You might also like

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (589)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (842)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5806)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1091)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Mega Force - Fire Fighting EnginesDocument4 pagesMega Force - Fire Fighting EngineskuraimundNo ratings yet

- TSDOS Adv Diag Testing DW PDFDocument61 pagesTSDOS Adv Diag Testing DW PDFDhammika Dharmadasa100% (1)

- UPS Riello Aros Sentinel ProDocument4 pagesUPS Riello Aros Sentinel ProagoengkoxcimenkNo ratings yet

- Customer Presentation LEWA EcoflowDocument35 pagesCustomer Presentation LEWA EcoflowMohammed ShallabyNo ratings yet

- ONGCDocument21 pagesONGCSafia AfreenNo ratings yet

- EPC BrochureDocument32 pagesEPC BrochureAmarinder Singh SandhuNo ratings yet

- Liquid Mud Plant VesselDocument29 pagesLiquid Mud Plant VesselMich100% (1)

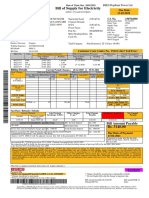

- Bill of Supply For Electricity: Due Date: 13-02-2021Document1 pageBill of Supply For Electricity: Due Date: 13-02-2021Killer HeadacheNo ratings yet

- Hot and Cold Water DespensorDocument6 pagesHot and Cold Water DespensorMohamedFasilNo ratings yet

- APEC-by-Corazon-C.-Blanes APECDocument4 pagesAPEC-by-Corazon-C.-Blanes APECChristopher PilotinNo ratings yet

- Littelfuse Magnetic Sensors and Reed Switches Inductive Load Arc Suppression Application Note PDFDocument2 pagesLittelfuse Magnetic Sensors and Reed Switches Inductive Load Arc Suppression Application Note PDFMarcelo SantibañezNo ratings yet

- Catálogo SM6 2017Document156 pagesCatálogo SM6 2017Jose OlivaresNo ratings yet

- White Paper #10609 Marco FERRARIDocument9 pagesWhite Paper #10609 Marco FERRARIJailanee ImakNo ratings yet

- 11-7579-WP Pipeline Hydraulics D PDFDocument15 pages11-7579-WP Pipeline Hydraulics D PDFLucas WalkerNo ratings yet

- Serbia 2014Document181 pagesSerbia 2014Hoang Duy ChinhNo ratings yet

- AP Electrical Safety SWPDocument12 pagesAP Electrical Safety SWPjvigforuNo ratings yet

- NTPC Project FinalDocument89 pagesNTPC Project Finalaja295100% (1)

- Project On Induction ProgramDocument50 pagesProject On Induction ProgramSupriya Singh45% (11)

- Reciprocating Compressors-HIT Dryers - ENGDocument16 pagesReciprocating Compressors-HIT Dryers - ENGJavier Moctezuma MNo ratings yet

- Westinghouse TB-04-13Document6 pagesWestinghouse TB-04-13Chris StroudNo ratings yet

- Powerengineering201704 DLDocument49 pagesPowerengineering201704 DLFaisal KasanofaNo ratings yet

- Glass Industries in IndiaDocument3 pagesGlass Industries in IndiaAnup PatodiNo ratings yet

- XLPE Insulated Cable 220 KV NexanDocument2 pagesXLPE Insulated Cable 220 KV Nexangyanendra_vatsa4380No ratings yet

- GD GDK SeriesDocument12 pagesGD GDK Serieswidnu wirasetiaNo ratings yet

- Voestalpine Heavy Plate TTD ALDUR E 14012013Document13 pagesVoestalpine Heavy Plate TTD ALDUR E 14012013Dragan JerčićNo ratings yet

- Global Oil & Gas - 130813 - BarclaysDocument56 pagesGlobal Oil & Gas - 130813 - Barclaysalokgupta87No ratings yet

- Accreditation Criteria DocumentsV2Document59 pagesAccreditation Criteria DocumentsV2Syahruulaa RazeehaNo ratings yet

- Waaree Gurantee CertificateDocument9 pagesWaaree Gurantee Certificatemurugan199118No ratings yet

- ZO3 AngDocument2 pagesZO3 Angmarcofffmota3196No ratings yet

- Technical Submittal of NIKKONDocument28 pagesTechnical Submittal of NIKKONJaved BhattiNo ratings yet