You might also like

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Kartu NamaDocument1 pageKartu NamaRe ZhaNo ratings yet

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Soal Uts AuditDocument1 pageSoal Uts AuditRe ZhaNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- 481 958 1 SMDocument1 page481 958 1 SMRe ZhaNo ratings yet

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Kartu NamaDocument1 pageKartu NamaRe ZhaNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Specific Determinants of Work Motivation, Competence, Organizational Climate, Job Satisfaction and Individual Performance: A Study Among LecturersDocument7 pagesSpecific Determinants of Work Motivation, Competence, Organizational Climate, Job Satisfaction and Individual Performance: A Study Among LecturersRe ZhaNo ratings yet

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Caq Icfr 042513 PDFDocument16 pagesCaq Icfr 042513 PDFRe ZhaNo ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Content ServerDocument17 pagesContent ServerRe ZhaNo ratings yet

- The Control Environment of A Company - ACCA Qualification - Students - ACCA GlobalDocument4 pagesThe Control Environment of A Company - ACCA Qualification - Students - ACCA GlobalRe ZhaNo ratings yet

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- THE Effect OF Work Discipline AND Work Environment ON THE Performance OF EmployeesDocument15 pagesTHE Effect OF Work Discipline AND Work Environment ON THE Performance OF EmployeesRe ZhaNo ratings yet

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Tanjungpura University Bachelor's Degree in EconomicsDocument1 pageTanjungpura University Bachelor's Degree in EconomicsRe ZhaNo ratings yet

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Hypothesis Testing WorksheetDocument2 pagesHypothesis Testing WorksheetRe ZhaNo ratings yet

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Materi Akuntansi Manajemen LanjutanDocument4 pagesMateri Akuntansi Manajemen LanjutanRe ZhaNo ratings yet

- Fair Value Disclosure, External Appraisers, and The Reliability of Fair Value MeasurementsDocument16 pagesFair Value Disclosure, External Appraisers, and The Reliability of Fair Value MeasurementsRe ZhaNo ratings yet

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- An Introduction To Literature ReviewsDocument9 pagesAn Introduction To Literature ReviewslynxhillNo ratings yet

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- PresentationDocument1 pagePresentationRe ZhaNo ratings yet

- Tanjungpura University Bachelor's Degree in EconomicsDocument1 pageTanjungpura University Bachelor's Degree in EconomicsRe ZhaNo ratings yet

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- ADocument1 pageARe ZhaNo ratings yet

- AvDocument1 pageAvRe ZhaNo ratings yet

- Financial Crisis and The Silence of The AuditorsDocument6 pagesFinancial Crisis and The Silence of The AuditorsRe ZhaNo ratings yet

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- 42 365 1 PBDocument24 pages42 365 1 PBRe ZhaNo ratings yet

- Clikeman Greatest FraudsDocument8 pagesClikeman Greatest FraudsRe ZhaNo ratings yet

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- Corporate Governance & Business EthicsDocument21 pagesCorporate Governance & Business EthicspriyankaNo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Doctor Naveed Iqbal C.VDocument14 pagesDoctor Naveed Iqbal C.Vفیضان علیNo ratings yet

- Lecture 10 Cash and Internal Controls - NUS ACC1002 2020 SpringDocument24 pagesLecture 10 Cash and Internal Controls - NUS ACC1002 2020 SpringZenyuiNo ratings yet

- Assignment 3Document13 pagesAssignment 3Hamsa VahiniNo ratings yet

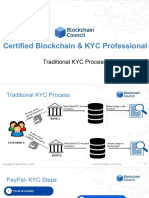

- Traditional KYC Process PDFDocument5 pagesTraditional KYC Process PDFvivxtractNo ratings yet

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

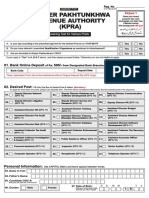

- Khyber Pakhtunkhwa Revenue Authority (KPRA) : Eligibility CriteriaDocument5 pagesKhyber Pakhtunkhwa Revenue Authority (KPRA) : Eligibility CriteriaFaisal AyazNo ratings yet

- MD50 - Sales Order Invoice For Another OUDocument14 pagesMD50 - Sales Order Invoice For Another OUVenkat Nkb100% (5)

- A. 1B Problem 7Document1 pageA. 1B Problem 7shuzoNo ratings yet

- Managing Early Growth Strategies & IssuesDocument13 pagesManaging Early Growth Strategies & IssuesDhananjay Parshuram SawantNo ratings yet

- CMCP Chap 13Document2 pagesCMCP Chap 13Kei SenpaiNo ratings yet

- Mrunal EconomyDocument19 pagesMrunal EconomyJeevan KumarNo ratings yet

- China Case StudyDocument10 pagesChina Case StudyAlvi100% (1)

- Factors Influencing Life Insurance ChoiceDocument199 pagesFactors Influencing Life Insurance ChoiceVenkat GVNo ratings yet

- 1 s2.0 S1042443123000690 MainDocument17 pages1 s2.0 S1042443123000690 MainOumema AL AZHARNo ratings yet

- Bajaj Finserv Limited - Leading Indian Financial Services CompanyDocument3 pagesBajaj Finserv Limited - Leading Indian Financial Services CompanySanam TNo ratings yet

- Export Import Process DocumentationDocument13 pagesExport Import Process Documentationgarganurag12No ratings yet

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Asset Based FinancingDocument64 pagesAsset Based FinancingChintan Shah100% (1)

- 208 - Umer - What Ails The MSME Sector in India Is It Poor Access To FundsDocument7 pages208 - Umer - What Ails The MSME Sector in India Is It Poor Access To FundsnomadisnoNo ratings yet

- QB IiiDocument33 pagesQB IiisaketramaNo ratings yet

- Mudharabah 2Document4 pagesMudharabah 2Hairizal HarunNo ratings yet

- Divine Education Hub Sandeep Choudhary: Mathematics & Reasoning Faculty MOBILE NO.-96492-03888Document9 pagesDivine Education Hub Sandeep Choudhary: Mathematics & Reasoning Faculty MOBILE NO.-96492-03888Prabha KaranNo ratings yet

- CPS Report-Aditya SoodDocument20 pagesCPS Report-Aditya SoodMadhav JhaNo ratings yet

- APA Jamii Plus Family Medical Cover BrochureDocument8 pagesAPA Jamii Plus Family Medical Cover BrochureADANARABOW100% (1)

- Negotiable Instruments Law DigestDocument83 pagesNegotiable Instruments Law DigestCha100% (2)

- Different Types of Investments: What Is An 'Investment'Document8 pagesDifferent Types of Investments: What Is An 'Investment'Anonymous oLTidvNo ratings yet

- Duties of Banker Towards His CoustomerDocument24 pagesDuties of Banker Towards His CoustomerAakashsharma0% (2)

- 2015-03-261427365719new Version of Accountancy Module - CDocument46 pages2015-03-261427365719new Version of Accountancy Module - CRamachandran MNo ratings yet

- FINMAR Final Term Money Market Instruments Part IDocument7 pagesFINMAR Final Term Money Market Instruments Part IMark Angelo BustosNo ratings yet

- A Project Report of Indian Financial System On Role of Rbi in Indian EconomyDocument14 pagesA Project Report of Indian Financial System On Role of Rbi in Indian EconomyAjay Gupta67% (3)

- Summer internship in Greenply's plywood and laminates businessDocument16 pagesSummer internship in Greenply's plywood and laminates businessVanshika MaheswaryNo ratings yet