You might also like

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Anti-Inflationary Policy in IndiaDocument14 pagesAnti-Inflationary Policy in Indiaapi-3712367No ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Policybrief Nov05Document6 pagesPolicybrief Nov05api-3712367No ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- WEight Training ScheduleDocument2 pagesWEight Training Scheduleapi-3712367100% (1)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Foreign Exchange Management Policy in IndiaDocument6 pagesForeign Exchange Management Policy in Indiaapi-371236767% (3)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Report OnDocument9 pagesReport Onapi-3712367No ratings yet

- Fema CDocument5 pagesFema Capi-3712367No ratings yet

- Macroeconomics AssignmentsDocument15 pagesMacroeconomics Assignmentsapi-3712367No ratings yet

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- SubPrime Mortgage MarketDocument6 pagesSubPrime Mortgage Marketapi-3712367No ratings yet

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Subprime Toxic Debt - Bloomberg July07Document10 pagesSubprime Toxic Debt - Bloomberg July07api-3712367No ratings yet

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- FFRChange HistoryDocument1 pageFFRChange Historyapi-3712367No ratings yet

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Subprime FinalDocument34 pagesSubprime Finalapi-3712367No ratings yet

- SubprimeDocument31 pagesSubprimeapi-3712367No ratings yet

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

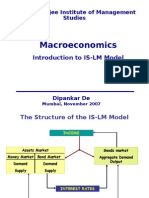

- MacroEconomics - Lecture 4 - IsLM ModelDocument24 pagesMacroEconomics - Lecture 4 - IsLM Modelapi-3712367No ratings yet

- Balanced ScorecardDocument67 pagesBalanced Scorecardapi-3712367100% (4)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Global Economics - IndiaDocument2 pagesGlobal Economics - Indiaapi-3712367No ratings yet

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Sebi TocDocument33 pagesSebi Tocapi-3712367No ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- BSC & Knowledge ManagementDocument3 pagesBSC & Knowledge Managementapi-3712367100% (1)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Balanced ScorecardDocument13 pagesBalanced Scorecardapi-3712367No ratings yet

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Amortization Calculator - Wikipedia, The Free EncyclopediaDocument3 pagesAmortization Calculator - Wikipedia, The Free Encyclopediaapi-3712367No ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- MacroEconomics - Lecture 4 SKM MultiplierDocument7 pagesMacroEconomics - Lecture 4 SKM Multiplierapi-3712367No ratings yet

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- MacroEconomics - Lecture 5 Introduction To ISLMDocument21 pagesMacroEconomics - Lecture 5 Introduction To ISLMapi-3712367100% (1)

- Micro Economics PresentationDocument18 pagesMicro Economics Presentationapi-3712367No ratings yet

- Developing and Implementing An Effective Talent Management StrategyDocument12 pagesDeveloping and Implementing An Effective Talent Management StrategyStephen Olieka100% (4)

- AWS Exam Cancellation Refund Policies and Other FeesDocument1 pageAWS Exam Cancellation Refund Policies and Other FeesZeeshan HasanNo ratings yet

- Bond Risk - Duration and ConvexityDocument26 pagesBond Risk - Duration and ConvexityamcucNo ratings yet

- Regulatory Implementation of The Statement of Principles Regarding The Activities of Credit Rating AgenciesDocument38 pagesRegulatory Implementation of The Statement of Principles Regarding The Activities of Credit Rating AgenciesChou ChantraNo ratings yet

- CRISIL Ratings Research Und CRISIL Ratings Rating Scales 2013Document8 pagesCRISIL Ratings Research Und CRISIL Ratings Rating Scales 2013chiragNo ratings yet

- 27r-03 Schedule Classification SystemDocument10 pages27r-03 Schedule Classification SystemHERNANDEZNo ratings yet

- Study Material On DiscriminantAnalysisDocument24 pagesStudy Material On DiscriminantAnalysisanupam99276No ratings yet

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Fabozzi Ch13 BMAS 7thedDocument36 pagesFabozzi Ch13 BMAS 7thedAvinash KumarNo ratings yet

- A Comprehensive Review of Metrics of Building EnvironmentalDocument11 pagesA Comprehensive Review of Metrics of Building Environmentalcarlos686210No ratings yet

- Module 6 Gathering Performance InformationDocument14 pagesModule 6 Gathering Performance Informationmitashi jainNo ratings yet

- IL&FS CrisisDocument6 pagesIL&FS CrisisPrakash SundaramNo ratings yet

- Guidelines) : Exemption: Provisions of Act/SchemesDocument14 pagesGuidelines) : Exemption: Provisions of Act/Schemes2009a003No ratings yet

- Jcr-Vis: Global Credit Rating IndustryDocument20 pagesJcr-Vis: Global Credit Rating Industryusmanahmed01No ratings yet

- Beta B - I1 Form (Debraj Chatterjee)Document2 pagesBeta B - I1 Form (Debraj Chatterjee)Vindyanchal KumarNo ratings yet

- Characteristics of Developed CountriesDocument28 pagesCharacteristics of Developed CountriesCasie Mack100% (1)

- Impact Assessment TemplateDocument3 pagesImpact Assessment Templatezio_nanoNo ratings yet

- Markit Itraxx Europe Series 18 RulebookDocument10 pagesMarkit Itraxx Europe Series 18 RulebookPeter FraserNo ratings yet

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Bir Horizons BL 28mar2019Document5 pagesBir Horizons BL 28mar2019Praful K RajuNo ratings yet

- Pringles Potato Chip Mailing ChallengeDocument2 pagesPringles Potato Chip Mailing ChallengeGina FelyaNo ratings yet

- Hardwick Route 32 Road Work Public HearingDocument9 pagesHardwick Route 32 Road Work Public HearingThe Republican/MassLive.comNo ratings yet

- MBA 620 - Assignment 2Document6 pagesMBA 620 - Assignment 2GeorgeStylianouNo ratings yet

- Chapter 3 - Levels of Measurement and ScalingDocument10 pagesChapter 3 - Levels of Measurement and ScalingRajan NandolaNo ratings yet

- Mutual Fund:: Asset Management CompanyDocument43 pagesMutual Fund:: Asset Management CompanymalaynvNo ratings yet

- Rating Scales: Types of Rating ScaleDocument6 pagesRating Scales: Types of Rating ScaleANITTA SNo ratings yet

- Meralco Strategy AnalysisDocument23 pagesMeralco Strategy AnalysisReynaldo De Leon80% (5)

- BNP emDocument20 pagesBNP emchaotic_pandemoniumNo ratings yet

- Mohana - A Study On Performance Appraisal in Event Management Sai Leaf Plate Indutsry at KarurDocument91 pagesMohana - A Study On Performance Appraisal in Event Management Sai Leaf Plate Indutsry at KarurAnonymous qRAAcePNo ratings yet

- H03875Document4 pagesH03875AQUILES CARRERANo ratings yet

- Enron ScandalDocument5 pagesEnron ScandalIshani Bhattacharya0% (1)

- Wello Jemal Research1Document43 pagesWello Jemal Research1Javeed ForeverNo ratings yet