You might also like

- CashappmethoDocument2 pagesCashappmethod86% (21)

- Verify Your PayPal Account Without A Credit CardDocument1 pageVerify Your PayPal Account Without A Credit Cardncasperue590k0% (1)

- Master Card - JsonDocument1 pageMaster Card - JsonSina SardarNo ratings yet

- Global Payments 2020 Transformation and ConvergenceDocument49 pagesGlobal Payments 2020 Transformation and ConvergenceGregory MartirosovNo ratings yet

- The Future of PaymentsDocument40 pagesThe Future of Paymentsanon_903741391No ratings yet

- Forrester Wave For Digital Banking Q3 2017Document17 pagesForrester Wave For Digital Banking Q3 2017Ahmed NasrNo ratings yet

- Merger Management - 1Document26 pagesMerger Management - 1boka987No ratings yet

- Innovation in Retail BankingDocument102 pagesInnovation in Retail BankingAlina DamaschinNo ratings yet

- MCK On Semiconductors - Issue 3 - 2013Document68 pagesMCK On Semiconductors - Issue 3 - 2013boka987No ratings yet

- Consumer Lending in IndiaDocument25 pagesConsumer Lending in IndiaGautamNo ratings yet

- Deconstructing Digital Only Banking Model A Proposed Policy Roadmap For India FINALDocument44 pagesDeconstructing Digital Only Banking Model A Proposed Policy Roadmap For India FINALVenke JayakanthNo ratings yet

- Mobile Payment Tutor Institution Date A Systematic Literature Review On Mobile PaymentDocument14 pagesMobile Payment Tutor Institution Date A Systematic Literature Review On Mobile PaymentShikz Alexine100% (1)

- Prime It Bank Statement - July 2019Document4 pagesPrime It Bank Statement - July 2019api-306226330No ratings yet

- BCG Digital Lending Report Tcm21 197622Document48 pagesBCG Digital Lending Report Tcm21 197622Krishna Chaitanya KothapalliNo ratings yet

- OpTransactionHistory23 03 2020 PDFDocument5 pagesOpTransactionHistory23 03 2020 PDFRINKU KATHURIYANo ratings yet

- Fintech: Digital PaymentsDocument15 pagesFintech: Digital PaymentsAnand ArgNo ratings yet

- Top 10 Trends 2019 in PaymentsDocument26 pagesTop 10 Trends 2019 in PaymentsscottyuNo ratings yet

- Carol Coye Benson - Scott J Loftesness - Payments Systems in The U.S. - A Guide For The Payments Professional-Glenbrook Partners (2013)Document149 pagesCarol Coye Benson - Scott J Loftesness - Payments Systems in The U.S. - A Guide For The Payments Professional-Glenbrook Partners (2013)Chico TonhosoNo ratings yet

- Lending and Leasing Top 10 Trends 2017 WebDocument28 pagesLending and Leasing Top 10 Trends 2017 WebGherasim BriceagNo ratings yet

- Banking - As - A - Service - An - Objective - Analysis - Research Paper - SG Fintech PDFDocument40 pagesBanking - As - A - Service - An - Objective - Analysis - Research Paper - SG Fintech PDFAshwin BS100% (2)

- Backbase - Top Banking Transformation Case StudiesDocument79 pagesBackbase - Top Banking Transformation Case StudiesPhương Anh Lê100% (1)

- The PAYTECH Book: The Payment Technology Handbook for Investors, Entrepreneurs, and FinTech VisionariesFrom EverandThe PAYTECH Book: The Payment Technology Handbook for Investors, Entrepreneurs, and FinTech VisionariesNo ratings yet

- McKinsey Global Payments Report 2019Document33 pagesMcKinsey Global Payments Report 2019Rajiv RaiNo ratings yet

- q1 2023 Quarterly Fintech InsightsDocument127 pagesq1 2023 Quarterly Fintech InsightsMuluken AlemuNo ratings yet

