You might also like

- Ias 24 Related Party DisclosuresDocument3 pagesIas 24 Related Party DisclosurescaarunjiNo ratings yet

- IAS 24-Related Party DisclosuresDocument27 pagesIAS 24-Related Party DisclosuresRiazboni100% (1)

- PAS 34 Interim Financial Reporting: Learning ObjectivesDocument5 pagesPAS 34 Interim Financial Reporting: Learning ObjectivesFhrince Carl CalaquianNo ratings yet

- Cfas ReviewerDocument6 pagesCfas ReviewerMaycacayan, Charlene M.No ratings yet

- IAS 10 Events After The Reporting Period PDFDocument1 pageIAS 10 Events After The Reporting Period PDFSajib PolashNo ratings yet

- Ifrs at A Glance: IAS 39 Financial InstrumentsDocument8 pagesIfrs at A Glance: IAS 39 Financial InstrumentsvivekchokshiNo ratings yet

- Module 6 - Operating SegmentsDocument3 pagesModule 6 - Operating SegmentsChristine Joyce BascoNo ratings yet

- Fund, Which Is Separate From The Reporting Entity For The Purpose ofDocument7 pagesFund, Which Is Separate From The Reporting Entity For The Purpose ofNaddieNo ratings yet

- Pas 40 Investment PropertyDocument4 pagesPas 40 Investment PropertykristineNo ratings yet

- PAS 24 Related Party Disclosures: Learning ObjectivesDocument4 pagesPAS 24 Related Party Disclosures: Learning ObjectivesFhrince Carl Calaquian100% (1)

- Non Current Asset Held For SaleDocument27 pagesNon Current Asset Held For SaleAbdulmajed Unda MimbantasNo ratings yet

- Topic 1: Statement of Financial PositionDocument10 pagesTopic 1: Statement of Financial Positionemman neri100% (1)

- Pfrs 16 LeasesDocument4 pagesPfrs 16 LeasesR.A.No ratings yet

- LG 03A Overview of Auditing and The Audit Process 2018 PDFDocument4 pagesLG 03A Overview of Auditing and The Audit Process 2018 PDFNash JuaqueraNo ratings yet

- Full Pfrs Vs Pfrs For Smes PDFDocument21 pagesFull Pfrs Vs Pfrs For Smes PDFPaula Merriles100% (2)

- Chapter 3Document5 pagesChapter 3Julie Neay AfableNo ratings yet

- Lecture 3 Provisions - Contingent Liabilities and Contingent AssetsDocument23 pagesLecture 3 Provisions - Contingent Liabilities and Contingent AssetsBrenden KapoNo ratings yet

- AFAR 12 Foreign Currency TransactionsDocument6 pagesAFAR 12 Foreign Currency TransactionsLouie RobitshekNo ratings yet

- Events After The Reporting Period Final 6 KiloDocument13 pagesEvents After The Reporting Period Final 6 Kilonati100% (1)

- Module I. Business Combination Date of Acquisition NADocument13 pagesModule I. Business Combination Date of Acquisition NAmax pNo ratings yet

- Pas 32Document34 pagesPas 32Iris SarigumbaNo ratings yet

- Chapter 19Document6 pagesChapter 19Joan Angelica ManaloNo ratings yet

- To Manage Financial Risk: Purpose of A DerivativeDocument4 pagesTo Manage Financial Risk: Purpose of A DerivativeVillaruz Shereen MaeNo ratings yet

- Chapter 17 Test Bank Corporate Liquidations, Reorganizations, and Debt Restructurings For Financially Distressed CorporationsDocument16 pagesChapter 17 Test Bank Corporate Liquidations, Reorganizations, and Debt Restructurings For Financially Distressed CorporationsBusiness MatterNo ratings yet

- Finacc 3 Question Set BDocument9 pagesFinacc 3 Question Set BEza Joy ClaveriasNo ratings yet

- Ifrs 5: Noncurrent Assets Held: For Sale and Discontinued OperationsDocument14 pagesIfrs 5: Noncurrent Assets Held: For Sale and Discontinued OperationsShah Kamal100% (1)

- REVIEWERDocument10 pagesREVIEWERRhyna Vergara SumaoyNo ratings yet

- Gross Income Deductions - Lecture Handout PDFDocument4 pagesGross Income Deductions - Lecture Handout PDFKarl RendonNo ratings yet

- Accntg4 Non-Current Assets Held For Sale and Discontinued Operations NewDocument32 pagesAccntg4 Non-Current Assets Held For Sale and Discontinued Operations NewALYSSA MAE ABAAGNo ratings yet

- Accounting Standard-18: Related Party DisclosureDocument26 pagesAccounting Standard-18: Related Party DisclosurelulughoshNo ratings yet

- Audit of Inv Property, NCA HFS and Disc OpDocument32 pagesAudit of Inv Property, NCA HFS and Disc OpPaula BitorNo ratings yet

- ISA 260 Revised 1Document24 pagesISA 260 Revised 1dzenita5beciragic5kaNo ratings yet

