You might also like

- Applied Corporate Finance. What is a Company worth?From EverandApplied Corporate Finance. What is a Company worth?Rating: 3 out of 5 stars3/5 (2)

- Net Present ValueDocument3 pagesNet Present Valuefawzan4zan100% (2)

- Net Present Value (NPV) : Calculation Methods and FormulasDocument3 pagesNet Present Value (NPV) : Calculation Methods and FormulasjozsefczNo ratings yet

- Net Present ValueDocument5 pagesNet Present ValueIsrar KhanNo ratings yet

- Capital BudgetingDocument6 pagesCapital Budgetingblackphoenix303No ratings yet

- NPV CalculationDocument7 pagesNPV CalculationnasirulNo ratings yet

- Extra Reading For Further Comprehension: Net Present Value (NPV)Document27 pagesExtra Reading For Further Comprehension: Net Present Value (NPV)widedbenmoussaNo ratings yet

- Net Present ValueDocument2 pagesNet Present Valueharish chandraNo ratings yet

- Capital Bugeting TechniquesDocument14 pagesCapital Bugeting TechniquesShujja Ur Rehman TafazzulNo ratings yet

- Formulas and Calculation: NPV CalculationsDocument3 pagesFormulas and Calculation: NPV Calculationssadianasir960No ratings yet

- Capital BudgetingDocument9 pagesCapital BudgetingZahidNo ratings yet

- Weighted Average Cost of CapitalDocument6 pagesWeighted Average Cost of CapitalStoryKingNo ratings yet

- Net Present Value vs. Internal Rate of ReturnDocument15 pagesNet Present Value vs. Internal Rate of ReturnSumaira BilalNo ratings yet

- Business Finance WorksheetsDocument11 pagesBusiness Finance WorksheetsShiny NatividadNo ratings yet

- Capital Budgeting MaterialDocument64 pagesCapital Budgeting Materialvarghees prabhu.sNo ratings yet

- Chapter 14 Capital Budgeting DecisionsDocument5 pagesChapter 14 Capital Budgeting DecisionsAime_randriNo ratings yet

- Unit 5Document26 pagesUnit 5Vidhyamahaasree DNo ratings yet

- Investment Decision CriteriaDocument71 pagesInvestment Decision CriteriaBitu GuptaNo ratings yet

- Capital Investment: Decisions: AnDocument16 pagesCapital Investment: Decisions: AnSakshi JhaNo ratings yet

- A Financial Model Is Simply A Tool ThatDocument5 pagesA Financial Model Is Simply A Tool ThatHarshalKolhatkarNo ratings yet

- Economics AssmDocument4 pagesEconomics AssmArpan AdakNo ratings yet

- Chapter Five FMDocument4 pagesChapter Five FMHope GoNo ratings yet

- Solutions: First Group Moeller-Corporate FinanceDocument13 pagesSolutions: First Group Moeller-Corporate Financelefteris82No ratings yet

- Kalyani Government Engineering CollegeDocument4 pagesKalyani Government Engineering CollegeArpan AdakNo ratings yet

- Economics Assignment.Document4 pagesEconomics Assignment.Manojit RoyNo ratings yet

- PA - Chapter 7Document32 pagesPA - Chapter 7Mai Lâm LêNo ratings yet

- Complex Investment DecisionsDocument36 pagesComplex Investment DecisionsAmir Siddiqui100% (1)

- EEF - Capital Budgeting - 2020-21Document31 pagesEEF - Capital Budgeting - 2020-21salkr30720No ratings yet

- Investment Apraisal or Capital Budgeting - IrrDocument4 pagesInvestment Apraisal or Capital Budgeting - IrrJayna CrichlowNo ratings yet

- 06 Lecture - Discounted Cash Flow Applications PDFDocument25 pages06 Lecture - Discounted Cash Flow Applications PDFjgutierrez_castro77240% (1)

- 4.1 Net Present Value & Profitability Index. Feb 1-5Document12 pages4.1 Net Present Value & Profitability Index. Feb 1-5John Garcia100% (1)

- Capital Budgeting Techniques NotesDocument4 pagesCapital Budgeting Techniques NotesSenelwa Anaya86% (7)

