You might also like

- The Indian Tractor Industry - Bumpy Road AheadDocument3 pagesThe Indian Tractor Industry - Bumpy Road AheadSanjana AcharyaNo ratings yet

- Tractors Article Sep14Document7 pagesTractors Article Sep14Abhinav WaliaNo ratings yet

- PWC Insurance BrokerageDocument28 pagesPWC Insurance BrokerageAbhinav Walia100% (1)

- Challenges: Need One Bank Licensing Policy, But Several Bank LicensingpoliciesDocument8 pagesChallenges: Need One Bank Licensing Policy, But Several Bank LicensingpoliciesAbhinav WaliaNo ratings yet

- SB Whitepaper AutomotivecrmDocument8 pagesSB Whitepaper AutomotivecrmAbhinav WaliaNo ratings yet

- Small To Big Marketing Makes It Possible: The Basics of Rural MarketingDocument2 pagesSmall To Big Marketing Makes It Possible: The Basics of Rural MarketingAbhinav WaliaNo ratings yet

- ContentServer - 3 COMPANY PROFILE Escorts Limited 2014Document9 pagesContentServer - 3 COMPANY PROFILE Escorts Limited 2014Abhinav WaliaNo ratings yet

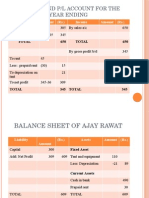

- Trading and P/L Account For The Year Ending: Expense Amount (RS.) Income Amount (RS.)Document2 pagesTrading and P/L Account For The Year Ending: Expense Amount (RS.) Income Amount (RS.)Abhinav WaliaNo ratings yet

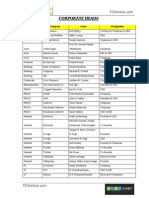

- Corporate Heads: Industry Company Name DesignationDocument2 pagesCorporate Heads: Industry Company Name DesignationAbhinav WaliaNo ratings yet

- Corporate PresentationDocument45 pagesCorporate PresentationAbhinav WaliaNo ratings yet

- Britannia Nutrichoice Case StudyDocument18 pagesBritannia Nutrichoice Case StudyAbhinav WaliaNo ratings yet

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Sofpo Report (06!07!22) Hi-Res WCMDocument190 pagesSofpo Report (06!07!22) Hi-Res WCMabhishek mandingiNo ratings yet

- Process of Registration and Accreditation of Agricultural Extension Service ProvidersDocument28 pagesProcess of Registration and Accreditation of Agricultural Extension Service Providersnicholas ssebalamu100% (1)

- Burundi EconomyDocument112 pagesBurundi EconomyMandar RasaikarNo ratings yet

- Dattabot GE Predix Case StudyDocument9 pagesDattabot GE Predix Case StudyKai SanNo ratings yet

- Postharvest Technology 1 1Document56 pagesPostharvest Technology 1 1Jr AquinoNo ratings yet

- Pids Ar 2020Document120 pagesPids Ar 2020bEVERLY SALAZARNo ratings yet

- Acceptance SpeechDocument31 pagesAcceptance SpeechJohn Richard Kasalika100% (1)

- Agriculture Value ChainDocument10 pagesAgriculture Value ChainYahaya LwindeNo ratings yet

- Agricultural Value Chain Financing AVCF and Development For Enhanced Export CompetitivenessDocument136 pagesAgricultural Value Chain Financing AVCF and Development For Enhanced Export CompetitivenessAndrew OseniNo ratings yet

- Miller - Value ChainDocument64 pagesMiller - Value ChainAkash GuptaNo ratings yet

- Climate Change and Food Security Status in UgandaDocument11 pagesClimate Change and Food Security Status in UgandaSteven SenabulyaNo ratings yet

- Vodafone PNG - Case Study by Issac McWillaims R. KakarayaDocument24 pagesVodafone PNG - Case Study by Issac McWillaims R. KakarayaIssac McWilliams R. KakarayaNo ratings yet

- Agrobased ClustersDocument118 pagesAgrobased ClustersWebley SkoutNo ratings yet

- Agribussiness Incubation and TT ReviewDocument16 pagesAgribussiness Incubation and TT ReviewYared FikaduNo ratings yet

- Opportunities in Agricultural Value Chain Digitisation: Learnings From GhanaDocument32 pagesOpportunities in Agricultural Value Chain Digitisation: Learnings From GhanaKuuku SamNo ratings yet

- Thesis AgribusinessDocument5 pagesThesis AgribusinessElizabeth Williams100% (2)

- Financing For Farmer Producer Organisations PDFDocument18 pagesFinancing For Farmer Producer Organisations PDFRaghuram BhallamudiNo ratings yet

- 1.3 Basics of Value Chain Financing-V1Document33 pages1.3 Basics of Value Chain Financing-V1សរ ឧត្តមNo ratings yet

- Entrepreneurship and Entrepreneurial Opportunities in The Food Value ChainDocument5 pagesEntrepreneurship and Entrepreneurial Opportunities in The Food Value ChainELVIS KOKANo ratings yet

- ADB - Op5-Rural-Development-And-Food-Security-FinalDocument30 pagesADB - Op5-Rural-Development-And-Food-Security-FinalFaris DzulfikarNo ratings yet

- Research Statement (Masters Thesis and PHD)Document5 pagesResearch Statement (Masters Thesis and PHD)Anoosha HabibNo ratings yet

- Agriculture Value Chain Financing in IndiaDocument7 pagesAgriculture Value Chain Financing in Indiaraggarwal101No ratings yet

- A Report On The Study of Onion Value ChainDocument51 pagesA Report On The Study of Onion Value Chainreny shah100% (1)

- The Use of ICT in Agricultural Value Chains To Improve Food Security - An International Perspective-Leisa Armstrong, Dean Ms Niketa GandhiDocument8 pagesThe Use of ICT in Agricultural Value Chains To Improve Food Security - An International Perspective-Leisa Armstrong, Dean Ms Niketa GandhieletsonlineNo ratings yet

- Challenges in Agribusiness in NigeriaDocument3 pagesChallenges in Agribusiness in NigeriaTomilola Odejayi Balogun50% (2)

- The Evolution of Rural Development Policies in EthiopiaDocument33 pagesThe Evolution of Rural Development Policies in EthiopiayaregalNo ratings yet

- Managing Agricultural Commercialization For Inclusive Growth in Sub-Saharan AfricaDocument8 pagesManaging Agricultural Commercialization For Inclusive Growth in Sub-Saharan AfricaAgripolicyoutreachNo ratings yet

- WP AFR Digital Access The Future of Financial Inclusion in Africa PUBLICDocument97 pagesWP AFR Digital Access The Future of Financial Inclusion in Africa PUBLICZach LeulNo ratings yet

- Digital Agriculture Strategy NDAS in Review - CleanDocument58 pagesDigital Agriculture Strategy NDAS in Review - CleanHassan KhalilNo ratings yet

- Value Chain Anlysis & Development 3,4&5 PPDocument102 pagesValue Chain Anlysis & Development 3,4&5 PPLemma Deme ResearcherNo ratings yet