You might also like

- Group B&D - Case 19 - Fonderia PresentationDocument24 pagesGroup B&D - Case 19 - Fonderia PresentationVinithi Thongkampala100% (2)

- Case of Dorchester LTD (Assignment)Document7 pagesCase of Dorchester LTD (Assignment)ShahedNo ratings yet

- Butler Lumber - Pro Forma - Balance and Income StatementDocument4 pagesButler Lumber - Pro Forma - Balance and Income StatementJack Benjamin83% (6)

- Case 26 Rockboro Group ADocument27 pagesCase 26 Rockboro Group AKanoknad KalaphakdeeNo ratings yet

- Rockboro Machine Tools Corporation Case QuestionsDocument1 pageRockboro Machine Tools Corporation Case QuestionsMasumiNo ratings yet

- Butler Lumber CaseDocument7 pagesButler Lumber CaseSam Rosenbaum100% (1)

- Butler Lumber 1Document6 pagesButler Lumber 1Bhavna Singh33% (3)

- FM SolutionDocument11 pagesFM SolutionBilal Naseer100% (4)

- Oblicon Project Bar Review QuestionsDocument35 pagesOblicon Project Bar Review QuestionsSarah Cadiogan88% (8)

- Butler Lumber Case Study SolutionDocument8 pagesButler Lumber Case Study SolutionBagus Be WeNo ratings yet

- Act 8Document6 pagesAct 8Carlos MartinezNo ratings yet

- Grennell Farm SolutionDocument6 pagesGrennell Farm SolutionMichael TorresNo ratings yet

- Butler Lumber Company Case SolutionDocument18 pagesButler Lumber Company Case SolutionNabab Shirajuddoula75% (8)

- Butler Lumber Company: Following Questions Are Answered in This Case Study SolutionDocument3 pagesButler Lumber Company: Following Questions Are Answered in This Case Study SolutionTalha SiddiquiNo ratings yet

- Butler Lumber CompanyDocument8 pagesButler Lumber CompanyAnmol ChopraNo ratings yet

- Sabya BhaiDocument6 pagesSabya BhaiamanNo ratings yet

- Butler Lumber Case SolutionDocument4 pagesButler Lumber Case SolutionCharleneNo ratings yet

- Blaine SolutionDocument4 pagesBlaine Solutionchintan MehtaNo ratings yet

- Rockboro Machine Tools Corporation: Source: Author EstimatesDocument10 pagesRockboro Machine Tools Corporation: Source: Author EstimatesMasumi0% (2)

- Case 3: Rockboro Machine Tools Corporation Executive SummaryDocument1 pageCase 3: Rockboro Machine Tools Corporation Executive SummaryMaricel GuarinoNo ratings yet

- Sure CutDocument1 pageSure Cutchch917No ratings yet

- BBBY Case ExerciseDocument7 pagesBBBY Case ExerciseSue McGinnisNo ratings yet

- Super ProjectDocument2 pagesSuper ProjectAnkit MehtaNo ratings yet

- Butler Lumber CaseDocument14 pagesButler Lumber CaseSangeet SaritaNo ratings yet

- Case Study: Financial Ratios Analysis: Pulp, Paper, and Paperboard, IncDocument3 pagesCase Study: Financial Ratios Analysis: Pulp, Paper, and Paperboard, Inchelsamra0% (2)

- Al-Ghazi Tractors - Final ProjectDocument27 pagesAl-Ghazi Tractors - Final ProjectAwais MasoodNo ratings yet

- Butler Lumber Company Case ProblemDocument2 pagesButler Lumber Company Case ProblemJem JemNo ratings yet

- Butler Lumber CaseDocument14 pagesButler Lumber CaseSamarth Mewada83% (6)

- Butler Lumber CompanyDocument4 pagesButler Lumber Companynickiminaj221421No ratings yet

- ButlerDocument8 pagesButlerHadi Khawaja100% (1)

- Butler Excel Sheets (Group 2)Document11 pagesButler Excel Sheets (Group 2)Nathan ClarkinNo ratings yet

- Hill CountryDocument8 pagesHill CountryAtif Raza AkbarNo ratings yet

- (S3) Butler Lumber - EnGDocument11 pages(S3) Butler Lumber - EnGdavidinmexicoNo ratings yet