- Theories Chapter 1Document16 pagesTheories Chapter 1Farhana GuiandalNo ratings yet

- Strategic Management Ch14Document15 pagesStrategic Management Ch14Pé IuNo ratings yet

- BUSCOMDocument5 pagesBUSCOMGeoreyGNo ratings yet

- TX10 Other Percentage TaxDocument16 pagesTX10 Other Percentage TaxAnna AldaveNo ratings yet

- Chapter 1Document7 pagesChapter 1Hoàng Thanh NguyễnNo ratings yet

- IFRS 11 SummaryDocument4 pagesIFRS 11 SummaryJoshua Capa Fronda100% (1)

- MAS 09 - Quantitative TechniquesDocument6 pagesMAS 09 - Quantitative TechniquesClint Abenoja0% (1)

- Montenegro Tabular Schedule of Standards and Interpretations 2019Document6 pagesMontenegro Tabular Schedule of Standards and Interpretations 2019Kathleen LeynesNo ratings yet

- 12e TB Chap 13Document9 pages12e TB Chap 13poopyguy12345678No ratings yet

- Module 6 FINP1 Financial ManagementDocument28 pagesModule 6 FINP1 Financial ManagementChristine Jane LumocsoNo ratings yet

- IFRS For SMEsDocument10 pagesIFRS For SMEsJhemmilyn RiveraNo ratings yet

- Accounting For Government GrantsDocument4 pagesAccounting For Government GrantsSandia EspejoNo ratings yet

- MODULE 5 - Investment Property: 3.1.1 Definition & NatureDocument12 pagesMODULE 5 - Investment Property: 3.1.1 Definition & NatureCj BarrettoNo ratings yet

- Cuartero - Unit 3 - Accounting Changes and Error CorrectionDocument10 pagesCuartero - Unit 3 - Accounting Changes and Error CorrectionAim RubiaNo ratings yet

- FAR and IAs Quali Exams With AnswersDocument17 pagesFAR and IAs Quali Exams With AnswersReghis AtienzaNo ratings yet

- M00340020220114128M0034-PT11-12-The Expenditure CycleDocument25 pagesM00340020220114128M0034-PT11-12-The Expenditure CycleriznaldoNo ratings yet

- Law2 CH 1 Law2 Business Laws and RegulationsDocument8 pagesLaw2 CH 1 Law2 Business Laws and Regulationsnelma mae ruzNo ratings yet

- Conceptual Framework For Financial ReportingDocument54 pagesConceptual Framework For Financial ReportingAlthea Claire Yhapon100% (1)

- IAS-37 Provisions, Contingent Liabilities and Contingent AssetsDocument29 pagesIAS-37 Provisions, Contingent Liabilities and Contingent AssetsAbdul SamiNo ratings yet

- Cpa Review School of The Philippines: ManilaDocument24 pagesCpa Review School of The Philippines: ManilaRalph Joshua JavierNo ratings yet

- Intermediate Accounting 2 THEORIESDocument68 pagesIntermediate Accounting 2 THEORIESLedelyn MaullonNo ratings yet

- Accounting ChangesDocument5 pagesAccounting Changeskty yjmNo ratings yet

- Forecasting One MarkDocument45 pagesForecasting One MarkJoshua Daniel EganNo ratings yet

- Chapter 5 Statement of Changes in EquityDocument6 pagesChapter 5 Statement of Changes in EquitylcNo ratings yet

- Quiz 2 Ncahs/ Discontinued Operation: FeedbackDocument67 pagesQuiz 2 Ncahs/ Discontinued Operation: FeedbackAngela Miles DizonNo ratings yet

- Exercise No.4 Bus. Co.Document56 pagesExercise No.4 Bus. Co.Jeane Mae BooNo ratings yet

- Chapter 07 PAS 24 RELATED PARTY DISCLOSURESDocument4 pagesChapter 07 PAS 24 RELATED PARTY DISCLOSURESJoelyn Grace MontajesNo ratings yet

- Ias 24 Related PartyDocument4 pagesIas 24 Related Partyhassaanbinqudoos411No ratings yet

- Consolidated FsDocument6 pagesConsolidated Fssimply PrettyNo ratings yet

- Separate FsDocument5 pagesSeparate Fssimply PrettyNo ratings yet

- LeaseDocument20 pagesLeasesimply Pretty0% (1)

- Interest in JVDocument6 pagesInterest in JVsimply PrettyNo ratings yet

- Key Definitions (IAS 8.5) Accounting PoliciesDocument6 pagesKey Definitions (IAS 8.5) Accounting Policiessimply PrettyNo ratings yet

- Discontinued Operation: Summary of IAS 35Document3 pagesDiscontinued Operation: Summary of IAS 35simply PrettyNo ratings yet

- Borrowing CostDocument3 pagesBorrowing Costsimply PrettyNo ratings yet

- Chapter 01 - Business CombinationsDocument17 pagesChapter 01 - Business CombinationsTina LundstromNo ratings yet

