You might also like

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

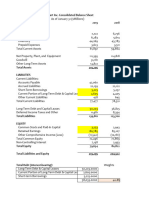

- Bestbuy Financial AnalysisDocument11 pagesBestbuy Financial AnalysisGPA FOURNo ratings yet

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- 02, Accounting & Financial Analysis: 13, Preparation of Profit and Loss Accounts Loss AccountDocument14 pages02, Accounting & Financial Analysis: 13, Preparation of Profit and Loss Accounts Loss AccountHOD Dept of BBA Vels UniversityNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5795)

- Chapter 7-The Revenue/Receivables/Cash Cycle: Multiple ChoiceDocument32 pagesChapter 7-The Revenue/Receivables/Cash Cycle: Multiple ChoiceLeonardoNo ratings yet

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Acc 6 CH 01Document46 pagesAcc 6 CH 01Md. Rubel HasanNo ratings yet

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- E3.5 Devin Wolf Company: Adjusting EntriesDocument2 pagesE3.5 Devin Wolf Company: Adjusting EntriesKhôi NguyễnNo ratings yet

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- 2cp Ce 23Document12 pages2cp Ce 23rodrigoNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Q4 2017 Eng ORG PDFDocument16 pagesQ4 2017 Eng ORG PDFAnonymous 6tuR1hzNo ratings yet

- Part-2 Cash Flow Apex Footwear Limited Growth RateDocument11 pagesPart-2 Cash Flow Apex Footwear Limited Growth RateRizwanul Islam 1912111630No ratings yet

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- B-MGAC203 Long QuizDocument6 pagesB-MGAC203 Long QuizMa. Yelena Italia TalabocNo ratings yet

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Balance Sheet of InfosysDocument2 pagesBalance Sheet of InfosysSamta SukhdeveNo ratings yet

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Debit Credit: EGG SHERAN Corp. (Home Office) Unadjusted Trial Balance December 31,20x1Document6 pagesDebit Credit: EGG SHERAN Corp. (Home Office) Unadjusted Trial Balance December 31,20x1Riza Mae AlceNo ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- UzAuto Motors JSC Financial ReportsDocument28 pagesUzAuto Motors JSC Financial Reportsid00001875No ratings yet

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- اسئلة اقتصادية باللغة الانجليزيةDocument5 pagesاسئلة اقتصادية باللغة الانجليزيةMoun DirNo ratings yet

- Excel Sheet Ratio AnalysisDocument5 pagesExcel Sheet Ratio AnalysisTajalli FatimaNo ratings yet

- S.Y.J.C. (Commerce) Book-Kkeping & Accoutancy Partnership Final Accounts Compiled By: Prof. Bosco FernandesDocument11 pagesS.Y.J.C. (Commerce) Book-Kkeping & Accoutancy Partnership Final Accounts Compiled By: Prof. Bosco FernandesDheer BhanushaliNo ratings yet

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Chapter 4 Test BankDocument21 pagesChapter 4 Test BankMohamed Diab100% (1)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- ch04 Completing The Accounting Cycle - StudentDocument13 pagesch04 Completing The Accounting Cycle - StudentTâm Vũ NhậtNo ratings yet

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Assignment/ TugasanDocument21 pagesAssignment/ Tugasanhafiz azuanNo ratings yet

- ACC 100 - Chapter 4 - Financial StatementsDocument4 pagesACC 100 - Chapter 4 - Financial StatementsTasnim SheikhNo ratings yet

- Cash Flows ExercicesDocument96 pagesCash Flows ExercicesAbdelmajid JamaneNo ratings yet

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- TuriDocument3 pagesTuriDedy SuyetnoNo ratings yet

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1091)

- Anureev TestDocument49 pagesAnureev TestНиколай Илиаев80% (5)

- Hitesh Sir Bba Sem 2-1Document25 pagesHitesh Sir Bba Sem 2-1Rohit SharmaNo ratings yet

- Suport Curs 13Document11 pagesSuport Curs 13Sorin GabrielNo ratings yet

- Topic 7 OF ACCONTINGDocument11 pagesTopic 7 OF ACCONTINGCharlesNo ratings yet

- Instruction: Prepare The Answers in Written Form Using A Clean Paper (E.g. Yellow Pad, Bond Paper, Notebook Etc.) and Submit A Snapshot in CANVASDocument2 pagesInstruction: Prepare The Answers in Written Form Using A Clean Paper (E.g. Yellow Pad, Bond Paper, Notebook Etc.) and Submit A Snapshot in CANVASKristine Lirose BordeosNo ratings yet

- ch07 SM Carlon 5eDocument39 pagesch07 SM Carlon 5eKyle100% (1)

- Answer Keys Assignment IDocument3 pagesAnswer Keys Assignment IAshutosh SinghNo ratings yet

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Ratio AnalysisDocument27 pagesRatio AnalysisPratik Thorat100% (1)

- Government GrantsDocument9 pagesGovernment Grantssorin8488100% (1)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)