- West Jet AirlinesDocument2 pagesWest Jet AirlinesPraeen Kc100% (1)

- Case: Blaine Kitchenware, IncDocument5 pagesCase: Blaine Kitchenware, IncWilliam NgNo ratings yet

- Clarkson TemplateDocument7 pagesClarkson TemplateJeffery KaoNo ratings yet

- Hill Country CaseDocument5 pagesHill Country CaseDeepansh Kakkar100% (1)

- Mid Term ExamDocument4 pagesMid Term ExamChris Rosbeck0% (1)

- Cred&coll Reviewer MidtermsDocument24 pagesCred&coll Reviewer MidtermsElla Marie LopezNo ratings yet

- Walmart Case 150Document38 pagesWalmart Case 150Phakpoom Naji100% (2)

- Butler Lumber CaseDocument4 pagesButler Lumber CaseLovin SeeNo ratings yet

- Butler Lumber SuggestionsDocument2 pagesButler Lumber Suggestionsmannu.abhimanyu3098No ratings yet

- The Butler Lumber Company - AH1Document6 pagesThe Butler Lumber Company - AH1shaluxlriNo ratings yet

- Butler Lumber Final First DraftDocument12 pagesButler Lumber Final First DraftAdit Swarup100% (3)

- Case #7 Butler LumberDocument2 pagesCase #7 Butler LumberBianca UcheNo ratings yet

- Butler Lumber Case DiscussionDocument3 pagesButler Lumber Case DiscussionJayzie Li100% (1)

- Butler CaseDocument16 pagesButler Casea_14sNo ratings yet

- Bulter Lumber CaseDocument3 pagesBulter Lumber CaseSwarna RSNo ratings yet

- Butler Lumber Case AnalysisDocument2 pagesButler Lumber Case AnalysisDucNo ratings yet

- Analysis Butler Lumber CompanyDocument3 pagesAnalysis Butler Lumber CompanyRoberto LlerenaNo ratings yet

- Joneja Bright Steels: The Cash Discount DecisionDocument13 pagesJoneja Bright Steels: The Cash Discount DecisionDiv_nNo ratings yet

- Hill Country Snack Food Co.Document7 pagesHill Country Snack Food Co.Anish NarulaNo ratings yet

- Sec6 Group13 SimulationDocument5 pagesSec6 Group13 SimulationAvinashDeshpande1989100% (1)

- Clarkson Lumber Company (7.0)Document17 pagesClarkson Lumber Company (7.0)Hassan Mohiuddin100% (1)

- Case QuestionsDocument6 pagesCase QuestionslddNo ratings yet

- M&A and Corporate Restructuring) - Prof. Ercos Valdivieso: Jung Keun Kim, Yoon Ho Hur, Soo Hyun Ahn, Jee Hyun KoDocument2 pagesM&A and Corporate Restructuring) - Prof. Ercos Valdivieso: Jung Keun Kim, Yoon Ho Hur, Soo Hyun Ahn, Jee Hyun Ko고지현100% (1)

- BCB Case StudyDocument20 pagesBCB Case Studycarota89100% (1)

- Assignment 7 - Clarkson LumberDocument5 pagesAssignment 7 - Clarkson Lumbertesttest1No ratings yet

- Case Analysis - Toy WorldDocument11 pagesCase Analysis - Toy Worldvarjin71% (7)

- Blaine Kitchenware 3Document8 pagesBlaine Kitchenware 3Chris100% (1)

- LYons Bond Case SolutionDocument2 pagesLYons Bond Case SolutionGautam Sethi75% (4)

- FIN254 Assignment# 1Document2 pagesFIN254 Assignment# 1Zahidul IslamNo ratings yet

- Analysis: Operating ActivitiesDocument3 pagesAnalysis: Operating ActivitiesSammy Dalie Soto Bernaola0% (1)

- Financial Statements, Taxes, and Cash FlowDocument46 pagesFinancial Statements, Taxes, and Cash FlowgagafikNo ratings yet

- Exercises AllDocument9 pagesExercises AllLede Ann Calipus YapNo ratings yet

- Butler Lumber Company Income StatementDocument8 pagesButler Lumber Company Income StatementpuspemoltuNo ratings yet