- Open Banking and BaaSDocument30 pagesOpen Banking and BaaSJagadeesh JNo ratings yet

- Building The Future Telco: Simplify - Automate - InnovateDocument69 pagesBuilding The Future Telco: Simplify - Automate - Innovateboka987100% (2)

- Banking of The Future - Embracing TechnologiesDocument44 pagesBanking of The Future - Embracing TechnologiesNeilFaver100% (1)

- Loan Origination System - Final Note - July 26 2022Document22 pagesLoan Origination System - Final Note - July 26 2022Ahsan Bin Asim100% (1)

- E Commerce PDFDocument254 pagesE Commerce PDFAbhiNo ratings yet

- Loan Management Technology Trends EguideDocument11 pagesLoan Management Technology Trends EguideAlexandra CiarnauNo ratings yet

- Messari Report Asia Crypto LandscapeDocument99 pagesMessari Report Asia Crypto LandscapeDicky IrwansyahNo ratings yet

- Banking2025 WhitepaperDocument49 pagesBanking2025 WhitepaperLuka AjvarNo ratings yet

- Streamline Unlimited Account: Closing Balance $3,265.34 CR Enquiries 13 2221Document4 pagesStreamline Unlimited Account: Closing Balance $3,265.34 CR Enquiries 13 2221jo220171No ratings yet

- Possible Designs of CBDCDocument3 pagesPossible Designs of CBDCSachin ChauhanNo ratings yet

- Payments Industry - SLIDE DECK 05.12.2017Document361 pagesPayments Industry - SLIDE DECK 05.12.2017Nat Banyatpiyaphod100% (2)

- Disrupting The $8T Payment Card Business:: The Outlook On Buy Now, Pay Later'Document34 pagesDisrupting The $8T Payment Card Business:: The Outlook On Buy Now, Pay Later'Tawanda Ngowe0% (1)

- Capgemini - World Payments Report 2013Document60 pagesCapgemini - World Payments Report 2013Carlo Di Domenico100% (1)

- Aite - Commercial Loan Origination Scoping The VendorsDocument71 pagesAite - Commercial Loan Origination Scoping The VendorsAsim HussainNo ratings yet

- Open Banking: What You Need To Know: Fintech FuturesDocument8 pagesOpen Banking: What You Need To Know: Fintech Futuresdarma bonarNo ratings yet

- Future of Southeast Asia Digital Financial ServicesDocument52 pagesFuture of Southeast Asia Digital Financial ServicesMaria HanyNo ratings yet

- Open BankingDocument8 pagesOpen BankingAadithyan T GNo ratings yet

- Microsoft - Digital Banking Playbook 2021Document46 pagesMicrosoft - Digital Banking Playbook 2021LinhNo ratings yet

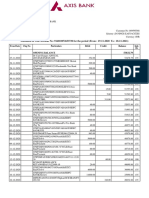

- Statement of Axis Account No:916010072653730 For The Period (From: 19-11-2020 To: 18-11-2021)Document7 pagesStatement of Axis Account No:916010072653730 For The Period (From: 19-11-2020 To: 18-11-2021)asphalt 9 legendsNo ratings yet

- The WEALTHTECH Book: The FinTech Handbook for Investors, Entrepreneurs and Finance VisionariesFrom EverandThe WEALTHTECH Book: The FinTech Handbook for Investors, Entrepreneurs and Finance VisionariesNo ratings yet

- FT Partners FinTech September 2020Document111 pagesFT Partners FinTech September 2020Sergey PostnovNo ratings yet

- Demystifying Digital Lending PDFDocument44 pagesDemystifying Digital Lending PDFHitesh DhaddhaNo ratings yet

- In Tech We Trust: A Report From The Economist Intelligence UnitDocument34 pagesIn Tech We Trust: A Report From The Economist Intelligence UnitAbhishekNo ratings yet

