You might also like

- Internship Report of Leather CoordinatorsDocument19 pagesInternship Report of Leather Coordinatorswaleed ahmadNo ratings yet

- HUMANITIESDocument3 pagesHUMANITIESJann Recto100% (7)

- ASICS Case - 311Document7 pagesASICS Case - 311Jake Marzoff100% (1)

- Internship Report of Leather CoordinatorsDocument22 pagesInternship Report of Leather CoordinatorsAmeer hamzaNo ratings yet

- LIBRO RIBERA Ingles BaixaDocument108 pagesLIBRO RIBERA Ingles Baixazaryab khan100% (2)

- Leather Industry Report 1transparentDocument18 pagesLeather Industry Report 1transparentvikramullalNo ratings yet

- Cost and Account Management: Leather Industry in IndiaDocument9 pagesCost and Account Management: Leather Industry in IndiaSourabhNo ratings yet

- Analysis of Leather Industry in PakistanDocument19 pagesAnalysis of Leather Industry in PakistanHasan AbidiNo ratings yet

- Brintons Project ReportDocument24 pagesBrintons Project ReportpgundechaNo ratings yet

- Leather Products Export To GermanyDocument35 pagesLeather Products Export To GermanyAbhijeet Kulshreshtha100% (3)

- Leather Project ReportDocument15 pagesLeather Project Reporthrn_world100% (1)

- Nike Environmental Analysis 1216536910789066 8Document26 pagesNike Environmental Analysis 1216536910789066 8Re YaNo ratings yet

- Leather Goods FinalDocument15 pagesLeather Goods FinalImran1978No ratings yet

- Industry Analysis Report Indian Leather IndustryDocument31 pagesIndustry Analysis Report Indian Leather Industrybalaji bysani100% (1)

- Assignment LeatherDocument6 pagesAssignment LeatherAhmed MastanNo ratings yet

- LeatherDocument15 pagesLeatherSingh Nitin80% (5)

- Summer Internship ReportDocument69 pagesSummer Internship ReportShobhitShankhalaNo ratings yet

- Footwear IndustryDocument22 pagesFootwear Industrymunibhaskar0% (1)

- Leather Products Export To Germany (EXIM)Document29 pagesLeather Products Export To Germany (EXIM)Thomas KevinNo ratings yet

- Indian Leather IndustryDocument19 pagesIndian Leather IndustryMahesh MahiNo ratings yet

- Leather Exporting PDFDocument20 pagesLeather Exporting PDFAyman BrohiNo ratings yet

- Leather Industry PresentationDocument18 pagesLeather Industry PresentationSara Pervez100% (1)

- Leather and FootwearDocument10 pagesLeather and FootwearArun SudarshanNo ratings yet

- A Quick Review of Emerging Leather Sector of BangladeshDocument10 pagesA Quick Review of Emerging Leather Sector of BangladeshAtabur RahmanNo ratings yet

- A Report On Leather and Leather Goods in PDFDocument13 pagesA Report On Leather and Leather Goods in PDFMd Tanjid Ahmed ZahidNo ratings yet

- Overview of Pakistani Leather Industry PDFDocument7 pagesOverview of Pakistani Leather Industry PDFMuhammad Shahid RazaNo ratings yet

- Value Chain AnalysisDocument76 pagesValue Chain AnalysisA B M Rafiqul Hasan Khan67% (3)

- Leather GarmentsDocument7 pagesLeather GarmentssirdlugorekiNo ratings yet

- Export-Import Procedure and Documentation: Topic: Exporting Leather Products To Germany Hussain Chunawala Roll No. 07Document29 pagesExport-Import Procedure and Documentation: Topic: Exporting Leather Products To Germany Hussain Chunawala Roll No. 07Thomas KevinNo ratings yet

- Deloitte Report Leather and FootwearDocument84 pagesDeloitte Report Leather and Footwearpgpm710No ratings yet

- Project PPT LeatherDocument12 pagesProject PPT Leathernitinsachdeva21No ratings yet

- Report On Analysis of Leather Industry in National and International ContextDocument42 pagesReport On Analysis of Leather Industry in National and International ContextJahir HasanNo ratings yet

- Environmental Friendly Preservation of Hides and Skin: Physical Preservation Chemical PreservationDocument11 pagesEnvironmental Friendly Preservation of Hides and Skin: Physical Preservation Chemical PreservationVivek SahuNo ratings yet

- Global Project Full and FinalDocument16 pagesGlobal Project Full and FinalFaizan Ahmad AfzalNo ratings yet

- Low Polution Leather TanningDocument8 pagesLow Polution Leather TanningFarhad HossainNo ratings yet

- Leather Goods Manufacturing Unit (Wallets) PDFDocument18 pagesLeather Goods Manufacturing Unit (Wallets) PDFSyed Zeeshan AliNo ratings yet

- Indian Footwear IndustryDocument29 pagesIndian Footwear IndustryRita ChatterjiNo ratings yet

- Studies On The Production of Football Leather From Cow HideDocument40 pagesStudies On The Production of Football Leather From Cow Hiderubelbclet100% (1)