- Assignment 1-Gideon Zoiku-R1810D6621 FMDocument16 pagesAssignment 1-Gideon Zoiku-R1810D6621 FMBrett ViceNo ratings yet

- Credit Guarantee Fund Trust For Micro & Small EnterprisesDocument19 pagesCredit Guarantee Fund Trust For Micro & Small EnterprisesAnand SinghNo ratings yet

- Marriott Corporation The Cost of Capital Case Study AnalysisDocument21 pagesMarriott Corporation The Cost of Capital Case Study AnalysisvasanthaNo ratings yet

- Investment Analysis and Portfolio Management-KRISTINA L PDFDocument166 pagesInvestment Analysis and Portfolio Management-KRISTINA L PDFWahyu S. Furqonnanto100% (2)

- Organized Crime in BulgariaDocument204 pagesOrganized Crime in BulgariahellasrocketmailNo ratings yet

- Real Estate Mortgage - SampleDocument3 pagesReal Estate Mortgage - SampleCharlotte GallegoNo ratings yet

- Chandan Project PDFDocument95 pagesChandan Project PDFChandan Kumar NNo ratings yet

- Problem Set-Leverage and Capital StructureDocument10 pagesProblem Set-Leverage and Capital StructuremaazNo ratings yet

- A Study On The Financial Analysis of Reliance Industries LimitedDocument13 pagesA Study On The Financial Analysis of Reliance Industries LimitedIJAR JOURNAL100% (1)

- Euro Currency MarketDocument33 pagesEuro Currency Marketsfkokane83% (6)

- A Comparative Analysis of Annual Report of "United Spirits LTD" Across IndustriesDocument12 pagesA Comparative Analysis of Annual Report of "United Spirits LTD" Across Industriesrishimahesh2005No ratings yet

- الأزمة المالية العالمية 2008 جذورها و تداعياتها ساعد مرابط PDFDocument15 pagesالأزمة المالية العالمية 2008 جذورها و تداعياتها ساعد مرابط PDFساعدNo ratings yet

- Tutorial 4 TVM ApplicationDocument4 pagesTutorial 4 TVM ApplicationTrần ThảoNo ratings yet

- Ifr 2019-11-02 PDFDocument96 pagesIfr 2019-11-02 PDFPiyushNo ratings yet

- JA Personal Finance - Blended - Answer Key - 19-20Document5 pagesJA Personal Finance - Blended - Answer Key - 19-20sheima siddigNo ratings yet

- Tan v. Rodil EnterprisesDocument3 pagesTan v. Rodil EnterprisesTootsie GuzmaNo ratings yet

- Public Debt and Its Sustainability at State Level-A Study of Kerala Literature ReviewDocument4 pagesPublic Debt and Its Sustainability at State Level-A Study of Kerala Literature ReviewM CharlesNo ratings yet

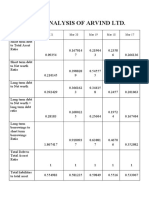

- Ratio Analysis of Arvind LTD.: Ratios Mar 21 Mar 20 Mar 19 Mar 18 Mar 17Document10 pagesRatio Analysis of Arvind LTD.: Ratios Mar 21 Mar 20 Mar 19 Mar 18 Mar 17simranNo ratings yet

- Penalties, Time Limit and Forms May 2023Document12 pagesPenalties, Time Limit and Forms May 2023VenkataRajuNo ratings yet

- In What Context Are Terms Pledge, Hypothecation and Mortgage UsedDocument2 pagesIn What Context Are Terms Pledge, Hypothecation and Mortgage Useddineshjain11100% (1)

- Grade Xi HOLIDAY HOMEWORK-2016-17 Commerce Stream AccountancyDocument36 pagesGrade Xi HOLIDAY HOMEWORK-2016-17 Commerce Stream AccountancysanjeevaniNo ratings yet

- Capital Structure: Meaning and Theories Presented by Namrata Deb 1 PGDBMDocument20 pagesCapital Structure: Meaning and Theories Presented by Namrata Deb 1 PGDBMDhiraj SharmaNo ratings yet

- Dominos ReportDocument20 pagesDominos ReportDisha HalderNo ratings yet