You might also like

- RatioDocument4 pagesRatioMd Junayed IslamNo ratings yet

- FIN-5823 - Financial Analysis ExampleDocument15 pagesFIN-5823 - Financial Analysis ExampleGPA FOURNo ratings yet

- Suzuki Motors (AutoRecovered)Document8 pagesSuzuki Motors (AutoRecovered)AIOU Fast AcademyNo ratings yet

- Front Valuation Page: Un-Levered Firm ValueDocument61 pagesFront Valuation Page: Un-Levered Firm Valueneelakanta srikar100% (1)

- Case Submission On: Mellon Financial and The Bank of New YorkDocument3 pagesCase Submission On: Mellon Financial and The Bank of New Yorkneelakanta srikarNo ratings yet

- HorizontalDocument4 pagesHorizontal30 Odicta, Justine AnneNo ratings yet

- SAPM Assignment: Company: Ashok Leyland Student Name and PRNDocument15 pagesSAPM Assignment: Company: Ashok Leyland Student Name and PRNAkshat JainNo ratings yet

- Small Bank Pro Forma Model: Balance Sheets Thousand $Document5 pagesSmall Bank Pro Forma Model: Balance Sheets Thousand $jam7ak3275No ratings yet

- Particulars (All Values in Lakhs Unless Specified Otherwise) 2019 2018Document6 pagesParticulars (All Values in Lakhs Unless Specified Otherwise) 2019 2018MOHIT MARHATTANo ratings yet

- 1 800 Flowers Com. Financial Statements EJ 1Document28 pages1 800 Flowers Com. Financial Statements EJ 1PuMuK03No ratings yet

- SENEA Financial AnalysisDocument22 pagesSENEA Financial Analysissidrajaffri72No ratings yet

- Managements Discussion Analysis 2022Document111 pagesManagements Discussion Analysis 2022arvind sharmaNo ratings yet

- Income Statement - PEPSICODocument11 pagesIncome Statement - PEPSICOAdriana MartinezNo ratings yet

- Term Valued CFDocument14 pagesTerm Valued CFEl MemmetNo ratings yet

- DCF Guide ExampleDocument4 pagesDCF Guide ExampleAlexander RiosNo ratings yet

- Excel Workings ITE ValuationDocument19 pagesExcel Workings ITE Valuationalka murarka100% (1)

- Steel Authority of India Limited.: Particulars Amt. (In Crore)Document8 pagesSteel Authority of India Limited.: Particulars Amt. (In Crore)1075SYBPATEL DHRUVNo ratings yet

- Competitors Bajaj MotorsDocument11 pagesCompetitors Bajaj MotorsdeepaksikriNo ratings yet

- Asf ExcleDocument6 pagesAsf ExcleAnam AbrarNo ratings yet

- Receivable Breakdown Type of Inventory Amount of Receivable Days Overdue RemarkDocument6 pagesReceivable Breakdown Type of Inventory Amount of Receivable Days Overdue RemarkYonatanNo ratings yet

- AIS Final ReqDocument10 pagesAIS Final ReqSucreNo ratings yet

- Financial TTDocument4 pagesFinancial TTJamilexNo ratings yet

- Colgate Estados Financieros 2021Document3 pagesColgate Estados Financieros 2021Lluvia RamosNo ratings yet

- Samsung RatiosDocument11 pagesSamsung RatiosjunaidNo ratings yet

- MBA5002 Sample Case Study 2Document13 pagesMBA5002 Sample Case Study 2Mohamed NaieemNo ratings yet

- Particular Formulae RatiosDocument13 pagesParticular Formulae RatiosRahul SinghNo ratings yet

- Long-Term Debt Handout (UPDATED 8-27-22)Document9 pagesLong-Term Debt Handout (UPDATED 8-27-22)Charudatta MundeNo ratings yet

- J&J FS AnalysisDocument5 pagesJ&J FS AnalysisEarl Justine FerrerNo ratings yet

- Cash Flow Statement Examples2Document8 pagesCash Flow Statement Examples2ReactorAkkharNo ratings yet

- 16453Document2 pages16453fazal nadeemNo ratings yet

- Basel Disclosure Ashad2080Document4 pagesBasel Disclosure Ashad2080Na Bee NaNo ratings yet

- AscascaDocument9 pagesAscascaDhruba DasNo ratings yet

- Consolidated Balance Sheet Metapower International, IncDocument12 pagesConsolidated Balance Sheet Metapower International, IncJha YaNo ratings yet