- AgricultureDocument5 pagesAgriculturesimply PrettyNo ratings yet

- Employee BenefitsDocument8 pagesEmployee Benefitssimply PrettyNo ratings yet

- Pool Canvas: Calculated FormulaDocument12 pagesPool Canvas: Calculated Formulasimply PrettyNo ratings yet

- 2012 Auditing and Attestation HandoutDocument21 pages2012 Auditing and Attestation Handoutsimply Pretty100% (1)

- Financial Supplement: January - MarchDocument9 pagesFinancial Supplement: January - MarchSanjeev ThadaniNo ratings yet

- The Steel War - Mittal Vs ArcelorDocument25 pagesThe Steel War - Mittal Vs ArcelorAsiri PrasadNo ratings yet

- Karkits CorporationDocument6 pagesKarkits CorporationKimNo ratings yet

- Assignment Chapter Issue of Shares Class 12thDocument5 pagesAssignment Chapter Issue of Shares Class 12thPriya TandonNo ratings yet

- Guidance Note On CSR Expenditure (My Notes)Document2 pagesGuidance Note On CSR Expenditure (My Notes)maulesh bhattNo ratings yet

- Bank Reporting Example NABILDocument54 pagesBank Reporting Example NABILSujit KoiralaNo ratings yet

- Summary Pointer Chapter 2 Advanced AccountingDocument6 pagesSummary Pointer Chapter 2 Advanced Accountingahmed arfanNo ratings yet

- Enclosure 1. Teacher-Made Learner's Home Task (Week 9) : The Nature of A Service BusinessDocument7 pagesEnclosure 1. Teacher-Made Learner's Home Task (Week 9) : The Nature of A Service BusinessKim FloresNo ratings yet

- Corporation Law Outline (Jacinto)Document16 pagesCorporation Law Outline (Jacinto)anon-856821100% (2)

- Unit 6Document19 pagesUnit 6Eco FacileNo ratings yet

- ACCA P2INT Notes J15 PDFDocument256 pagesACCA P2INT Notes J15 PDFopentuitionID100% (1)

- Consolidation of Wholly Owned Subsidiaries Acquired at More Than Book ValueDocument11 pagesConsolidation of Wholly Owned Subsidiaries Acquired at More Than Book ValueJeklin LewaneyNo ratings yet

- Landmark Facility Solutions - SunilDocument4 pagesLandmark Facility Solutions - SunilPawan Mishra67% (3)

- Marketing of Financial Services: A Project On Morgan StanleyDocument5 pagesMarketing of Financial Services: A Project On Morgan Stanleysanket sunilNo ratings yet

- Chapter Two Principles & Basis of Accounting For Government & NFP EntitiesDocument10 pagesChapter Two Principles & Basis of Accounting For Government & NFP Entitiesmeron fitsum100% (1)

- Ambit Strategy Thematic TenBaggers5 05jan2016 PDFDocument28 pagesAmbit Strategy Thematic TenBaggers5 05jan2016 PDFVikas TiwariNo ratings yet

- Strategic Management - Midterm Quiz 1Document6 pagesStrategic Management - Midterm Quiz 1Uy SamuelNo ratings yet

- Finance Module 01 - Week 1Document14 pagesFinance Module 01 - Week 1Christian ZebuaNo ratings yet

- Internship Project Education LoanDocument57 pagesInternship Project Education LoanYuvraaj singh BaghelNo ratings yet

- October 2020: Canada Core Pick ListDocument3 pagesOctober 2020: Canada Core Pick ListblacksmithMGNo ratings yet

- Aau ModelDocument34 pagesAau ModelTayech TayuNo ratings yet

- ASPIRATIONDocument9 pagesASPIRATIONClinton ForgyNo ratings yet

- TAX Ch03Document13 pagesTAX Ch03GabriellaNo ratings yet

- Faculty of Law: Jamia Millia IslamiaDocument21 pagesFaculty of Law: Jamia Millia IslamiaFaisal HassanNo ratings yet

- HO 1 - Commercial Law - Corporation Law PDFDocument35 pagesHO 1 - Commercial Law - Corporation Law PDFBerchman MelendezNo ratings yet

- Far Weeks1 7Document245 pagesFar Weeks1 7Mitch Minglana100% (1)

- Team Evolvers - CFA RCDocument10 pagesTeam Evolvers - CFA RCSUMAN SUMANNo ratings yet

- Wealth-Lab Developer 6.9 Performance: Strategy: Channel Breakout VT Dataset/Symbol: AALDocument1 pageWealth-Lab Developer 6.9 Performance: Strategy: Channel Breakout VT Dataset/Symbol: AALHamahid pourNo ratings yet

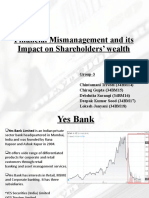

- Group3 - CFEV - Project Presentation - Fin-MismanagementDocument11 pagesGroup3 - CFEV - Project Presentation - Fin-MismanagementDeepak SoodNo ratings yet

- 2Q 2019 PEHA Phapros+TbkDocument91 pages2Q 2019 PEHA Phapros+TbkHiji DuaNo ratings yet