturer - Dr. Robert JackJuha PropertiesNo ratings yet

- Ch01 - International Financial ManagementDocument47 pagesCh01 - International Financial Managementalsatusatusatu100% (1)

- Crowdfunding Report CCAF Africa 2017Document76 pagesCrowdfunding Report CCAF Africa 2017CrowdfundInsiderNo ratings yet

- StratMan-Outside USADocument23 pagesStratMan-Outside USAoceansNo ratings yet

- K&S Supply Chain LocationDocument8 pagesK&S Supply Chain LocationRohanNo ratings yet

- IBM's Global Back-Up: International TreasurerDocument1 pageIBM's Global Back-Up: International TreasureritreasurerNo ratings yet

- Doing Business in China: Opportunities and ChallengesDocument15 pagesDoing Business in China: Opportunities and ChallengesSanjana BhattNo ratings yet

- Mozal FinancingDocument18 pagesMozal FinancingSourabh Dhawan100% (1)

- Case AnalysisDocument16 pagesCase AnalysisVeda DhageNo ratings yet

- Smartlessons MakingPPPsWorkForThePoorDocument4 pagesSmartlessons MakingPPPsWorkForThePoorasdf789456123No ratings yet

- Keep Calm & Drive Safe: Zipcar Case AnalysisDocument15 pagesKeep Calm & Drive Safe: Zipcar Case AnalysisAmit Pathak100% (1)

- Business Environment 5 (MNCS)Document29 pagesBusiness Environment 5 (MNCS)NABIHA AZAD NOORNo ratings yet

- EFVCDocument11 pagesEFVCValdemar Miguel SilvaNo ratings yet

- Ceoguidetogloballeadership BK DdiDocument23 pagesCeoguidetogloballeadership BK DdiNasir AliNo ratings yet

- Polaris CapitalDocument33 pagesPolaris CapitalBurj CapitalNo ratings yet

- Great Startup Ideas Eds 111Document20 pagesGreat Startup Ideas Eds 111okpara chukwukaNo ratings yet

- Venture Capital & Entrepreneurship in The U.A.E.Document11 pagesVenture Capital & Entrepreneurship in The U.A.E.Jaideep DhanoaNo ratings yet

- How Main Street Businesses Use Financial Services: Key Survey FindingsDocument15 pagesHow Main Street Businesses Use Financial Services: Key Survey Findingsapi-249785899No ratings yet

- Zipcar Case Analysis Reveals Growth Potential and Optimization OpportunitiesDocument1 pageZipcar Case Analysis Reveals Growth Potential and Optimization Opportunitiesbmjk800% (1)

- Greenhaven Road Value - Halogen Software FINALDocument24 pagesGreenhaven Road Value - Halogen Software FINALCanadianValue100% (1)

- Week 2 UIDocument28 pagesWeek 2 UISlendy CamargoNo ratings yet

- Getting Work with the Federal Government: A Guide to Figuring out the Procurement PuzzleFrom EverandGetting Work with the Federal Government: A Guide to Figuring out the Procurement PuzzleNo ratings yet

- Jan 17 - ZipCarDocument7 pagesJan 17 - ZipCarellenzhuNo ratings yet

- Market Development in EthiopiaDocument24 pagesMarket Development in EthiopiaGeremew MetadelNo ratings yet

- International Financial Management: 7 EditionDocument47 pagesInternational Financial Management: 7 Editionbiradardnyaneshwar90No ratings yet

- Capital Budgeting Cash Flow PrinciplesDocument37 pagesCapital Budgeting Cash Flow PrinciplesJoshNo ratings yet

- PA4 EnglishDocument8 pagesPA4 EnglishJUDITH MARGOT LLERENA TAPIANo ratings yet

- Regulation A+ and Other Alternatives to a Traditional IPO: Financing Your Growth Business Following the JOBS ActFrom EverandRegulation A+ and Other Alternatives to a Traditional IPO: Financing Your Growth Business Following the JOBS ActNo ratings yet

- Chapter - GlobalizationDocument18 pagesChapter - Globalizationvarsha bansodeNo ratings yet

- KPMG Private Equity Survey 2013Document64 pagesKPMG Private Equity Survey 2013bobbyr01norNo ratings yet

- Stream Theory: An Employee-Centered Hybrid Management System for Achieving a Cultural Shift through Prioritizing Problems, Illustrating Solutions, and Enabling EngagementFrom EverandStream Theory: An Employee-Centered Hybrid Management System for Achieving a Cultural Shift through Prioritizing Problems, Illustrating Solutions, and Enabling EngagementNo ratings yet

- 5 Insights - Capital AllocationDocument8 pages5 Insights - Capital AllocationPatrickBrown1No ratings yet

- Zipcar: Redefining Its Business ModelDocument11 pagesZipcar: Redefining Its Business Modelshmuup10% (1)

- Chapter 4 (Contemporary Models)Document22 pagesChapter 4 (Contemporary Models)Moktar Mohamed omerNo ratings yet

- International Finance: IAME - International Academy of Management & Entrepreneurship Shashank BPDocument46 pagesInternational Finance: IAME - International Academy of Management & Entrepreneurship Shashank BPValentineJoaoNo ratings yet

