You might also like

- IU Loan Debt Letter (Example)Document3 pagesIU Loan Debt Letter (Example)Indiana Public Media NewsNo ratings yet

- Tax Tips For Families With ChildrenDocument2 pagesTax Tips For Families With ChildrenallancombesNo ratings yet

- RESP Child EducationDocument7 pagesRESP Child Educationzamai123No ratings yet

- Enrolled by Six Strategy: Peel Post Secondary StrategyDocument12 pagesEnrolled by Six Strategy: Peel Post Secondary Strategyrobert_trewarthaNo ratings yet

- Education Savings Accounts (Esas) : Reyna GobelDocument8 pagesEducation Savings Accounts (Esas) : Reyna GobelAbhishek SinghNo ratings yet

- Study Now. Pay Later Scheme in The Philippines Student LoanDocument11 pagesStudy Now. Pay Later Scheme in The Philippines Student Loanjulia sabasNo ratings yet

- Saving For CollegeDocument2 pagesSaving For CollegeBeth SimsNo ratings yet

- FutureBuilders StrategyDocument2 pagesFutureBuilders StrategyMohammad RizaNo ratings yet

- Matters: A Guide To Financial Support For New Full-Time Students in Higher Education 2012/13Document20 pagesMatters: A Guide To Financial Support For New Full-Time Students in Higher Education 2012/13Wayne Claudio FernandesNo ratings yet

- College Grants Free To StudentsDocument8 pagesCollege Grants Free To StudentshudsonblairNo ratings yet

- How to Pay for College: A Guide to Student Loans, Scholarships, and Making School AffordableFrom EverandHow to Pay for College: A Guide to Student Loans, Scholarships, and Making School AffordableRating: 5 out of 5 stars5/5 (1)

- On The Precipice: The "Fiscal Cliff": Collaborative Financial Solutions, LLCDocument4 pagesOn The Precipice: The "Fiscal Cliff": Collaborative Financial Solutions, LLCJanet BarrNo ratings yet

- Saving For Retirement and A Child's Education at The Same TimeDocument5 pagesSaving For Retirement and A Child's Education at The Same TimeDavid BriggsNo ratings yet

- Building Your Child's Education FundDocument32 pagesBuilding Your Child's Education FundLNP MEDIA GROUP, Inc.No ratings yet

- 529 Plans Glendora FoundationDocument5 pages529 Plans Glendora FoundationGlendora Education FoundationNo ratings yet

- Student Loan Deferment ThesisDocument4 pagesStudent Loan Deferment Thesiscarolinaabramspaterson100% (2)

- Section 529 Plans: Saving For College: Planning EducationDocument3 pagesSection 529 Plans: Saving For College: Planning EducationWasana AndrahannadigeNo ratings yet

- A Review of Childrens Savings Accounts PDFDocument12 pagesA Review of Childrens Savings Accounts PDFjohnNo ratings yet

- Federal Pell GrantDocument9 pagesFederal Pell Grantayde_lldmNo ratings yet

- Financial AidDocument5 pagesFinancial Aidayde_lldmNo ratings yet

- Family Faqs - WebDocument4 pagesFamily Faqs - Webapi-101811350No ratings yet

- CCPA - Eliminating Tuition and Compulsory Fees For Post-Secondary EducationDocument7 pagesCCPA - Eliminating Tuition and Compulsory Fees For Post-Secondary EducationRBeaudryCCLENo ratings yet

- AwardLetter PDFDocument3 pagesAwardLetter PDFColby PalmerNo ratings yet

- Generic FA CombinedDocument12 pagesGeneric FA CombinedReyMejiaNo ratings yet

- June 2014: Top 10 Tax Breaks You'll Miss in 2014Document4 pagesJune 2014: Top 10 Tax Breaks You'll Miss in 2014Income Solutions Wealth ManagementNo ratings yet

- Efu Education PlanDocument4 pagesEfu Education PlanSoofi Bedil BekasNo ratings yet

- 2011 Federal Budget GolombekDocument3 pages2011 Federal Budget GolombekKen WangNo ratings yet

- Caring For My Family PDFDocument16 pagesCaring For My Family PDFBoo Cheng EnNo ratings yet

- Oloya JEduc 70mDocument3 pagesOloya JEduc 70mLUBANGAKENE RICHARDNo ratings yet

- Financial LiteracyDocument23 pagesFinancial Literacyapi-528768453No ratings yet

- I DR Fact Sheet FinalDocument4 pagesI DR Fact Sheet FinalWDIV/ClickOnDetroitNo ratings yet

- RDSP Frequently Asked QuestionsDocument11 pagesRDSP Frequently Asked QuestionsMikaila BurnettNo ratings yet

- BgbproposalDocument10 pagesBgbproposalapi-313113870No ratings yet

- Chapter 13Document28 pagesChapter 13YusufMalangSekaliNo ratings yet

- What to Do When You're 73: Financial Considerations for Life’s StagesFrom EverandWhat to Do When You're 73: Financial Considerations for Life’s StagesNo ratings yet

