You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5814)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1092)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (844)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (897)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (348)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- итоговое заданиеDocument2 pagesитоговое заданиеOlga Kukhtina100% (1)

- Calamba - RPT PDFDocument12 pagesCalamba - RPT PDFJela OasinNo ratings yet

- Pasig Revenue Code PDFDocument295 pagesPasig Revenue Code PDFJela Oasin33% (9)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

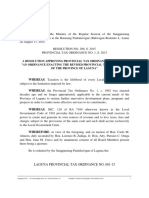

- Laguna Revenue Code PDFDocument91 pagesLaguna Revenue Code PDFJela OasinNo ratings yet

- Sonnet 307Document1 pageSonnet 307Jela OasinNo ratings yet

- Sonnet 307Document1 pageSonnet 307Jela OasinNo ratings yet

- CH1 HbotbDocument7 pagesCH1 HbotbJela OasinNo ratings yet

- 34 Ms Surgery LogbookDocument111 pages34 Ms Surgery LogbookMohamedHossam50% (2)

- Demand Forecasting QuestionsDocument30 pagesDemand Forecasting QuestionsgigipapasNo ratings yet

- Manila PDFDocument17 pagesManila PDFJela OasinNo ratings yet

- RR No. 14-12 PDFDocument9 pagesRR No. 14-12 PDFJela OasinNo ratings yet

- Risks and ControlsDocument43 pagesRisks and ControlsJela Oasin100% (1)

- Second Division: Republic of The Philippines Court of Tax Appeals Quezon CityDocument50 pagesSecond Division: Republic of The Philippines Court of Tax Appeals Quezon CityJela OasinNo ratings yet

- BIR Ruling No. 059-97Document2 pagesBIR Ruling No. 059-97Jela OasinNo ratings yet

- IntroDocument24 pagesIntroJela OasinNo ratings yet

- Cebu Revenue Code PDFDocument9 pagesCebu Revenue Code PDFJela Oasin0% (1)

- StemsDocument2 pagesStemsJela OasinNo ratings yet

- Petitioner vs. vs. Respondents Bayani L. Bernardo Lucas C. Carpio, JR Danilo B BenaresDocument16 pagesPetitioner vs. vs. Respondents Bayani L. Bernardo Lucas C. Carpio, JR Danilo B BenaresJela OasinNo ratings yet

- Logic ScriptDocument3 pagesLogic ScriptJela OasinNo ratings yet

- Zoology 100 Notes 1Document8 pagesZoology 100 Notes 1Bethany Jane Ravelo IsidroNo ratings yet

- Brother Mfc-9420cn PartsDocument34 pagesBrother Mfc-9420cn PartsNikolaos MavridisNo ratings yet

- Dylos Conversion Education - Cehs.health - Umt.eduDocument117 pagesDylos Conversion Education - Cehs.health - Umt.eduMCNo ratings yet

- 2016 Specimen Paper 2 Mark Scheme PDFDocument2 pages2016 Specimen Paper 2 Mark Scheme PDFAsad ZamanNo ratings yet

- Assignments MOSDocument4 pagesAssignments MOSRajeev RanaNo ratings yet

- Fillers Adaptations On Traditional and CDocument10 pagesFillers Adaptations On Traditional and CMaja SMNo ratings yet

- Fishing in The Roman WorldDocument69 pagesFishing in The Roman Worldmnm06100% (1)

- The Night FloorsDocument57 pagesThe Night FloorsNat LinkenNo ratings yet

- Chapter Two Approaches To Ethics: Ayenew Birhanu (PHD)Document43 pagesChapter Two Approaches To Ethics: Ayenew Birhanu (PHD)Nasri IBRAHIMNo ratings yet

- Assignment 2 & 3 - PeaDocument3 pagesAssignment 2 & 3 - PeaShehzad khanNo ratings yet

- Generator ProtectionDocument10 pagesGenerator ProtectionSriram rams100% (1)

- Sequence Based SpecificationsDocument11 pagesSequence Based SpecificationsrexthrottleNo ratings yet

- Guide Droping Point MethodologyDocument44 pagesGuide Droping Point MethodologyFrankPapaNo ratings yet

- External Commands of Dos With Syntax PDFDocument2 pagesExternal Commands of Dos With Syntax PDFCekap100% (2)

- Career Essay Eng 1302Document4 pagesCareer Essay Eng 1302Madison MorenoNo ratings yet

- Machine Learning Classification Model For Identifying Wildlife Species in East AfricaDocument9 pagesMachine Learning Classification Model For Identifying Wildlife Species in East AfricaInternational Journal of Innovative Science and Research TechnologyNo ratings yet

- PipeChart Trupply 2015 PDFDocument2 pagesPipeChart Trupply 2015 PDFDeepak PatilNo ratings yet

- Mead's Theory of The SelfDocument1 pageMead's Theory of The Selfsumayya tariqNo ratings yet

- 3483-Article Text-8498-2-10-20201015Document15 pages3483-Article Text-8498-2-10-20201015Nawzi kagimboNo ratings yet

- Central Mosque Northampton: 112 116. Abington Avenue Abington, Northampton Nn1 4PdDocument1 pageCentral Mosque Northampton: 112 116. Abington Avenue Abington, Northampton Nn1 4PdAshraf OsmaniNo ratings yet

- Pharmacognosy - Lab-ManualDocument28 pagesPharmacognosy - Lab-ManualHarish KakraniNo ratings yet

- Tivoli MessagesDocument851 pagesTivoli Messagesjackiexie3813No ratings yet

- Lyrics BLOODY MARYDocument1 pageLyrics BLOODY MARYMuhd Baqir AzidzNo ratings yet

- Implementing Sales 12Document566 pagesImplementing Sales 12Amer YehiaNo ratings yet

- Nama: Selma Selyvia Kelas: X1-Keperawatan No: 28Document3 pagesNama: Selma Selyvia Kelas: X1-Keperawatan No: 28Selma SelyviaNo ratings yet

- Resultant of Concurrent Force System - Engineering Mechanics ReviewDocument2 pagesResultant of Concurrent Force System - Engineering Mechanics Reviewimrancenakk0% (2)

- End Closure of Pressure VesselDocument11 pagesEnd Closure of Pressure VesselYl WongNo ratings yet