You might also like

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5813)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (844)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (348)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1092)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- What Is White Supremacy Martinez PDFDocument6 pagesWhat Is White Supremacy Martinez PDFshivadogNo ratings yet

- Principles of Economics 7th Edition Frank Solutions ManualDocument18 pagesPrinciples of Economics 7th Edition Frank Solutions ManualEdwardBishopacsy100% (39)

- ResearchDocument14 pagesResearchJohnBanda100% (1)

- China - Legal Growing Pains in A Land of OpportunityDocument9 pagesChina - Legal Growing Pains in A Land of OpportunityManisha TripathyNo ratings yet

- Solution Manual For Managerial Accounting 5th Edition by JiambalvoDocument12 pagesSolution Manual For Managerial Accounting 5th Edition by Jiambalvoa129714627No ratings yet

- The Exchange Rate - A-Level EconomicsDocument13 pagesThe Exchange Rate - A-Level EconomicsjannerickNo ratings yet

- Advanced Banking Bank Runs Exercise SolutionsDocument7 pagesAdvanced Banking Bank Runs Exercise Solutions吳悅寧No ratings yet

- Warrant Buffet: Investment StrategyDocument16 pagesWarrant Buffet: Investment StrategyYassir SlaouiNo ratings yet

- What Is Protectionism?Document7 pagesWhat Is Protectionism?jannerickNo ratings yet

- Doha Talks - The EconomistDocument3 pagesDoha Talks - The EconomistjannerickNo ratings yet

- The Economic Cycle - A-Level EconomicsDocument11 pagesThe Economic Cycle - A-Level EconomicsjannerickNo ratings yet

- Credit Agencies Criticised - BBCDocument2 pagesCredit Agencies Criticised - BBCjannerickNo ratings yet

- The Balance of Payments - A Level EconomicsDocument10 pagesThe Balance of Payments - A Level EconomicsjannerickNo ratings yet

- Flexible Labour Markets - A Level EconomicsDocument3 pagesFlexible Labour Markets - A Level EconomicsjannerickNo ratings yet

- Globalisation - A-Level EconomicsDocument15 pagesGlobalisation - A-Level EconomicsjannerickNo ratings yet

- 2019-20 S.Y. B.Com. (CBCS)Document55 pages2019-20 S.Y. B.Com. (CBCS)ASdfNo ratings yet

- Viner Cost Curves and Supply CurvesDocument25 pagesViner Cost Curves and Supply CurvesZenobio FarfNo ratings yet

- Sob June 2023 Supplementary Special Exam TTDocument16 pagesSob June 2023 Supplementary Special Exam TTSarah MuthoniNo ratings yet

- một số câu hỏi bài tập tiếng anhDocument21 pagesmột số câu hỏi bài tập tiếng anhNam chính Chị củaNo ratings yet

- DC 1st Year SyllabusDocument9 pagesDC 1st Year SyllabusRectify TechNo ratings yet

- This Is A Sample Trading Plan For Educational Purposes OnlyDocument6 pagesThis Is A Sample Trading Plan For Educational Purposes OnlyJamican PrasadNo ratings yet

- Revised Supplementary Material Semester 2 2013Document98 pagesRevised Supplementary Material Semester 2 2013HeoHamHốNo ratings yet

- Chapter 6-Firm and IntegrationDocument10 pagesChapter 6-Firm and IntegrationUyển Nhi Lê ĐoànNo ratings yet

- Role of International Marketing in Economic DevelopmentDocument12 pagesRole of International Marketing in Economic DevelopmentAdnan ChaudhryNo ratings yet

- Chapter 31 - Indifference Curves and Budget LinesDocument22 pagesChapter 31 - Indifference Curves and Budget LinesPhuong DaoNo ratings yet

- Role of FDI in Indian EconomyDocument16 pagesRole of FDI in Indian EconomyAnna Anjana VargheseNo ratings yet

- Market StructureDocument3 pagesMarket StructureSonwabo MgciyoNo ratings yet

- Mid-Essay IE 124109Document6 pagesMid-Essay IE 124109Alexandra BragaNo ratings yet

- Computational IntelligenceDocument54 pagesComputational Intelligencebogdan.oancea3651No ratings yet

- Book Review of "E-Gov 2.0"Document2 pagesBook Review of "E-Gov 2.0"SiberianVillageNo ratings yet

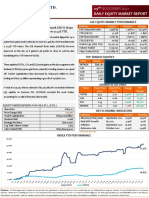

- Daily Equity Market Report - 09.11.2021Document1 pageDaily Equity Market Report - 09.11.2021Fuaad DodooNo ratings yet

- Theoritical Market PriceDocument3 pagesTheoritical Market PriceJNo ratings yet

- Daniel Diaz Vidal CVDocument5 pagesDaniel Diaz Vidal CVapi-239095261No ratings yet

- Blue Print of Economics PDFDocument2 pagesBlue Print of Economics PDFRushender kaur bhullarNo ratings yet

- Use The Table Below To Answer The Following QuestionDocument9 pagesUse The Table Below To Answer The Following QuestionexamkillerNo ratings yet

- Economics - Law of Diminishing Marginal Utility PDFDocument5 pagesEconomics - Law of Diminishing Marginal Utility PDFabhaybittu100% (2)

- Tata Steel Share AnalysisDocument9 pagesTata Steel Share AnalysisArchit JainNo ratings yet

- The New Institutionalisms in Economics and SociologyDocument27 pagesThe New Institutionalisms in Economics and Sociologymam1No ratings yet