- Solutions: First Group Moeller-Corporate FinanceDocument13 pagesSolutions: First Group Moeller-Corporate FinancejwbkunNo ratings yet

- Irr, NPV, PB, ArrDocument54 pagesIrr, NPV, PB, ArrSushma Jeswani Talreja100% (3)

- Net Present Value MethodDocument6 pagesNet Present Value MethodAkash Rs100% (1)

- Chapter 7: Net Present Value and Other Investment Criteria: FIN 301 Class NotesDocument8 pagesChapter 7: Net Present Value and Other Investment Criteria: FIN 301 Class NotesHema BhimarajuNo ratings yet

- Finance Acumen For Non FinanceDocument55 pagesFinance Acumen For Non FinanceHarihar PanigrahiNo ratings yet

- Project Appraisal TechniquesDocument6 pagesProject Appraisal TechniquesChristinaNo ratings yet

- Payback Period:: Period in Capital Budgeting Refers To The Period of Time Required For The Return On An InvestmentDocument4 pagesPayback Period:: Period in Capital Budgeting Refers To The Period of Time Required For The Return On An InvestmentshabnababuNo ratings yet

- Project Appraisal TechniquesDocument11 pagesProject Appraisal TechniquesChristineNo ratings yet

- Capital Budgeting Decisions: Key Terms and Concepts To KnowDocument17 pagesCapital Budgeting Decisions: Key Terms and Concepts To Knownisarg_No ratings yet

- Feasibility Study ReportDocument41 pagesFeasibility Study ReportGail IbayNo ratings yet

- Chapter 6: Introduction To Capital BudgetingDocument3 pagesChapter 6: Introduction To Capital BudgetingDeneree Joi EscotoNo ratings yet

- Chapter 6: Introduction To Capital BudgetingDocument3 pagesChapter 6: Introduction To Capital BudgetingDeneree Joi EscotoNo ratings yet

- DocxDocument12 pagesDocxDiscord YtNo ratings yet

- Project Management: The Financial Perspective: Muhammad UmerDocument37 pagesProject Management: The Financial Perspective: Muhammad Umermumer1No ratings yet

- Industrial Management and Process Economics Assignment: University of The PunjabDocument14 pagesIndustrial Management and Process Economics Assignment: University of The PunjabAbubakr KhanNo ratings yet

- Net Present Value: Mod. 4.3 VCMDocument27 pagesNet Present Value: Mod. 4.3 VCMPrincesNo ratings yet

- DSM 9Document5 pagesDSM 9SoahNo ratings yet

- Project Evaluation Techniques-NPVDocument18 pagesProject Evaluation Techniques-NPVSamar PratapNo ratings yet

- Investment DecDocument29 pagesInvestment DecSajal BasuNo ratings yet

- Chapter 9 PDFDocument29 pagesChapter 9 PDFYhunie Nhita Itha50% (2)

- Capital Budgeting 2Document23 pagesCapital Budgeting 2Rohit Rajesh RathiNo ratings yet

- 4-Capital Budgeting TechniquesDocument20 pages4-Capital Budgeting TechniquesnoortiaNo ratings yet

- Module 2Document9 pagesModule 2vinitaggarwal08072002No ratings yet

- BUSINESS FINANCE NotesDocument9 pagesBUSINESS FINANCE NotesRishia Diniella PorquiadoNo ratings yet

- Net Present Value and The Internal Rate of Return - CFA Level 1 - InvestopediaDocument9 pagesNet Present Value and The Internal Rate of Return - CFA Level 1 - InvestopediaPrannoyChakrabortyNo ratings yet

- Unit 2 Capital Budgeting Technique ProblemsDocument39 pagesUnit 2 Capital Budgeting Technique ProblemsAshok KumarNo ratings yet

- Decoding DCF: A Beginner's Guide to Discounted Cash Flow AnalysisFrom EverandDecoding DCF: A Beginner's Guide to Discounted Cash Flow AnalysisNo ratings yet

- Root Cause Analysis ToolsDocument22 pagesRoot Cause Analysis Toolsjmpbarros100% (4)

