You might also like

- Outline Foreclosure Defense - Tila & RespaDocument13 pagesOutline Foreclosure Defense - Tila & RespaEdward BrownNo ratings yet

- Fannie Mae Term Sheet For The Citigroup - New Century Mortgage Deal 2006-09-07 Cmlti 2006-NC2Document50 pagesFannie Mae Term Sheet For The Citigroup - New Century Mortgage Deal 2006-09-07 Cmlti 2006-NC283jjmackNo ratings yet

- SEC Vs Citigroup CDOs RMBS and Class V III Funding Comp-Pr2011-214Document21 pagesSEC Vs Citigroup CDOs RMBS and Class V III Funding Comp-Pr2011-214CarrieonicNo ratings yet

- World Bank Insider Blows Whistle On Corruption - Federal Reserve May 2013Document8 pagesWorld Bank Insider Blows Whistle On Corruption - Federal Reserve May 2013CarrieonicNo ratings yet

- Class V III ProspectusDocument209 pagesClass V III ProspectusCarrieonicNo ratings yet

- FCA Citi Mortgage Complaint-In-InterventionDocument36 pagesFCA Citi Mortgage Complaint-In-InterventionjodiebrittNo ratings yet

- Citigroup Whistle-Blower Says Bank's Brute Force' Hid Bad Loans From U.SDocument5 pagesCitigroup Whistle-Blower Says Bank's Brute Force' Hid Bad Loans From U.SCarrieonicNo ratings yet

- r01c 079901Document522 pagesr01c 079901CarrieonicNo ratings yet

- FHFA V Citigroup Inc. (09-02-11)Document95 pagesFHFA V Citigroup Inc. (09-02-11)Master ChiefNo ratings yet

- In RE CitiGroup Inc Securities Litigation 1Document547 pagesIn RE CitiGroup Inc Securities Litigation 1CarrieonicNo ratings yet

- Subsidiarys of Citigroup Inc. 2009 Exhibit21-01Document5 pagesSubsidiarys of Citigroup Inc. 2009 Exhibit21-01CarrieonicNo ratings yet

- Bloomberg Markets Magazine - Citifraud July 2012Document10 pagesBloomberg Markets Magazine - Citifraud July 2012CarrieonicNo ratings yet

- Citi V SMITH WDocument4 pagesCiti V SMITH WCarrieonicNo ratings yet

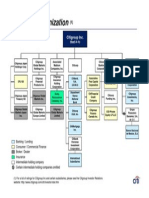

- Corp Struct CitigroupDocument1 pageCorp Struct CitigroupCarrieonicNo ratings yet

- Citi Subsidiarys 2010 Exhibit 21-01Document4 pagesCiti Subsidiarys 2010 Exhibit 21-01CarrieonicNo ratings yet

- Citi Portfolio CorpDocument2 pagesCiti Portfolio CorpCarrieonicNo ratings yet

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5795)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Legalresearchmemorandum SampleDocument2 pagesLegalresearchmemorandum SampleYan Lean Dollison100% (1)

- Suicide - Attempt To Commit Suicide - Abetting SuicideDocument18 pagesSuicide - Attempt To Commit Suicide - Abetting SuicideniravmodyNo ratings yet

- ICMC vs. CallejaDocument2 pagesICMC vs. CallejaJustin Jeric M. IsidoroNo ratings yet

- Security For Keeping The Peace and For Good Behaviour (S.106-124) Copywrite By:-Dr. P. K. ShuklaDocument26 pagesSecurity For Keeping The Peace and For Good Behaviour (S.106-124) Copywrite By:-Dr. P. K. ShuklaAkshay Sarjan100% (5)

- Clayton v. United States of America - Document No. 2Document3 pagesClayton v. United States of America - Document No. 2Justia.comNo ratings yet

- Assign Crimrev Feb 12 2019Document183 pagesAssign Crimrev Feb 12 2019Rolly AcunaNo ratings yet

- People v. Borromeo, GR. No. L-61873, October 31, 1984Document1 pagePeople v. Borromeo, GR. No. L-61873, October 31, 1984MonicaCelineCaroNo ratings yet