- Child Care Subsidy Literature ReviewDocument7 pagesChild Care Subsidy Literature Reviewgw1wayrw100% (1)

- Case A Stefan Starts To SaveDocument6 pagesCase A Stefan Starts To SavecathymelverineNo ratings yet

- This Article Explores The Pros and Cons of Investing in Fundisa' - A Savings Initiative Subsidised by The Government and Open To All CitizensDocument4 pagesThis Article Explores The Pros and Cons of Investing in Fundisa' - A Savings Initiative Subsidised by The Government and Open To All CitizensMbalekelwa MpembeNo ratings yet

- Saving EarlyDocument1 pageSaving EarlyEarth na Outer spaceNo ratings yet

- Expanded Eitc SummaryDocument1 pageExpanded Eitc SummaryjmicekNo ratings yet

- Federal Student Aid PSLF ProgramDocument4 pagesFederal Student Aid PSLF ProgramElliotPianoNo ratings yet

- OSAP Student Presentation English PDFDocument29 pagesOSAP Student Presentation English PDFMandy TramiltonNo ratings yet

- Asse T Revi Ew: Activi Ty Centr e Educa Tion Plann ErDocument13 pagesAsse T Revi Ew: Activi Ty Centr e Educa Tion Plann ErkvijayasokNo ratings yet

- 20 InsiderstrategiescappexDocument24 pages20 Insiderstrategiescappexapi-188979941No ratings yet

- Smartkid RPDocument6 pagesSmartkid RPRajbir Singh YadavNo ratings yet

- 14S UMHS Frequently Asked QuestionsDocument2 pages14S UMHS Frequently Asked QuestionsDiorella Marie López GonzálezNo ratings yet

- Free Money by John Around Him (Write A Conclusion)Document1 pageFree Money by John Around Him (Write A Conclusion)jeanninestankoNo ratings yet

- Investing in Your FutureDocument34 pagesInvesting in Your FutureCristiNo ratings yet

- Collection of InformationDocument7 pagesCollection of InformationdeepashajiNo ratings yet

- Finance Matters: Tuition and Examination FeesDocument4 pagesFinance Matters: Tuition and Examination FeesAnonymous issxPUNo ratings yet

- The Arc of North Carolina Compares N.C. House and Senate BudgetsDocument3 pagesThe Arc of North Carolina Compares N.C. House and Senate BudgetsNC Policy WatchNo ratings yet

- Form - DIME Calclator (Life Insurance)Document2 pagesForm - DIME Calclator (Life Insurance)Corbin Lindsey100% (1)

- Child Tax Credit and ACTCDocument1 pageChild Tax Credit and ACTCNelwin ThomasNo ratings yet

- Thesis Student Loan ThresholdDocument6 pagesThesis Student Loan Thresholdseewbyvff100% (2)

- How FEE-HELP Loans Can Pay for Your University Tuition FeesDocument4 pagesHow FEE-HELP Loans Can Pay for Your University Tuition FeesSedana HartaNo ratings yet

- FactorsDocument70 pagesFactorsjashanNo ratings yet

- Fin Aid NightDocument7 pagesFin Aid NightcollegeofficeNo ratings yet

- MM Tep Guide To Rdsps enDocument12 pagesMM Tep Guide To Rdsps enmosh1243No ratings yet

- Education LoanDocument29 pagesEducation LoanPravesh Kumar Singh100% (2)

- Chutiya RatingDocument1 pageChutiya Ratingapi-97071804No ratings yet

- Chutiya RatingDocument1 pageChutiya Ratingapi-97071804No ratings yet

- Ins Trav TravelinsurancebroDocument2 pagesIns Trav Travelinsurancebroapi-97071804No ratings yet

- Mortgage Insurance ArticleDocument1 pageMortgage Insurance Articleapi-97071804No ratings yet

- Ins Trav InsurancemftistudentsbrochureDocument2 pagesIns Trav Insurancemftistudentsbrochureapi-97071804No ratings yet

- Ins Flex Guideon 17Document1 pageIns Flex Guideon 17api-97071804No ratings yet

- Letter of Recommendation From EmbassyDocument1 pageLetter of Recommendation From Embassyapi-97071804No ratings yet

- What Is An RRSP?: Prepared For CHOU Financial June 14, 2012Document3 pagesWhat Is An RRSP?: Prepared For CHOU Financial June 14, 2012api-97071804No ratings yet

- Tax-Free Savings Account: Investment SolutionsDocument3 pagesTax-Free Savings Account: Investment Solutionsapi-97071804No ratings yet

- Letter of Recommendations For Chou Financial From Thai Consulate GeneralDocument1 pageLetter of Recommendations For Chou Financial From Thai Consulate Generalapi-97071804No ratings yet

- Diploma Resp BrochureDocument16 pagesDiploma Resp Brochureapi-97071804No ratings yet

- Start Investing For Tomorrow: Your Guide To RrspsDocument12 pagesStart Investing For Tomorrow: Your Guide To Rrspsapi-97071804No ratings yet