- Bangladeshi Leather IndustryDocument8 pagesBangladeshi Leather IndustrySyed Nayem100% (1)

- Leather Business PlanDocument7 pagesLeather Business PlanAmit Kumar0% (1)

- Leather Industry and The Export Market of India..Sanjay YadavDocument50 pagesLeather Industry and The Export Market of India..Sanjay Yadavsanjayyadav007No ratings yet

- A. Introduction To Leather Goods Designing - EBDPD - LGT IIIDocument57 pagesA. Introduction To Leather Goods Designing - EBDPD - LGT IIIIndranil SahaNo ratings yet

- LeatherDocument2 pagesLeatherAlim MaheraliNo ratings yet

- Export & ImportDocument29 pagesExport & ImportKhan ZiaNo ratings yet

- Quality Control-Notes Presentation - Chongeri Azaria Mikas Leather Dit MwanzaDocument81 pagesQuality Control-Notes Presentation - Chongeri Azaria Mikas Leather Dit MwanzaAzaria MikasNo ratings yet

- Pollution of Leather IndustryDocument70 pagesPollution of Leather IndustryBalaji GajendranNo ratings yet

- 4 Day Practical Leather TechnologyDocument4 pages4 Day Practical Leather Technologyemmanuel byoNo ratings yet

- Final+Report +++Raymond+Chhindwara1 1Document94 pagesFinal+Report +++Raymond+Chhindwara1 1Neeraj Kumar40% (5)

- List of The Top 10 Leather Manufacturers in BangladeshDocument4 pagesList of The Top 10 Leather Manufacturers in BangladeshNasim HasanNo ratings yet

- Case Study Leather Industrial Parks PDocument144 pagesCase Study Leather Industrial Parks PGayatri G.No ratings yet

- Leather TanningDocument8 pagesLeather TanningSahar SohailNo ratings yet

- Raymond Akhilesh Final ReportDocument59 pagesRaymond Akhilesh Final ReportAkhilesh50% (4)

- Environmental Biology: Course TitleDocument20 pagesEnvironmental Biology: Course Titlehalamobeen100% (1)

- From Leather Waste To Functional Leather ISBN 978-84-934261-9-4Document61 pagesFrom Leather Waste To Functional Leather ISBN 978-84-934261-9-4Thanaa AsiNo ratings yet

- Business - Plan - of - Leather - Products - GlemKore International (Opc) PVT LTD, SBIDocument21 pagesBusiness - Plan - of - Leather - Products - GlemKore International (Opc) PVT LTD, SBIUjjwal SenNo ratings yet

- Industrial Profile-Leather IndustryDocument15 pagesIndustrial Profile-Leather IndustryPratistha BhargavaNo ratings yet

- Hides and Skins and the Manufacture of Leather - A Layman's View of the IndustryFrom EverandHides and Skins and the Manufacture of Leather - A Layman's View of the IndustryNo ratings yet

- Indian Leather Industry AnalysisDocument10 pagesIndian Leather Industry Analysisrajanikanthreddy_mNo ratings yet

- Indian Leather Industry OverviewDocument30 pagesIndian Leather Industry OverviewPrithvi DhanukaNo ratings yet

- Leather IndustryDocument7 pagesLeather IndustrySumit ChandraNo ratings yet

- Leather IndustryDocument23 pagesLeather IndustryChhaya SinghNo ratings yet

- BATA INDIA LIMITED Final OneDocument65 pagesBATA INDIA LIMITED Final OneGaurav MudgalNo ratings yet

- Marketing Strategies For Domestic Sale of Laether Products.: Project ReportDocument27 pagesMarketing Strategies For Domestic Sale of Laether Products.: Project ReportAdwait VermaNo ratings yet

- Structure of MisDocument5 pagesStructure of MisMohammed BilalNo ratings yet

- Project On Work Environment in Hero HondaDocument82 pagesProject On Work Environment in Hero HondaMohammed BilalNo ratings yet

- Recommendation LetterDocument1 pageRecommendation LetterMohammed BilalNo ratings yet

- 302EL2Document15 pages302EL2Mohammed BilalNo ratings yet

- ASUS AuthorizedDocument1 pageASUS AuthorizedMohammed BilalNo ratings yet

- International Business: Subject Code: Credit: L+P: 4+0 Teaching Hours: 60 HrsDocument1 pageInternational Business: Subject Code: Credit: L+P: 4+0 Teaching Hours: 60 HrsMohammed BilalNo ratings yet

- AnalysisDocument1 pageAnalysisMohammed BilalNo ratings yet

- Analysis 2Document1 pageAnalysis 2Mohammed BilalNo ratings yet

- Analysis IDocument1 pageAnalysis IMohammed BilalNo ratings yet

- Staff Recommended BY Name of The Applicant Appl. NO. MAR KS RemarksDocument22 pagesStaff Recommended BY Name of The Applicant Appl. NO. MAR KS RemarksMohammed BilalNo ratings yet

- Literature ReviewDocument65 pagesLiterature ReviewMohammed Bilal0% (1)