- Ain 20201025074Document8 pagesAin 20201025074HAMMADHRNo ratings yet

- Foreign Institutional Investors (FII) : Shareholders (As of 31 December 2015) Promoter Group (HDFC)Document10 pagesForeign Institutional Investors (FII) : Shareholders (As of 31 December 2015) Promoter Group (HDFC)Vinod KananiNo ratings yet

- Financial Reporting Case: What Is It Worth?: Property of STIDocument2 pagesFinancial Reporting Case: What Is It Worth?: Property of STIJoannie Cercado RabiaNo ratings yet

- Financial Statement BICDocument4 pagesFinancial Statement BICQuynh NguyenNo ratings yet

- PTRY AnalysisDocument5 pagesPTRY AnalysisthesaneinvestorNo ratings yet

- 01 ELMS Activity 1Document2 pages01 ELMS Activity 1Emperor SavageNo ratings yet

- Societe Generale Ghana PLC Unaudited Financial Statements For The Quarter Ended 30 September 2021Document2 pagesSociete Generale Ghana PLC Unaudited Financial Statements For The Quarter Ended 30 September 2021Fuaad DodooNo ratings yet

- E I D-Parry (India) LTD.: Balance Sheet Summary: Mar 2011 - Mar 2020: Non-Annualised: Rs. CroreDocument15 pagesE I D-Parry (India) LTD.: Balance Sheet Summary: Mar 2011 - Mar 2020: Non-Annualised: Rs. Crorehardik aroraNo ratings yet

- Balance Sheet: Liquidity Analysis RatiosDocument7 pagesBalance Sheet: Liquidity Analysis RatiosJan OleteNo ratings yet

- Chapter 3. Finance Department 3.1 Essar Steel LTD.: 3.1.1 P&L AccountDocument8 pagesChapter 3. Finance Department 3.1 Essar Steel LTD.: 3.1.1 P&L AccountT.Y.B68PATEL DHRUVNo ratings yet

- Accounting Assignment QuestionDocument14 pagesAccounting Assignment QuestionsureshdassNo ratings yet

- ValuationDocument31 pagesValuationAman TaterNo ratings yet

- Cash Flow Statement Examples3Document3 pagesCash Flow Statement Examples3ReactorAkkharNo ratings yet

- Q3 Financial Statement q3 For Period 30 September 2021Document2 pagesQ3 Financial Statement q3 For Period 30 September 2021Fuaad DodooNo ratings yet

- Farag HWCH 3Document8 pagesFarag HWCH 3drenghalaNo ratings yet

- Assessment 4 Written Assignment Final Zhaoming ZhengDocument4 pagesAssessment 4 Written Assignment Final Zhaoming ZhengNawshin DastagirNo ratings yet

- Elnusa 2019Document3 pagesElnusa 2019Pieri MosesNo ratings yet

- Globe Vertical AnalysisDocument22 pagesGlobe Vertical AnalysisArriana RefugioNo ratings yet

- Bibliography: BooksDocument17 pagesBibliography: BooksshravanigangampalliNo ratings yet

- Bajaj Finance Limited Fra ProjectDocument12 pagesBajaj Finance Limited Fra ProjectSUBASH S 2019No ratings yet

- Byte Back, Inc. FS June 30, 2009Document17 pagesByte Back, Inc. FS June 30, 2009byteback2No ratings yet

- Chapter 3 108-117Document10 pagesChapter 3 108-117Leony SantikaNo ratings yet

- Trident, Inc. Consolidated Balance Sheets: Execonline - Mastering Finance FundamentalsDocument3 pagesTrident, Inc. Consolidated Balance Sheets: Execonline - Mastering Finance Fundamentalschemicalchouhan9303No ratings yet

- Final AnalyticsDocument10 pagesFinal AnalyticsAries BautistaNo ratings yet

- PayTM FinancialsDocument43 pagesPayTM FinancialststNo ratings yet

- Assets: PAYNET, Inc. Consolidated Balance SheetsDocument3 pagesAssets: PAYNET, Inc. Consolidated Balance Sheetschemicalchouhan9303No ratings yet

- Test Bank AISDocument12 pagesTest Bank AISJOCELYN BERDULNo ratings yet

- Final Assignment Strategy Formulation: Sheraz Hassan Mba 1.5 2nd Roll No F-016 - 019 Subject Strategic ManagementDocument9 pagesFinal Assignment Strategy Formulation: Sheraz Hassan Mba 1.5 2nd Roll No F-016 - 019 Subject Strategic ManagementFaisal AwanNo ratings yet