- STM CH12 Mba.183969.1584520478.5985 PDFDocument39 pagesSTM CH12 Mba.183969.1584520478.5985 PDFNattanonSirirungruangNo ratings yet

- Wells FargoDocument30 pagesWells Fargosyidaramli100% (3)

- 2020 Main MemoDocument7 pages2020 Main MemoPusheletso MashiloNo ratings yet

- Zambia Investment Climate Assessment 2005 PDFDocument68 pagesZambia Investment Climate Assessment 2005 PDFjunk08100% (1)

- Strategy Importance in 21st CenturyDocument5 pagesStrategy Importance in 21st CenturyChavie NoynayNo ratings yet

- Entre CutdownDocument16 pagesEntre Cutdownapi-276863157No ratings yet

- One Stop Shops: Improving Better Business Environment and CompetitivenessDocument17 pagesOne Stop Shops: Improving Better Business Environment and CompetitivenessAnonymous hwNoPqNo ratings yet

- Research Paper On Revenue CollectionDocument8 pagesResearch Paper On Revenue Collectionfyrqkxfq100% (1)

- Greenfield MFIs in Sub-Saharan AfricaDocument44 pagesGreenfield MFIs in Sub-Saharan AfricaCGAP PublicationsNo ratings yet

- Informal Cross-Border Trade in East African RegionDocument20 pagesInformal Cross-Border Trade in East African RegionGemmeNo ratings yet

- Setting Up Accounts Receivable Policies For Business in CanadaDocument24 pagesSetting Up Accounts Receivable Policies For Business in CanadaasdefenceNo ratings yet

- Case-Study 01 - Airtel AfricaDocument42 pagesCase-Study 01 - Airtel AfricaBiniNo ratings yet

- South Africa Case StudyDocument3 pagesSouth Africa Case StudyWalaa AlzoubiNo ratings yet

- Capital Budgeting Process GuideDocument74 pagesCapital Budgeting Process GuideMitul KathuriaNo ratings yet

- 11.30 Michel Folliet, International Finance CorporationDocument11 pages11.30 Michel Folliet, International Finance CorporationMohd AliNo ratings yet

- Informal Sector: A: Comprehensive StudyDocument17 pagesInformal Sector: A: Comprehensive Studysorti nortiNo ratings yet

- Management of Multinational Companies - Problems & Prospects of Mncs in An International EnvironmentDocument23 pagesManagement of Multinational Companies - Problems & Prospects of Mncs in An International EnvironmentMuskaan ChhabraNo ratings yet

- International Business: Prof: Viju NavareDocument17 pagesInternational Business: Prof: Viju NavareNimisha BurdeNo ratings yet

- DRC-Iraq MSME Support-Print PDFDocument4 pagesDRC-Iraq MSME Support-Print PDFsimonlevineNo ratings yet

- Past and PerspectiveDocument19 pagesPast and PerspectiveManivvannan AmbigapathyNo ratings yet

- 2020 Main MemoDocument6 pages2020 Main MemoPusheletso MashiloNo ratings yet

- KPMG DissertationDocument5 pagesKPMG Dissertationcreasimovel1987100% (1)

- Disruptive Technologies V Sep 2021Document33 pagesDisruptive Technologies V Sep 2021dekom bpr-tsmsNo ratings yet

- Client Briefing Mozambique Rovuma Basin Decree New 6028706Document10 pagesClient Briefing Mozambique Rovuma Basin Decree New 6028706beyu777No ratings yet

- Guide TrinidadTobagoDocument104 pagesGuide TrinidadTobagobeyu777No ratings yet

- Africa Oil and Gas GuideDocument205 pagesAfrica Oil and Gas Guidekalite123No ratings yet

- Africa Oil and Gas GuideDocument577 pagesAfrica Oil and Gas Guidebeyu777No ratings yet

- 2014 Africa CSOSI FINAL PDFDocument241 pages2014 Africa CSOSI FINAL PDFbeyu777No ratings yet

- Canadian Firms Survey of Issues in AfricaDocument16 pagesCanadian Firms Survey of Issues in Africabeyu777No ratings yet

- Tutorial - Convert Avi To VCD, Mpeg To VCD, WMV To VCDDocument4 pagesTutorial - Convert Avi To VCD, Mpeg To VCD, WMV To VCDbeyu777No ratings yet

- EIA NGL Workshop Kristen HolmquistDocument14 pagesEIA NGL Workshop Kristen Holmquistbeyu777No ratings yet

- Process Safety Leading and Lagging Metrics - CCPS - 2011Document44 pagesProcess Safety Leading and Lagging Metrics - CCPS - 2011Haribo1962No ratings yet

- Infra Red EffectDocument5 pagesInfra Red Effectbeyu777No ratings yet

- Energy Independence Study ProspectusDocument9 pagesEnergy Independence Study Prospectusbeyu777No ratings yet

- Overcoming Our LimitationDocument96 pagesOvercoming Our Limitationbeyu777No ratings yet