- 13-441a English BrochureDocument16 pages13-441a English Brochureapi-97071804No ratings yet

- FM303 Tutorial Question Week 5Document3 pagesFM303 Tutorial Question Week 5Smriti LalNo ratings yet

- Factors Influencing The Investors' Decision Making in Stock MarketDocument27 pagesFactors Influencing The Investors' Decision Making in Stock Marketحمامة السلامNo ratings yet

- Horizontal and Vertical Analysis of ProfitDocument3 pagesHorizontal and Vertical Analysis of ProfitIfzal AhmadNo ratings yet

- Fairholme Fund 2017 Q4 Letter PDFDocument60 pagesFairholme Fund 2017 Q4 Letter PDFSmitty WNo ratings yet

- EarlyBird PresentationDocument8 pagesEarlyBird PresentationbrisbourneNo ratings yet

- Azerbaijan Oil Company 2017 IFRS ReportsDocument96 pagesAzerbaijan Oil Company 2017 IFRS ReportsMehemmed MemmedliNo ratings yet

- ENV Envestnet Investor Presentation Draft 2018-01-09Document25 pagesENV Envestnet Investor Presentation Draft 2018-01-09Ala BasterNo ratings yet

- MBA Syllabus 3rd SemDocument8 pagesMBA Syllabus 3rd SemShivam Thakur 5079No ratings yet

- Accounting Textbook Solutions - 66Document19 pagesAccounting Textbook Solutions - 66acc-expertNo ratings yet

- CBSE Class 12 Accountancy Accounting For Share Capital and Debenture WorksheetDocument3 pagesCBSE Class 12 Accountancy Accounting For Share Capital and Debenture WorksheetJenneil CarmichaelNo ratings yet

- Mexico Private Equity Industry 1990-2006Document12 pagesMexico Private Equity Industry 1990-2006Manuel ReyesNo ratings yet

- Work With Financial Planners 1. Enumerate The Three Basic Choices and Managing Your Money and Explain It's Description in Your Own WordDocument2 pagesWork With Financial Planners 1. Enumerate The Three Basic Choices and Managing Your Money and Explain It's Description in Your Own WordRhia shin PasuquinNo ratings yet

- MCQ Accounts For 10+2 TS Grewal SirDocument66 pagesMCQ Accounts For 10+2 TS Grewal SirYash ChhabraNo ratings yet

- 2 Sma SM 1Document12 pages2 Sma SM 1Pondok Pesantren Darunnajah CipiningNo ratings yet

- Assessing A New Venture's Financial Strength and ViabilityDocument6 pagesAssessing A New Venture's Financial Strength and ViabilityAsif KureishiNo ratings yet

- Types of Business Organisation: Textbook, Chapter 4 (PG 35-51)Document12 pagesTypes of Business Organisation: Textbook, Chapter 4 (PG 35-51)Vincent ChurchillNo ratings yet

- Financial Health RatiosDocument29 pagesFinancial Health Ratiosmushiechan888No ratings yet

- Audit Super 100 Important QuestionsDocument92 pagesAudit Super 100 Important QuestionswipeyourassNo ratings yet

- Finance - Treasury BillDocument38 pagesFinance - Treasury BillJayesh BhagatNo ratings yet

- An Investment Perspective of HRMDocument18 pagesAn Investment Perspective of HRMSoyed Mohammed Zaber HossainNo ratings yet

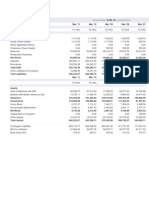

- Balance Sheet of ICICI BankDocument3 pagesBalance Sheet of ICICI Banknikitagupta44No ratings yet

- Abeeb's ProjectDocument92 pagesAbeeb's ProjectOlu SamNo ratings yet

- Forex Trading Advantages & Disadvantages ExplainedDocument2 pagesForex Trading Advantages & Disadvantages ExplainedKhushi SiviaNo ratings yet

- Rules of The Game:: Please Refer To The Next Sheet 'Sectors and Companies' For The Closing PricesDocument8 pagesRules of The Game:: Please Refer To The Next Sheet 'Sectors and Companies' For The Closing PricesAbhinav PrakashNo ratings yet

- MATERIALDocument23 pagesMATERIALPocari OnceNo ratings yet

- Option Chain Analysis With Examples - Dot Net TutorialsDocument9 pagesOption Chain Analysis With Examples - Dot Net TutorialsMandi100% (1)

- Balance Transfer From Last Month Salary Amount in Hand OthersDocument3 pagesBalance Transfer From Last Month Salary Amount in Hand OthersJithin RoyNo ratings yet

- The Wall Street Journal 10 June 2023Document58 pagesThe Wall Street Journal 10 June 2023Raden Angga Widitama PutraNo ratings yet

- Sachdevajk, Journal Manager, 5-4-3 - Sumeet-1Document26 pagesSachdevajk, Journal Manager, 5-4-3 - Sumeet-1Parth DongaNo ratings yet

- Time ValueDocument6 pagesTime Valuechris david100% (1)