You might also like

- Management Accounting Formula Summary GarrisonDocument5 pagesManagement Accounting Formula Summary GarrisonAyman AlamNo ratings yet

- Cost Accounting SolutionDocument736 pagesCost Accounting Solutionniggy.fan85% (34)

- Cost and Management Accounting Notes and FormulaDocument84 pagesCost and Management Accounting Notes and FormulaKanchan Chaturvedi74% (47)

- Cost AccountingDocument6 pagesCost AccountingCarl Angelo100% (5)

- 29 Problems and Solution CostingDocument70 pages29 Problems and Solution CostingNavin Joshi70% (10)

- Cost Accounting QuestionsDocument52 pagesCost Accounting QuestionsEych Mendoza67% (9)

- Standard Costing FormulaDocument2 pagesStandard Costing FormulaAce Erguiza50% (4)

- Eoq ProblemsDocument5 pagesEoq ProblemsrajeshwariNo ratings yet

- ACCRETION and EVAPORATION LOSSDocument17 pagesACCRETION and EVAPORATION LOSSVon Andrei MedinaNo ratings yet

- Cost Accounting Imporatant FormulasDocument3 pagesCost Accounting Imporatant FormulassanthimbaNo ratings yet

- Study Notes On Cost AccountingDocument69 pagesStudy Notes On Cost AccountingPriyankaJainNo ratings yet

- Cost AccountingDocument28 pagesCost AccountingImthe OneNo ratings yet

- Cost Accounting Theory NotesDocument41 pagesCost Accounting Theory NotesShrividhya Venkata Prasath83% (6)

- Cost Accounting Practice TestDocument27 pagesCost Accounting Practice Testaiswift100% (1)

- 2a. Job Order Costing CRDocument17 pages2a. Job Order Costing CRAnaly Omandac PelayoNo ratings yet

- Cost Sheet Exercise 1Document3 pagesCost Sheet Exercise 1Phaniraj LenkalapallyNo ratings yet

- 35 Resource 11Document16 pages35 Resource 11Anonymous bf1cFDuepPNo ratings yet

- Procurement and Inventory Management Partial Assignment On Inventory Management Uqba Imtiaz 20171-22152Document7 pagesProcurement and Inventory Management Partial Assignment On Inventory Management Uqba Imtiaz 20171-22152Aqba ImtiazNo ratings yet

- Accounting For Production Losses Under Job Order CostingDocument10 pagesAccounting For Production Losses Under Job Order CostingRia BryleNo ratings yet

- AFAR H01 Cost AccountingDocument7 pagesAFAR H01 Cost AccountingPau SantosNo ratings yet

- Elements of Cost SheetDocument41 pagesElements of Cost Sheetapi-2701408994% (18)

- Chapter 1 2 Cost Accounting and Control by de Leon 2019Document10 pagesChapter 1 2 Cost Accounting and Control by de Leon 2019Accounting Files50% (2)

- Cost AccountingDocument208 pagesCost AccountingSankalp Navghare75% (8)

- Cost Sheet ProblemsDocument22 pagesCost Sheet ProblemsAvinash Tanawade100% (4)

- Job Order Costing ExamDocument18 pagesJob Order Costing ExamRjan LG100% (1)

- Absorption CostingDocument5 pagesAbsorption CostingBurhan Ahmed CheemaNo ratings yet

- Absorption Marginal CostingDocument36 pagesAbsorption Marginal CostingsamiNo ratings yet

- Topic 1: Cost Concepts and Cost Behavior COGS Merchandising CompanyDocument6 pagesTopic 1: Cost Concepts and Cost Behavior COGS Merchandising CompanyKezNo ratings yet

- Marginal Costs (Extra Reading)Document15 pagesMarginal Costs (Extra Reading)Gabriel BelmonteNo ratings yet

- Garrison/Libby/Webb Managerial Accounting 11 Edition Formula SummaryDocument4 pagesGarrison/Libby/Webb Managerial Accounting 11 Edition Formula Summaryمنیر ساداتNo ratings yet

- Absorption CostingDocument34 pagesAbsorption Costinggaurav pandeyNo ratings yet

