You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5813)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1092)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (844)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (348)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Instant Download Ebook PDF Academic Transformation The Road To College Success 3rd Edition PDF ScribdDocument41 pagesInstant Download Ebook PDF Academic Transformation The Road To College Success 3rd Edition PDF Scribddavid.ginder334100% (42)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Ex Fix Safe Zone For UE by Fahad AJDocument1 pageEx Fix Safe Zone For UE by Fahad AJAlHasaNo ratings yet

- Scenario (Business Area) : Business Process: : Functional SpecificationDocument21 pagesScenario (Business Area) : Business Process: : Functional SpecificationsapeinsNo ratings yet

- Municipality of Paniqui Term PaperDocument23 pagesMunicipality of Paniqui Term PaperNhevia de GuzmanNo ratings yet

- Faculty Mentor: Dr. PRABIR Jana Mr. Deepak Panghal Industry Mentor: Mr. UDAY N B (Sales & Technical Manager)Document2 pagesFaculty Mentor: Dr. PRABIR Jana Mr. Deepak Panghal Industry Mentor: Mr. UDAY N B (Sales & Technical Manager)Varun MehrotraNo ratings yet

- Lecture 13 - Lumber GradingDocument20 pagesLecture 13 - Lumber GradingimanolkioNo ratings yet

- Yarn Over 101Document3 pagesYarn Over 101Bea Ann83% (6)

- Compensation Management & Job EvaluationDocument20 pagesCompensation Management & Job EvaluationSunil Patnaik100% (1)

- Hayden Res 10/2017Document2 pagesHayden Res 10/2017Hayden MichaelNo ratings yet

- Spirulina in Sadhana ForestDocument20 pagesSpirulina in Sadhana ForestsarathNo ratings yet

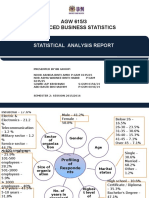

- AGW 615/3 Advanced Business Statistics: Statistical Analysis ReportDocument10 pagesAGW 615/3 Advanced Business Statistics: Statistical Analysis ReportNida AmriNo ratings yet

- Gender Stereotypes Discussion Questions PDFDocument2 pagesGender Stereotypes Discussion Questions PDFHypeLensNo ratings yet

- Mini Flow Channel ExperimentDocument9 pagesMini Flow Channel Experimentpotato92No ratings yet

- NIHMS753481 Supplement Supplemental DataDocument124 pagesNIHMS753481 Supplement Supplemental DataAle ZevallosNo ratings yet

- Guidance For The Management of Crude Oil Incidents - ENDocument178 pagesGuidance For The Management of Crude Oil Incidents - ENAbdul KaderNo ratings yet

- 8 - Problem Reduction SearchDocument31 pages8 - Problem Reduction SearchArchana PanwarNo ratings yet

- Fgtech Driver List Truck TractorDocument6 pagesFgtech Driver List Truck TractorTuấn NeoNo ratings yet

- Building and Enhancing New Literacies Across The Curriculum: Lomoarcpsd - 5406869Document12 pagesBuilding and Enhancing New Literacies Across The Curriculum: Lomoarcpsd - 5406869Nel BorniaNo ratings yet

- Enforcement Question 3Document2 pagesEnforcement Question 3Tan Chen WuiNo ratings yet

- News Letter Philips Sod87 (200912)Document2 pagesNews Letter Philips Sod87 (200912)sole_zemunNo ratings yet

- Neff Oxford Handbook Hip-Hop Studies 1/17Document16 pagesNeff Oxford Handbook Hip-Hop Studies 1/17Ali ColleenNo ratings yet

- Excavator O&KDocument8 pagesExcavator O&Keknasius iwan sugoro100% (2)

- Dipesh Chakrabarty: Fifty Years of E P Thompson's The Making of The English Working ClassDocument3 pagesDipesh Chakrabarty: Fifty Years of E P Thompson's The Making of The English Working ClassTigersEye99No ratings yet

- Master Syllabus Fix TOM-JAN2019-BOED PDFDocument4 pagesMaster Syllabus Fix TOM-JAN2019-BOED PDFBogiNo ratings yet

- Rurban PowerPoint Presentation Final OneDocument65 pagesRurban PowerPoint Presentation Final OneVIVEK VERMANo ratings yet

- Narrative ReportDocument4 pagesNarrative ReportAlbert Bagasala AsidoNo ratings yet

- 31725H Unit6 Pef 20190814Document25 pages31725H Unit6 Pef 20190814hello1737828No ratings yet

- Case Study Stroke RehabilitationDocument1 pageCase Study Stroke RehabilitationJanantik PandyaNo ratings yet

- Printing Inks - Issues, Guidance and RegulationsDocument93 pagesPrinting Inks - Issues, Guidance and RegulationsDinesh RajputNo ratings yet

- Descriptive TextDocument7 pagesDescriptive Textayu suhestiNo ratings yet