- United States v. David Monahan, 633 F.2d 984, 1st Cir. (1980)Document2 pagesUnited States v. David Monahan, 633 F.2d 984, 1st Cir. (1980)Scribd Government DocsNo ratings yet

- International Business - Sri Lanka - Country AssignmentDocument98 pagesInternational Business - Sri Lanka - Country AssignmentDinesh ShamnaniNo ratings yet

- Case Digest TemplateDocument17 pagesCase Digest TemplateStephen ParaisoNo ratings yet

- Hollinger 1 Running Head: MemorandumDocument4 pagesHollinger 1 Running Head: Memorandumdmiller_hollingerNo ratings yet

- Adez Realty, Incorporated vs. Court of AppealsDocument2 pagesAdez Realty, Incorporated vs. Court of AppealsPer-Vito DansNo ratings yet

- LZK Holdings and Development Corporation Vs Planters Development BankDocument2 pagesLZK Holdings and Development Corporation Vs Planters Development BankThomas Vincent O. PantaleonNo ratings yet

- Kevin Patricio-Damian, A061 342 980 (BIA Oct. 27, 2015)Document8 pagesKevin Patricio-Damian, A061 342 980 (BIA Oct. 27, 2015)Immigrant & Refugee Appellate Center, LLCNo ratings yet

- Nego LawwwDocument76 pagesNego LawwwLeeNo ratings yet

- Judgement Gpa Not Valid TitleDocument7 pagesJudgement Gpa Not Valid TitleSanjay SandhuNo ratings yet

- Republic of The Philippines Manila: Gutierrez v. Collector G.R. Nos. L-9738 and L-9771Document7 pagesRepublic of The Philippines Manila: Gutierrez v. Collector G.R. Nos. L-9738 and L-9771Jopan SJ100% (1)

- 2018 Last Minute Tips in Political LawDocument31 pages2018 Last Minute Tips in Political LawGeorge AngelesNo ratings yet

- 02 Chittick Vs CADocument5 pages02 Chittick Vs CAArkhaye SalvatoreNo ratings yet

- Motion For Summary JudgmentDocument11 pagesMotion For Summary JudgmentDodd Harris100% (3)

- 29 Golden Donuts V NLRCDocument2 pages29 Golden Donuts V NLRCAlexis Ailex Villamor Jr.No ratings yet

- People of The State of Illinois v. Nationwide Title Clearing, Inc. 2012-CH-03602 - DocketDocument10 pagesPeople of The State of Illinois v. Nationwide Title Clearing, Inc. 2012-CH-03602 - Docketlarry-612445No ratings yet

- The United States of America v. Russell Decicco, Rene Decicco, Louis Markus and Gregory Parness, 435 F.2d 478, 2d Cir. (1970)Document13 pagesThe United States of America v. Russell Decicco, Rene Decicco, Louis Markus and Gregory Parness, 435 F.2d 478, 2d Cir. (1970)Scribd Government DocsNo ratings yet

- Report248 - Law Commission of India Recommends Repeal of 72 LawsDocument158 pagesReport248 - Law Commission of India Recommends Repeal of 72 LawsLive LawNo ratings yet

- Cases For Wills and Succession CompilationDocument113 pagesCases For Wills and Succession CompilationRaffy LopezNo ratings yet

- WACK WACK v. LEE E. WONDocument4 pagesWACK WACK v. LEE E. WONIsabela IñigoNo ratings yet

- 27 Llorente V CA - Governing LawDocument2 pages27 Llorente V CA - Governing LawDonvidachiye Liwag CenaNo ratings yet

- United States v. Kamara-Reid, 4th Cir. (2001)Document3 pagesUnited States v. Kamara-Reid, 4th Cir. (2001)Scribd Government DocsNo ratings yet

- United States v. Alexander Bortnovsky, A/K/A "Sasha," and Leonid Braz, 879 F.2d 30, 2d Cir. (1989)Document19 pagesUnited States v. Alexander Bortnovsky, A/K/A "Sasha," and Leonid Braz, 879 F.2d 30, 2d Cir. (1989)Scribd Government DocsNo ratings yet

- Interpretivist TheoryDocument14 pagesInterpretivist TheoryPaul Valeros100% (1)