- Activity Based CostingDocument28 pagesActivity Based CostingApril TorresNo ratings yet

- Absorption and Marginal CostingDocument19 pagesAbsorption and Marginal CostingsadikzeenatNo ratings yet

- Chapter 10 - Marginal and Absorption CostingDocument8 pagesChapter 10 - Marginal and Absorption CostingkundiarshdeepNo ratings yet

- Cost AccountingDocument6 pagesCost AccountingMj PacunayenNo ratings yet

- Analisis Varians Dan Standar Products CostsDocument4 pagesAnalisis Varians Dan Standar Products CostsAhad KamisNo ratings yet

- Absorption and Variable CostingDocument12 pagesAbsorption and Variable CostingMatrika ThapaNo ratings yet

- Chapter 7Document4 pagesChapter 7Mixx MineNo ratings yet

- Overhead and Other Variances PDFDocument26 pagesOverhead and Other Variances PDFAnuruddha RajasuriyaNo ratings yet

- Formula SheetDocument1 pageFormula SheetTaha SauoodNo ratings yet

- Chapter 10 - Accounting (Financial Statements) - 1-1Document8 pagesChapter 10 - Accounting (Financial Statements) - 1-1Sonali AnandNo ratings yet

- Absorption MarginalDocument17 pagesAbsorption MarginalSHIVANSH BANSALNo ratings yet

- Absorption and Variable Costing ReviewDocument13 pagesAbsorption and Variable Costing ReviewRodelLabor100% (1)

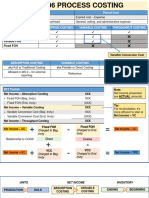

- MS 06-06 Process CostingDocument6 pagesMS 06-06 Process CostingxernathanNo ratings yet

- Financial Tools Week 2 Block BDocument15 pagesFinancial Tools Week 2 Block BBelen González BouzaNo ratings yet

- Chapter 1 - Absorption and Marginal CostingDocument31 pagesChapter 1 - Absorption and Marginal CostingTrinhNo ratings yet

- Chapter 4 Income Measurement and ReportingDocument13 pagesChapter 4 Income Measurement and ReportingOmisha KhatiwadaNo ratings yet

- Cost ManagementDocument23 pagesCost ManagementEswara ReddyNo ratings yet

- SUMMARY - Working Capital ManagementDocument4 pagesSUMMARY - Working Capital ManagementAccounting MaterialsNo ratings yet

- P 15 5. Standard Costing ChartDocument1 pageP 15 5. Standard Costing ChartHari MNo ratings yet

- Formula:: High Low Method (High - Low) Break-Even PointDocument24 pagesFormula:: High Low Method (High - Low) Break-Even PointRedgie Mark UrsalNo ratings yet

- Module 2 Practice ProblemsDocument21 pagesModule 2 Practice ProblemsLiza Mae MirandaNo ratings yet

- Strat Cost Handout 02 CVP Analysis Updated 0212 - CompressDocument17 pagesStrat Cost Handout 02 CVP Analysis Updated 0212 - CompressAerwyna AfarinNo ratings yet

- Marginal & Absorption Costing ST Academy With SolutionDocument14 pagesMarginal & Absorption Costing ST Academy With SolutionFaisal KhanNo ratings yet

- Prelim - Cost FormulaDocument3 pagesPrelim - Cost FormulaStanley AquinoNo ratings yet

- Prelim - Cost FormulaDocument3 pagesPrelim - Cost FormulaStanley AquinoNo ratings yet

- Product CostingDocument34 pagesProduct CostingrhearomefranciscoNo ratings yet

- Five-Page Summary of Key Concepts:: Cost ClassificationsDocument16 pagesFive-Page Summary of Key Concepts:: Cost ClassificationsDar FayeNo ratings yet

- Assignment: VarianceDocument3 pagesAssignment: VarianceFarhan MehmoodNo ratings yet

- In Class Quiz: November 7th Chapter: 8 & 9Document6 pagesIn Class Quiz: November 7th Chapter: 8 & 9SabrinaNo ratings yet

- Feasibility StudyDocument46 pagesFeasibility StudyAcsecnarf AbarueNo ratings yet