- Bleeding During Pregnancy Causes & How To Prevent Bleeding During PregnancyDocument6 pagesBleeding During Pregnancy Causes & How To Prevent Bleeding During Pregnancybeyu777No ratings yet

- NewGold BrochureDocument6 pagesNewGold Brochurebeyu777No ratings yet

- DauwalterDocument28 pagesDauwalterbeyu777No ratings yet

- 30-Dec-2020-Memorandum To Sebi and Justice BN AgrawalDocument17 pages30-Dec-2020-Memorandum To Sebi and Justice BN AgrawalMoneylife FoundationNo ratings yet

- Balance Sheet: Titan Industries LimitedDocument4 pagesBalance Sheet: Titan Industries LimitedShalini ShreyaNo ratings yet

- CH 18 Audit of The Acquisition and Payment Cycle PDFDocument13 pagesCH 18 Audit of The Acquisition and Payment Cycle PDFFred The Fish100% (1)

- Global IME BankDocument29 pagesGlobal IME BankSujan Bajracharya100% (2)

- Master in Economics of Banking and Finance ProgramDocument2 pagesMaster in Economics of Banking and Finance ProgramtranglomangoNo ratings yet

- 2013-14 Wabash College Academic BulletinDocument294 pages2013-14 Wabash College Academic BulletinYoung-ho ParkNo ratings yet

- Consistency Analysis of Mixed Mutual Fund Performance and Equity Mutual Funds Performance Between 2003-2014 Using Sharpe, Treynor, and Jensen MethodsDocument12 pagesConsistency Analysis of Mixed Mutual Fund Performance and Equity Mutual Funds Performance Between 2003-2014 Using Sharpe, Treynor, and Jensen MethodsNuniek KartikariniNo ratings yet

- Verma Committee ReportDocument170 pagesVerma Committee Reportaeroa1No ratings yet

- Financial & Management Accounting PapersDocument10 pagesFinancial & Management Accounting PapersKeyur Patel0% (1)

- Economic History: The IndiaDocument231 pagesEconomic History: The IndiaShubhang Shankar SrivastavaNo ratings yet

- Tanggal Uraian Transaksi Nominal Transaksi SaldoDocument2 pagesTanggal Uraian Transaksi Nominal Transaksi SaldoRazor RRNo ratings yet

- International Financial Institutions and Human Rights - Implications For Public Health PDFDocument17 pagesInternational Financial Institutions and Human Rights - Implications For Public Health PDFFERNANDA LAGE ALVES DANTASNo ratings yet

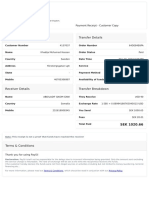

- Sender Details Transfer Details: Payment Receipt - CustomerDocument1 pageSender Details Transfer Details: Payment Receipt - CustomerAbshira Abdi AliNo ratings yet

- Cash Flows Chap-13Document52 pagesCash Flows Chap-13nina0301100% (1)

- Chapter 12 AnswersDocument3 pagesChapter 12 AnswersMarisa Vetter100% (1)

- Bank Loan ContractDocument6 pagesBank Loan ContractSiddharth BaxiNo ratings yet

- Accounting Mcqs 3Document6 pagesAccounting Mcqs 3Mohd AyazNo ratings yet

- Gels Omino 2016Document22 pagesGels Omino 2016Karen HerasNo ratings yet

- Go v. Metrobank G.R. No. 168842 (2010) DoctrineDocument2 pagesGo v. Metrobank G.R. No. 168842 (2010) DoctrineRey Emmanuel BurgosNo ratings yet

- Reimbursement Expense Receipt Reimbursement Expense ReceiptDocument1 pageReimbursement Expense Receipt Reimbursement Expense ReceiptMark Calpon Lechido100% (1)

- Accounting recap for sole proprietor and partnership final accountsDocument10 pagesAccounting recap for sole proprietor and partnership final accountsShivamNo ratings yet

- Budget: Events Project OperationDocument3 pagesBudget: Events Project OperationAngelie SanchezNo ratings yet

- Consolidated Financial Statement (Part 1)Document32 pagesConsolidated Financial Statement (Part 1)Ruby Amor DoligosaNo ratings yet

- Cash and Liquidity Management - Topic 3Document47 pagesCash and Liquidity Management - Topic 3kodeNo ratings yet

- A201 Ch6 Fall 2013Document44 pagesA201 Ch6 Fall 2013Set LuNo ratings yet

- Recruitment SampleDocument3 pagesRecruitment SampleNkanyezi MagwazaNo ratings yet

- Siemens Audit Report PDFDocument43 pagesSiemens Audit Report PDFShameel IrshadNo ratings yet

- IT Income From Other Sources Pt-2Document7 pagesIT Income From Other Sources Pt-2syedfareed596No ratings yet

- A Study On Investors Investment Perception Towards Cooperative Banks With Special Reference To Edappal PanchayathDocument63 pagesA Study On Investors Investment Perception Towards Cooperative Banks With Special Reference To Edappal Panchayathdreem Hunter100% (1)

- Takeover - Credit ReportDocument8 pagesTakeover - Credit ReportShantanuMogalNo ratings yet