- Innovation in Payments Opportunities and Challenges For EMDEsDocument55 pagesInnovation in Payments Opportunities and Challenges For EMDEsluisNo ratings yet

- Accelerate Cash Management DigitizationDocument24 pagesAccelerate Cash Management DigitizationKV SinglaNo ratings yet

- Fintech Business ModelsDocument8 pagesFintech Business ModelsSarthak0% (1)

- Ifw Process GimDocument24 pagesIfw Process Gimmyownhminbox485No ratings yet

- Digital PaymentsDocument36 pagesDigital PaymentsHarsh VoraNo ratings yet

- Digital WalletDocument19 pagesDigital WalletJoselin ReañoNo ratings yet

- The Rise of BaaS (Banking As A Service) WhitepaperDocument7 pagesThe Rise of BaaS (Banking As A Service) WhitepaperBeltan TönükNo ratings yet

- The Future of Digital Banking PDFDocument27 pagesThe Future of Digital Banking PDFRahmat SyarifNo ratings yet

- Chapter 2 Merchant Acquiring The Rise of Merchant ServicesDocument6 pagesChapter 2 Merchant Acquiring The Rise of Merchant ServicesTech qpaymentzNo ratings yet

- PaymentRoadmap 2021 PDFDocument60 pagesPaymentRoadmap 2021 PDFviolet suNo ratings yet

- Small Business Lending in The Digital AgeDocument27 pagesSmall Business Lending in The Digital AgeCrowdfundInsiderNo ratings yet

- Opportunity For AI ML in BFSI IndustryDocument8 pagesOpportunity For AI ML in BFSI IndustryShekhar SoniNo ratings yet

- Accenture Payment Services Merchant AcquiringDocument4 pagesAccenture Payment Services Merchant AcquiringNature GraceNo ratings yet

- Finacle Core Banking BrochureDocument32 pagesFinacle Core Banking Brochurechirag randhirNo ratings yet

- PDFDocument2 pagesPDFLIMNo ratings yet

- Frictionless Cross-Border Payments Alternatives To Correspondent Banking Volante PDFDocument17 pagesFrictionless Cross-Border Payments Alternatives To Correspondent Banking Volante PDFBen ChampionNo ratings yet

- Digital Banking Playbook Final 1Document21 pagesDigital Banking Playbook Final 1hiteshgoel100% (2)

- The Global Open Banking Report 2020 Beyond Open Banking Into The Open Finance and Open Data EconomyDocument134 pagesThe Global Open Banking Report 2020 Beyond Open Banking Into The Open Finance and Open Data EconomylrNo ratings yet

- Open Banking + Real-Time Payments: A Match Made in Heaven For EuropeDocument16 pagesOpen Banking + Real-Time Payments: A Match Made in Heaven For Europetmuzaffar1No ratings yet

- API Strategy For Open Banking v2Document120 pagesAPI Strategy For Open Banking v2BalsasaNo ratings yet

- Report & Analysis About The Market of Payment Gateway Industry in Indonesia and A Strategic Plan On How To Survive The Market.Document15 pagesReport & Analysis About The Market of Payment Gateway Industry in Indonesia and A Strategic Plan On How To Survive The Market.Ario Wibisono100% (1)

- Market Segmentation in The Construction Industry - Designing Buildings WikiDocument6 pagesMarket Segmentation in The Construction Industry - Designing Buildings Wikiboka987No ratings yet

- Fin Wealth Epamv5 090516Document33 pagesFin Wealth Epamv5 090516Ankur PandeyNo ratings yet

- Fintech Collection Report 2021 - TransUnionDocument22 pagesFintech Collection Report 2021 - TransUnionArnelit PhilipNo ratings yet

- How Open Banking Can Support SME FinanceDocument13 pagesHow Open Banking Can Support SME FinanceADBI EventsNo ratings yet

- Cloud Computing Challenges - 2020Document18 pagesCloud Computing Challenges - 2020boka987No ratings yet

