You might also like

- CFP Exam Calculation Workbook: 400+ Calculations to Prepare for the CFP Exam (2018 Edition)From EverandCFP Exam Calculation Workbook: 400+ Calculations to Prepare for the CFP Exam (2018 Edition)Rating: 5 out of 5 stars5/5 (1)

- CFP Certification Exam Practice Question Workbook: 1,000 Comprehensive Practice Questions (2018 Edition)From EverandCFP Certification Exam Practice Question Workbook: 1,000 Comprehensive Practice Questions (2018 Edition)Rating: 5 out of 5 stars5/5 (1)

- Computerised Accounting Practice Set Using MYOB AccountRight - Advanced Level: Australian EditionFrom EverandComputerised Accounting Practice Set Using MYOB AccountRight - Advanced Level: Australian EditionNo ratings yet

- F 2 Final AssessmentDocument15 pagesF 2 Final Assessmentayazmustafa0% (1)

- F3 Mock Questions 201603 PDFDocument14 pagesF3 Mock Questions 201603 PDFMD.Rakibul HasanNo ratings yet

- C02 Sample Questions Feb 2013Document20 pagesC02 Sample Questions Feb 2013Elizabeth Fernandez100% (1)

- Financial Accounting Final AssessmentDocument17 pagesFinancial Accounting Final AssessmentroydkaswekaNo ratings yet

- Financial Accounting Test One (01) James MejaDocument21 pagesFinancial Accounting Test One (01) James MejaroydkaswekaNo ratings yet

- 0452 s07 QP 1Document11 pages0452 s07 QP 1MahmozNo ratings yet

- Oshwal College: Association of Chartered Certified Accountants (ACCA) Foundation Level FA2 Maintaining Financial RecordsDocument6 pagesOshwal College: Association of Chartered Certified Accountants (ACCA) Foundation Level FA2 Maintaining Financial RecordsKhushi SinghNo ratings yet

- BA3 Special Revision MockDocument17 pagesBA3 Special Revision MockSanjeev JayaratnaNo ratings yet

- 7110 w03 QP 1Document12 pages7110 w03 QP 1mstudy123456No ratings yet

- Cambridge International Examinations General Certificate of Education Ordinary Level Principles of Accounts Paper 1 Multiple Choice October/November 2003 1 Hour 15 MinutesDocument12 pagesCambridge International Examinations General Certificate of Education Ordinary Level Principles of Accounts Paper 1 Multiple Choice October/November 2003 1 Hour 15 MinutesMERCY LAWNo ratings yet

- 0452 s04 QP 1Document11 pages0452 s04 QP 1MahmozNo ratings yet

- 0452 w03 QP 1Document11 pages0452 w03 QP 1MahmozNo ratings yet

- 7110 w06 QP 1Document12 pages7110 w06 QP 1mstudy123456No ratings yet

- 7110 s05 QP 1Document12 pages7110 s05 QP 1kaviraj1006No ratings yet

- 7110 s03 QP 1Document12 pages7110 s03 QP 1zahid_mahmood3811No ratings yet

- 7110 s12 QP 12Document8 pages7110 s12 QP 12mstudy123456No ratings yet

- AccountingDocument32 pagesAccountingArShadNo ratings yet

- 0452 w02 QP 1Document13 pages0452 w02 QP 1MahmozNo ratings yet

- Second Semester Accounting Paper 1Document8 pagesSecond Semester Accounting Paper 1egi.academicinfoNo ratings yet

- F3 - Mock B - QuestionsDocument15 pagesF3 - Mock B - QuestionsabasNo ratings yet

- Amended Multiple Choice - Part 2Document6 pagesAmended Multiple Choice - Part 2Ray CheungNo ratings yet

- MCQ Test 1Document8 pagesMCQ Test 1jabbaralijontuNo ratings yet

- 7110 s12 QP 11Document12 pages7110 s12 QP 11mstudy123456No ratings yet

- Template - Multiple Choice Revision 1Document9 pagesTemplate - Multiple Choice Revision 1Vimbai NyakudangaNo ratings yet

- Acc SampleexamDocument12 pagesAcc SampleexamAmber AJNo ratings yet

- 0452 w09 QP 1Document12 pages0452 w09 QP 1MahmozNo ratings yet

- Financial Statements Types Presentation Limitations UsersDocument20 pagesFinancial Statements Types Presentation Limitations UsersGemma PalinaNo ratings yet

- Accounting Paper 1Document12 pagesAccounting Paper 1Tenzin ChoekyNo ratings yet