- Continuous Internal Assessment, Apr.14 The New College (Autonomous), Chennai 600 014Document3 pagesContinuous Internal Assessment, Apr.14 The New College (Autonomous), Chennai 600 014Mohammed BilalNo ratings yet

- Continuous Internal Assessment, Apr.14 The New College (Autonomous), Chennai 600 014Document2 pagesContinuous Internal Assessment, Apr.14 The New College (Autonomous), Chennai 600 014Mohammed BilalNo ratings yet

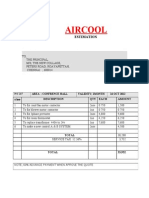

- Aircool: EstimationDocument4 pagesAircool: EstimationMohammed BilalNo ratings yet

- BBA OverallDocument2 pagesBBA OverallMohammed BilalNo ratings yet

- Tamilnadu Institute of Labour StudiesDocument3 pagesTamilnadu Institute of Labour StudiesMohammed Bilal100% (1)

- Economic ServicesDocument1 pageEconomic ServicesMohammed BilalNo ratings yet

- Tying Shoe Laces: Suggested StrategiesDocument3 pagesTying Shoe Laces: Suggested StrategiesJacob BurnsNo ratings yet

- RsscanDocument34 pagesRsscanapi-268534894No ratings yet

- Leather and Leather Goods PDFDocument56 pagesLeather and Leather Goods PDFAshish DixitNo ratings yet

- The Beginners Guide To EleganceDocument54 pagesThe Beginners Guide To EleganceCornelia SlabbertNo ratings yet

- DIY Leather Baby Shoes With Free PatternDocument10 pagesDIY Leather Baby Shoes With Free PatternhairbynatNo ratings yet

- Thor Defense 2011Document151 pagesThor Defense 2011Mario LopezNo ratings yet

- Temu Explore The Latest Clothing, Beauty, HomeDocument1 pageTemu Explore The Latest Clothing, Beauty, HomeEl Mamadou Baïlo SowNo ratings yet

- Skateboarding'S Best Kept SecretDocument23 pagesSkateboarding'S Best Kept SecretRodrigo DinizNo ratings yet

- Cosh Construction Occupational Safety & Health Course: Personal Protective Equipment (PPE)Document57 pagesCosh Construction Occupational Safety & Health Course: Personal Protective Equipment (PPE)Ralph John ColomaNo ratings yet

- Store KeepingDocument8 pagesStore KeepingRavikant PandeyNo ratings yet

- ShoesDocument53 pagesShoesMajibul RehmanNo ratings yet

- Kolhapuri ChappalsDocument30 pagesKolhapuri ChappalsPriyanka TrivediNo ratings yet

- Human Movement Science: Eric C. Honert, Karl E. Zelik TDocument12 pagesHuman Movement Science: Eric C. Honert, Karl E. Zelik Tpignus engenhariaNo ratings yet

- Arif Harbott Cass EMBA Sep10 Operations Management PDFDocument12 pagesArif Harbott Cass EMBA Sep10 Operations Management PDFwaja abdNo ratings yet

- Strength Running PR GuideDocument46 pagesStrength Running PR GuideAnonymous 7BQxlt8c100% (3)

- Quality Questions and Answers ISC Class 11 and Class 12Document9 pagesQuality Questions and Answers ISC Class 11 and Class 12Ayan Arif100% (1)

- 10 Tips To Eliminate Smell Shoes Easily and QuicklyDocument3 pages10 Tips To Eliminate Smell Shoes Easily and QuicklyRiniNo ratings yet

- Barrel Race BarefootDocument6 pagesBarrel Race Barefootapi-199934300No ratings yet

- ERSA Pro Stringer Magazine 1 - 2019 Prostringer 1-2019 WebDocument32 pagesERSA Pro Stringer Magazine 1 - 2019 Prostringer 1-2019 WebMark Maslowski100% (1)

- Work Shoes "Kickflip Low": Red BlueDocument1 pageWork Shoes "Kickflip Low": Red BlueIzhoneRdrNo ratings yet

- BindingTechManual 1213 FRDocument52 pagesBindingTechManual 1213 FRPascal DownNo ratings yet

- Manual Patinete ElectricoDocument13 pagesManual Patinete ElectricoRubén Aparicio LlanderasNo ratings yet

- RC-01 Shoe Repair Machine Manual, Shoe Finisher Machine InstructionsDocument3 pagesRC-01 Shoe Repair Machine Manual, Shoe Finisher Machine InstructionsRobin ChouNo ratings yet

- Down Garrapata Road by Anne EstevisDocument129 pagesDown Garrapata Road by Anne EstevisArte Público Press50% (2)

- Brochure Quarvif Eng LowDocument32 pagesBrochure Quarvif Eng Lownovisad199506No ratings yet

- 07 Foot ProtectionDocument18 pages07 Foot ProtectionJoseph BP100% (1)

- Do You Like To Sew?: Jordan Baby T-Strap ShoesDocument11 pagesDo You Like To Sew?: Jordan Baby T-Strap ShoesMaria Lúcia PereiraNo ratings yet