- What's It Like Working in Corporate Strategy?: Intj1359 CS Rank: Senior Chimp - 21Document10 pagesWhat's It Like Working in Corporate Strategy?: Intj1359 CS Rank: Senior Chimp - 21boka987No ratings yet

- Network NotesDocument16 pagesNetwork Notesboka987No ratings yet

- How Elon Musk Learns Faster and Better Than Everyone ElseDocument9 pagesHow Elon Musk Learns Faster and Better Than Everyone Elseboka987No ratings yet

- Additive Manufacturing - MIT Technology ReviewDocument6 pagesAdditive Manufacturing - MIT Technology Reviewboka987No ratings yet

- Marketing Metrics PDFDocument9 pagesMarketing Metrics PDFboka987No ratings yet

- BE ITSyllabusDocument83 pagesBE ITSyllabusboka987No ratings yet

- Business Model PatternsDocument20 pagesBusiness Model Patternsboka987100% (1)

- LucerneDocument1 pageLucernerahul venkateshwaranNo ratings yet

- SBI Site Upload-Service Charges-2017 June 2017 (REVISED)Document1 pageSBI Site Upload-Service Charges-2017 June 2017 (REVISED)NDTVNo ratings yet

- 2022-11-28PDF 221128 104454Document2 pages2022-11-28PDF 221128 104454Andreea ChiriţăNo ratings yet

- Islamic Banking Operations-2019Document20 pagesIslamic Banking Operations-2019Sharifah Faizah As SeggafNo ratings yet

- Fly by Night Alphagraphics InvoiceDocument1 pageFly by Night Alphagraphics InvoiceVaibu MohanNo ratings yet

- Nomad 2022 August Monthly StatementsDocument4 pagesNomad 2022 August Monthly StatementsCarlos HM PiresNo ratings yet

- New Han Bin ResumeDocument1 pageNew Han Bin Resumeapi-262821198No ratings yet

- Shershtacart ShoppingDocument13 pagesShershtacart ShoppingMaruti LavateNo ratings yet

- A Project Report On: "Block Chain and Artificial Intelligence Banking Industry-A Conceptual Perspective"Document58 pagesA Project Report On: "Block Chain and Artificial Intelligence Banking Industry-A Conceptual Perspective"MITESH PANCHALNo ratings yet

- Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDocument50 pagesDate Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing Balanceavnish sharmaNo ratings yet

- Account Details and Transaction History: Ecosave Sa-IDocument48 pagesAccount Details and Transaction History: Ecosave Sa-IDayana MhdNo ratings yet

- UK Finance UK Payment Markets Report 2019 SUMMARYDocument8 pagesUK Finance UK Payment Markets Report 2019 SUMMARYRohitNo ratings yet

- 2018 CPM-done-withmock PDFDocument38 pages2018 CPM-done-withmock PDFLee KimNo ratings yet

- Bill Statement: Previous Charges Amount (RM) Current Charges Amount (RM)Document6 pagesBill Statement: Previous Charges Amount (RM) Current Charges Amount (RM)Nurl AinaNo ratings yet

- Banking & Economy PDF - September 2019 by AffairsCloudDocument77 pagesBanking & Economy PDF - September 2019 by AffairsCloudtoanthoni123No ratings yet

- Wa0015. 1Document15 pagesWa0015. 1austine odhiamboNo ratings yet

- IDFC First Bank: MBG771 - Strategy Formulation Course 1 - Strategy Formulation Assignment 2Document11 pagesIDFC First Bank: MBG771 - Strategy Formulation Course 1 - Strategy Formulation Assignment 2Sandesh Sunil BoraNo ratings yet

- Bitcoin Pres - CREOGNDocument24 pagesBitcoin Pres - CREOGNBridget McGoldrickNo ratings yet

- Hetzner 2019-11-02 R0010328753Document1 pageHetzner 2019-11-02 R0010328753dimaNo ratings yet