- Tuto 4 CPCDocument2 pagesTuto 4 CPCPrabakaran LinggamNo ratings yet

- Time SchedjuleDocument1 pageTime Schedjulebass_121085477No ratings yet

- Pidgin - God's Simple PlanDocument3 pagesPidgin - God's Simple PlanAfrica BiblesNo ratings yet

- 1015Document11 pages1015Crystal Audrey Malinda NelsonNo ratings yet

- Liquefaction of SoilDocument18 pagesLiquefaction of SoilPrabha KaranNo ratings yet

- Deped Form 137 Shs - 1-Gen. Academic StrandDocument4 pagesDeped Form 137 Shs - 1-Gen. Academic StrandCharline A. Radislao100% (3)

- 2nd Term SyllabusDocument1 page2nd Term SyllabusBiplab233No ratings yet

- Topic 6 - Self and Filipino SocietyDocument46 pagesTopic 6 - Self and Filipino SocietyRianne AngelNo ratings yet

- Endress HauserDocument28 pagesEndress Hausermanox007No ratings yet

- Credentials Evaluation Service Applicant HandbookDocument26 pagesCredentials Evaluation Service Applicant HandbookdramachicNo ratings yet

- 5-Prestress Diagram - Equivalent LoadsDocument15 pages5-Prestress Diagram - Equivalent Loadssamuel tejedaNo ratings yet

- Famous Writters-WPS OfficeDocument3 pagesFamous Writters-WPS OfficeMelmel TheKnightNo ratings yet

- Composition of PetroleumDocument17 pagesComposition of PetroleumAleem Ahmed100% (1)

- Physicochemical Characterization of Selected Rice Oryza Sativa Lgenotypes Based On Gel Consistency and Alkali Digestion 2161 1009 1000285 PDFDocument5 pagesPhysicochemical Characterization of Selected Rice Oryza Sativa Lgenotypes Based On Gel Consistency and Alkali Digestion 2161 1009 1000285 PDFJawaria IshfaqNo ratings yet

- 94 Balance of Payments 3Document1 page94 Balance of Payments 3Tiffany100% (1)

- Pre-Test - Science 4Document4 pagesPre-Test - Science 4Jonalyn AntonioNo ratings yet

- Pipe Wrinkle Study-Final ReportDocument74 pagesPipe Wrinkle Study-Final Reportjafarimehdi17No ratings yet

- Solubility Improvement of Curcumin Through PVP K-30 Solid DispersionsDocument6 pagesSolubility Improvement of Curcumin Through PVP K-30 Solid Dispersionsuday_khandavilliNo ratings yet

- Lesson 1 Poster AnalysisDocument5 pagesLesson 1 Poster AnalysisJanvi PatelNo ratings yet

- Disaster Readiness and Risk ReductionDocument239 pagesDisaster Readiness and Risk ReductionGemma Rose LaquioNo ratings yet

- Deforestation in MeghalayaDocument13 pagesDeforestation in MeghalayaSuman SouravNo ratings yet

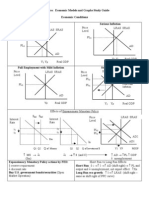

- AP Macroeconomic Models and Graphs Study GuideDocument23 pagesAP Macroeconomic Models and Graphs Study GuideAznAlexT90% (21)

- Superstructure Concrete Quality Control Plan ChecklistDocument5 pagesSuperstructure Concrete Quality Control Plan ChecklistallennicoleNo ratings yet

- Data Collection and Rock Mass ClassificationDocument7 pagesData Collection and Rock Mass ClassificationScott FosterNo ratings yet

- 1964 1obli ChronicleDocument12 pages1964 1obli Chronicleapi-198872914No ratings yet

- ResumeDocument4 pagesResumeapi-233282347No ratings yet

- Turbulence Modeling - BetaDocument88 pagesTurbulence Modeling - BetaMayra ZezattiNo ratings yet

- Group 14 Monitoring SystemDocument27 pagesGroup 14 Monitoring SystemAndrei 26No ratings yet

- Mark Scheme (Results) Summer 2013Document15 pagesMark Scheme (Results) Summer 2013lolomg90No ratings yet