- A Study On Consumer Buying Behaviour in Retail Readymade Garment ShopsDocument2 pagesA Study On Consumer Buying Behaviour in Retail Readymade Garment ShopsATSx room clashNo ratings yet

- Mckinsey-Full Article 25 PDFDocument7 pagesMckinsey-Full Article 25 PDFjcmunevar1484No ratings yet

- Internal Controls Checklist: Yes No Not Sure Not ApplicableDocument5 pagesInternal Controls Checklist: Yes No Not Sure Not Applicableijlal_1100% (1)

- News Just In:: Et 500 CompaniesDocument2 pagesNews Just In:: Et 500 CompaniesAshutosh ApteNo ratings yet

- Event Management For Tourism Cultural Business andDocument13 pagesEvent Management For Tourism Cultural Business andSarthak DasNo ratings yet

- SantiagoDocument3 pagesSantiagoMia Valerie JumanguinNo ratings yet

- Brewin Dolphin - Our-Services-And-Charges-Sept18Document16 pagesBrewin Dolphin - Our-Services-And-Charges-Sept18srowbothamNo ratings yet

- ECO162 - Grab Holdings IncDocument19 pagesECO162 - Grab Holdings Incdewi balqisNo ratings yet

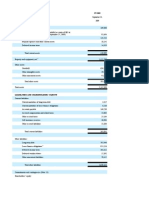

- Financial Reports: Agha Steel Industries LTDDocument33 pagesFinancial Reports: Agha Steel Industries LTDeman shafiqueNo ratings yet

- Zagreb Logistics Park BrochureDocument10 pagesZagreb Logistics Park BrochureZeljko Stevic RusNo ratings yet

- New Importer Security Filing ISF 10Document6 pagesNew Importer Security Filing ISF 10Jonathan Freitas100% (1)

- Coursera Courses For 2nd Year StudentsDocument2 pagesCoursera Courses For 2nd Year StudentsNaziya TamboliNo ratings yet

- A Study On Buying Behavior of Teenagers in Kannur DistrictDocument5 pagesA Study On Buying Behavior of Teenagers in Kannur DistrictEditor IJRITCCNo ratings yet

- Aud TheoDocument10 pagesAud TheoNicole Anne Santiago SibuloNo ratings yet

- Kinney9eChapter 17 InstructorDocument35 pagesKinney9eChapter 17 InstructorPatricia Allison GaniganNo ratings yet

- ICT Tender Final - Website - Before PrebidDocument219 pagesICT Tender Final - Website - Before PrebidTouheed KhalidNo ratings yet

- Industry Structure AnalysisDocument71 pagesIndustry Structure AnalysisSanat Kumar100% (2)

- Far Reviewer - Conceptual FrameworkDocument3 pagesFar Reviewer - Conceptual Frameworkprish yeolhanNo ratings yet

- #2. C2-Product DesignDocument14 pages#2. C2-Product DesignHashane PereraNo ratings yet

- CBSE Woksheets For Class 12 Entrepreneurship Chapter 5 Business Arithmetic PDFDocument2 pagesCBSE Woksheets For Class 12 Entrepreneurship Chapter 5 Business Arithmetic PDFAbheejit VijayNo ratings yet

- RachitKaw CVDocument3 pagesRachitKaw CVrachit_kawNo ratings yet

- Corpuz, Aily F-Fm2-2-Midterm Practice ProblemDocument5 pagesCorpuz, Aily F-Fm2-2-Midterm Practice ProblemAily CorpuzNo ratings yet

- Top 900 Pharma Cos Admin Heads - SampleDocument7 pagesTop 900 Pharma Cos Admin Heads - SampleRahil Saeed 07889582701No ratings yet

- Welcome Aboard 3 Year Bsa!!Document61 pagesWelcome Aboard 3 Year Bsa!!Riza Mae AlceNo ratings yet

- HR Business Partner Benchmarking ReportDocument25 pagesHR Business Partner Benchmarking ReportTara Selvam100% (1)

- What Is NCFM Exam? What Is Nism Exam? NCFM, Nism Mock Test at WWW - Modelexam.in.Document15 pagesWhat Is NCFM Exam? What Is Nism Exam? NCFM, Nism Mock Test at WWW - Modelexam.in.SRINIVASAN100% (4)

- 3 Payroll ReportDocument4 pages3 Payroll ReportBen NgNo ratings yet

- ConceptualizingDocument8 pagesConceptualizingHyacinth'Faith Espesor IIINo ratings yet