- Profit and Loss Projection 1yr March 2018Document1 pageProfit and Loss Projection 1yr March 2018Aqsa SajjadNo ratings yet

- Answer Prime Cost Raw Material Purchased + Opening Stock of Raw Materials - Closing Stock of RawDocument2 pagesAnswer Prime Cost Raw Material Purchased + Opening Stock of Raw Materials - Closing Stock of RawVarun ChaitanyaNo ratings yet

- Chapter 5Document4 pagesChapter 5Ngô Hoàng Bích KhaNo ratings yet

- Cost Accounting - Different Kinds of CostsDocument3 pagesCost Accounting - Different Kinds of CostsPam Alem Caval PlarisanNo ratings yet

- Ac102 ch7Document22 pagesAc102 ch7Mohammed OsmanNo ratings yet

- Insurance Claims - FTDocument6 pagesInsurance Claims - FTblack jackNo ratings yet

- Accounting Ratios - Class NotesDocument8 pagesAccounting Ratios - Class NotesAbdullahSaqibNo ratings yet

- CH 09Document52 pagesCH 09NghiaBuiQuangNo ratings yet

- Applied Auditing: T E AC H E R S M A N U A LDocument118 pagesApplied Auditing: T E AC H E R S M A N U A LIce Voltaire Buban GuiangNo ratings yet

- Cost Accounting - Case-Daniel DobbinsDocument1 pageCost Accounting - Case-Daniel DobbinsRatin Mathur100% (4)

- Meeting 9 - 10 - Student VersionDocument72 pagesMeeting 9 - 10 - Student VersionKevin ChandraNo ratings yet

- Benson Tolomia Dagoy Banaybanay Cadiente VistaDocument25 pagesBenson Tolomia Dagoy Banaybanay Cadiente VistaClaire VensueloNo ratings yet

- Managerial AccountingDocument21 pagesManagerial AccountingRam KnowlesNo ratings yet

- Chapter - 1: A Case Study On "Fortune Cotton & Agro Industries"Document50 pagesChapter - 1: A Case Study On "Fortune Cotton & Agro Industries"Tippesh KokanurNo ratings yet

- Overheads - IBADocument6 pagesOverheads - IBAZehra HussainNo ratings yet

- Bài Kiểm Tra MA2Document5 pagesBài Kiểm Tra MA2ngablack3110No ratings yet

- 462 1Document10 pages462 1M Noaman AkbarNo ratings yet

- Inventories HandoutsDocument7 pagesInventories HandoutsAera GarcesNo ratings yet

- 01 Homework - Urbino Bsa - 4aDocument8 pages01 Homework - Urbino Bsa - 4aVeralou UrbinoNo ratings yet

- Consolidated FAR UC QUESTIONDocument15 pagesConsolidated FAR UC QUESTIONNathalie GetinoNo ratings yet

- Homework Solution - Week 10 - Relevant Costing - GarrisonDocument6 pagesHomework Solution - Week 10 - Relevant Costing - GarrisonGloria WongNo ratings yet

- Standard Costing Hand-OutDocument1 pageStandard Costing Hand-OutJoshua RomasantaNo ratings yet

- Inventory Book (Intermediate Accounting)Document77 pagesInventory Book (Intermediate Accounting)Joelo De VeraNo ratings yet

- Quiz No. 4 - InventoriesDocument8 pagesQuiz No. 4 - Inventoriesremalyn rigorNo ratings yet

- CH 2 - Job Costing SystemDocument19 pagesCH 2 - Job Costing SystemDeeb. DeebNo ratings yet

- Asset - Inventory - For Posting PDFDocument8 pagesAsset - Inventory - For Posting PDFNhicoleChoiNo ratings yet

- A Cost Center Is A Unit of Activity Within The Factory To Which Costs MayDocument3 pagesA Cost Center Is A Unit of Activity Within The Factory To Which Costs MayqasmsNo ratings yet

- Marginal and Absorption CostingDocument17 pagesMarginal and Absorption CostingHAHAHANo ratings yet

- Using Cost Flow Methods ConsistentlyDocument9 pagesUsing Cost Flow Methods Consistentlymagdy kamelNo ratings yet