- FFA Mock Exam Set 6Document19 pagesFFA Mock Exam Set 6miss ainaNo ratings yet

- 7110 w07 QP 1Document12 pages7110 w07 QP 1mstudy123456No ratings yet

- Accountant PaperDocument12 pagesAccountant PaperRajshree DewooNo ratings yet

- Mock Exam FinalDocument23 pagesMock Exam FinalKamaruslan MustaphaNo ratings yet

- Bsec Accounting Challenge 2007Document10 pagesBsec Accounting Challenge 2007Chuột Cao CấpNo ratings yet

- 7110 w09 QP 1Document12 pages7110 w09 QP 1mstudy123456No ratings yet

- EY ENTRANCE TEST final-ACE THE FUTUREDocument18 pagesEY ENTRANCE TEST final-ACE THE FUTURETrà Hương100% (1)

- Financial Reporting and Analysis IIDocument27 pagesFinancial Reporting and Analysis IISagarPirtheeNo ratings yet

- ACCADocument12 pagesACCAanon-502587No ratings yet

- University of Cambridge International Examinations General Certificate of Education Ordinary LevelDocument12 pagesUniversity of Cambridge International Examinations General Certificate of Education Ordinary LevelRobert EdwardsNo ratings yet

- Do Not Turn Over This Question Paper Until You Are Told To Do SoDocument17 pagesDo Not Turn Over This Question Paper Until You Are Told To Do SoMin HeoNo ratings yet

- 0452 s05 QP 1Document12 pages0452 s05 QP 1Kenzy99No ratings yet

- Cambridge International Examinations Cambridge International Advanced Subsidiary and Advanced LevelDocument10 pagesCambridge International Examinations Cambridge International Advanced Subsidiary and Advanced LevelsagarnitishpirtheeNo ratings yet

- Lecture Notes Chapters 1-4Document32 pagesLecture Notes Chapters 1-4BlueFireOblivionNo ratings yet

- 7110 s10 QP 11Document12 pages7110 s10 QP 11mstudy123456No ratings yet

- Principles of Accounts: PAPER 1 Multiple ChoiceDocument12 pagesPrinciples of Accounts: PAPER 1 Multiple Choicemstudy123456No ratings yet

- Mock 2Document14 pagesMock 2Arslan AlviNo ratings yet

- Economic & Budget Forecast Workbook: Economic workbook with worksheetFrom EverandEconomic & Budget Forecast Workbook: Economic workbook with worksheetNo ratings yet

- How to Read a Financial Report: Wringing Vital Signs Out of the NumbersFrom EverandHow to Read a Financial Report: Wringing Vital Signs Out of the NumbersNo ratings yet

- Financial Accounting - Want to Become Financial Accountant in 30 Days?From EverandFinancial Accounting - Want to Become Financial Accountant in 30 Days?Rating: 3.5 out of 5 stars3.5/5 (2)

- Your Amazing Itty Bitty® Book of QuickBooks® TerminologyFrom EverandYour Amazing Itty Bitty® Book of QuickBooks® TerminologyNo ratings yet

- CR 3-23 A-FGJ-A-E-HQQE: Position Qty. Description Single PriceDocument7 pagesCR 3-23 A-FGJ-A-E-HQQE: Position Qty. Description Single PriceIshak AnsarNo ratings yet

- Cover Sheet: Print Form Clear FormDocument1 pageCover Sheet: Print Form Clear FormIshak AnsarNo ratings yet

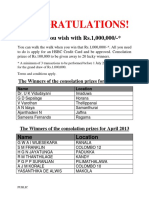

- Congratulations!: Live As You Wish With Rs.1,000,000Document1 pageCongratulations!: Live As You Wish With Rs.1,000,000Ishak AnsarNo ratings yet

- Postcoital ContraceptionDocument6 pagesPostcoital ContraceptionIshak AnsarNo ratings yet

- Hund T FindingsDocument4 pagesHund T FindingsIshak AnsarNo ratings yet

- Calendar 2012 BlackDocument1 pageCalendar 2012 BlackIshak AnsarNo ratings yet

- Project Titles and Supervisors-2011Document24 pagesProject Titles and Supervisors-2011Ishak AnsarNo ratings yet

- Central Bank of Sri Lanka: Premier Financial InstitutionDocument1 pageCentral Bank of Sri Lanka: Premier Financial InstitutionIshak AnsarNo ratings yet

- Department of Electronic Engineering: Final Year Project ReportDocument59 pagesDepartment of Electronic Engineering: Final Year Project ReportIshak AnsarNo ratings yet

- RE and Dfhgrapid ProductDocument6 pagesRE and Dfhgrapid ProductIshak AnsarNo ratings yet

- Semi Log Graph Paper BWDocument1 pageSemi Log Graph Paper BWIshak AnsarNo ratings yet